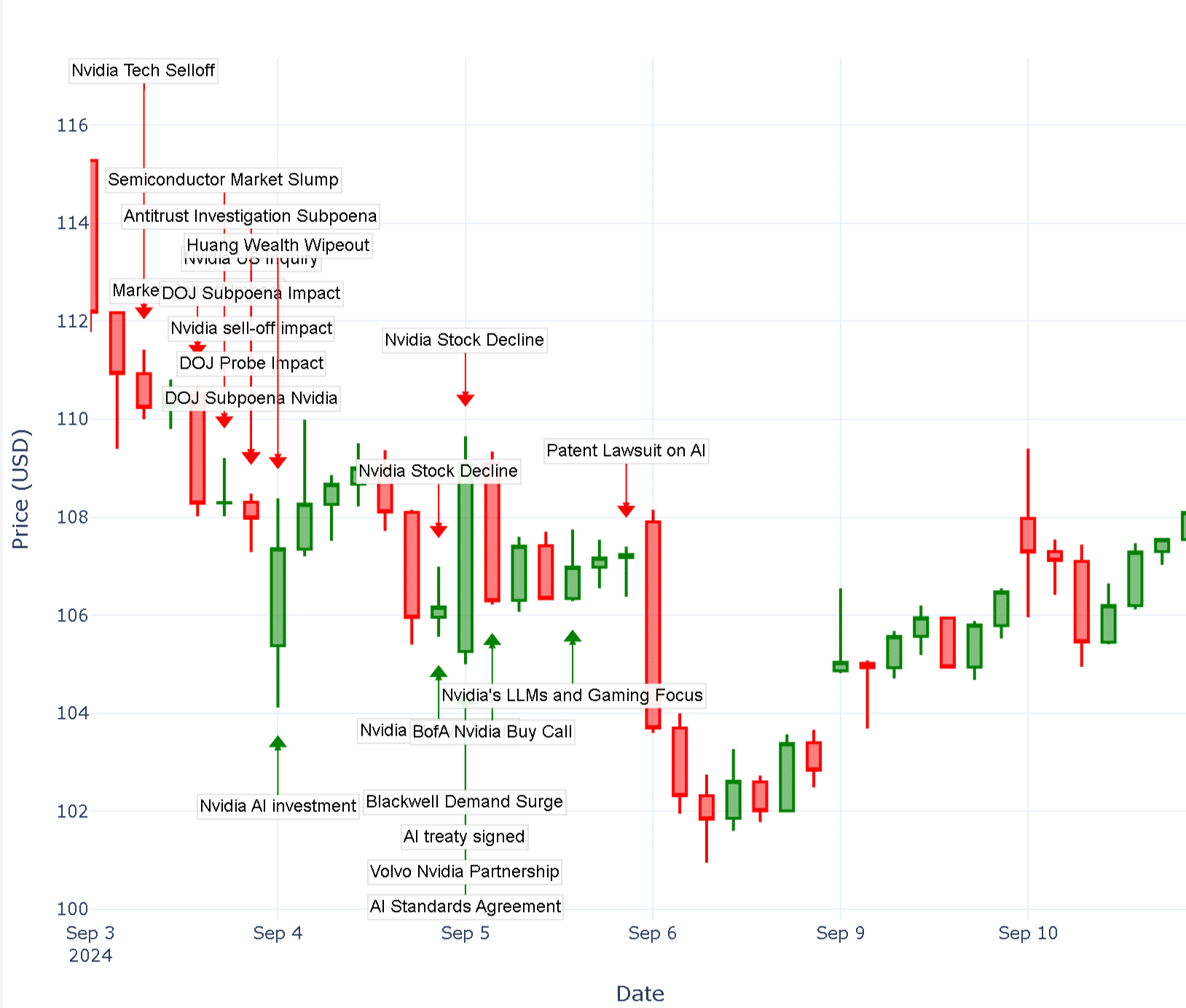

In the modern financial landscape, few tickers command as much attention as NVDA. As the poster child for the artificial intelligence revolution, NVIDIA has transitioned from a niche hardware manufacturer for gamers into a systemic pillar of the global economy. However, even the most formidable market leaders are not immune to volatility. When a stock that has experienced such meteoric growth begins to stumble, investors naturally scramble for answers.

The question “why is NVIDIA stock down?” rarely has a single answer. Instead, it is usually the result of a complex interplay between macroeconomic shifts, valuation corrections, and specific geopolitical risks. To understand the current downward pressure on NVIDIA, one must look beyond the surface-level price action and examine the fundamental financial drivers governing its movement.

Macroeconomic Headwinds and the Broader Market Sentiment

NVIDIA does not trade in a vacuum. As a high-beta growth stock, its performance is deeply intertwined with the broader health of the equity markets and the prevailing monetary policy. When the macroeconomic environment shifts, NVIDIA is often among the first to feel the impact, both on the way up and on the way down.

Interest Rates and the Cost of Capital

The most significant driver of tech stock valuations over the past two years has been the Federal Reserve’s stance on interest rates. In financial modeling, the value of a high-growth company like NVIDIA is heavily weighted toward its future cash flows. When interest rates rise—or remain “higher for longer”—the discount rate applied to those future earnings increases. This mathematically lowers the present value of the stock.

For NVIDIA, which trades at a premium based on earnings expected years into the future, any signal that the Fed will delay rate cuts or that inflation remains sticky creates immediate selling pressure. Investors often rotate out of “expensive” growth stocks and into “safer” fixed-income assets or value stocks when the cost of capital remains high.

The Rotation from Growth to Value

Market cycles are characterized by rotations. After a period of extreme outperformance by the “Magnificent Seven,” institutional investors often engage in profit-taking to rebalance their portfolios. This “Great Rotation” often sees capital moving out of high-flying tech names and into laggard sectors like utilities, healthcare, or small-cap stocks.

When NVIDIA experiences a dip, it is frequently part of a broader “risk-off” sentiment. If a series of economic data points—such as the Consumer Price Index (CPI) or employment reports—suggest an economic slowdown, investors may trim their positions in high-volatility semiconductor stocks to lock in gains and mitigate potential downside.

Valuation Realities: Navigating the “Price for Perfection”

One of the most common reasons for a decline in NVIDIA’s stock price is the sheer weight of expectations. When a company is perceived as the leader of a generational technological shift, it is often “priced for perfection.” This means that the market expects not just good results, but flawless execution and exponential growth.

Analyzing the Price-to-Earnings (P/E) Multiple

Even though NVIDIA has backed up its stock price growth with massive increases in revenue and net income, its valuation multiples can become overextended. Investors often look at the Forward P/E ratio to determine if the stock has become too expensive relative to its projected earnings.

When the P/E ratio reaches historical highs, any slight deviation from the growth narrative can trigger a sell-off. In many cases, NVIDIA’s stock may go down even after reporting record-breaking earnings. This happens because the “whisper numbers”—the unofficial expectations held by professional traders—were even higher than the official analyst estimates. If the company’s guidance for the next quarter is merely “great” instead of “unprecedented,” the market may react by decompressing the valuation multiple.

The Law of Large Numbers and Growth Deceleration

Investors are perpetually forward-looking. NVIDIA has seen triple-digit year-over-year growth in its data center business, but the “Law of Large Numbers” dictates that such growth rates are impossible to sustain indefinitely. As the baseline revenue grows into the tens of billions per quarter, the percentage growth will naturally decelerate.

When the market begins to sense this inevitable deceleration, the stock price often undergoes a “reset.” Investors begin to question if the peak of the AI spending cycle has been reached. If there is any indication that big tech firms (like Microsoft, Alphabet, or Meta) are slowing down their capital expenditure (CapEx) on AI infrastructure, NVIDIA’s stock price will reflect that perceived cooling of demand long before it shows up in the actual financial statements.

Supply Chain Volatility and Geopolitical Constraints

Semiconductors are the new oil—a strategic resource that is central to national security and global industrial dominance. This puts NVIDIA at the heart of geopolitical tensions, particularly between the United States and China.

Export Controls and the China Factor

A significant portion of the downward pressure on NVIDIA in recent months has stemmed from the U.S. Department of Commerce’s evolving export restrictions. China represents a massive market for NVIDIA’s data center chips. When the U.S. government restricts the sale of high-end AI chips (like the H100 or Blackwell series) to Chinese entities, it creates a direct hit to NVIDIA’s total addressable market (TAM).

While NVIDIA has attempted to design “lite” versions of its chips to comply with regulations, the uncertainty surrounding future policy changes creates a “geopolitical risk premium.” Investors hate uncertainty; the possibility of more stringent bans or retaliatory measures from Beijing can cause institutional investors to reduce their exposure to the stock.

Sustaining the AI Infrastructure Build-out

The “AI gold rush” relies on a physical supply chain that is incredibly complex. NVIDIA designs the chips, but it relies on partners like TSMC (Taiwan Semiconductor Manufacturing Company) for fabrication and various other firms for high-bandwidth memory (HBM) and advanced packaging.

Any bottleneck in this supply chain—whether due to natural disasters, logistics issues, or manufacturing yields—threatens NVIDIA’s ability to meet demand. If there are reports that Blackwell chip production is delayed by even a few weeks, the stock can drop significantly. The market views these delays not just as a timing issue, but as an opportunity for competitors to gain a foothold in a rapidly evolving market.

Internal Dynamics: Insider Selling and Earnings Expectations

Beyond the macro and the geo-political, internal signals from within NVIDIA itself often influence the daily movement of the stock.

Executive Stock Sales and Signaling

It is common for high-level executives, including CEO Jensen Huang, to sell shares through pre-arranged 10b5-1 trading plans. While these sales are often planned months in advance for tax purposes or portfolio diversification, the optics can be jarring for retail investors.

When “insider selling” hits the headlines, it can create a psychological ripple effect. Even if the sales represent a tiny fraction of the executive’s total holdings, the narrative can shift to “the insiders think the top is in,” leading to short-term selling pressure from momentum traders.

Beating Estimates vs. Guidance Outlook

NVIDIA’s quarterly earnings calls have become the most important events on the financial calendar. However, the stock’s reaction to these calls is often counterintuitive. We frequently see a “sell the news” phenomenon. Because the stock often rallies in anticipation of the earnings report, the good news is already “priced in” by the time the numbers are released.

If NVIDIA beats earnings but provides “cautious” guidance—perhaps citing supply chain constraints or a transition period between chip architectures—the stock may fall. Investors are less interested in what NVIDIA did over the last three months and are almost exclusively focused on the “guide”—the company’s forecast for the future.

The Path Forward: Risk Management for Modern Investors

Understanding why NVIDIA is down is only half the battle; the other half is determining how to react to that information. For the modern investor, NVIDIA represents both the greatest opportunity and one of the highest risks in a balanced portfolio.

Identifying Key Support Levels

Technical analysis plays a massive role in NVIDIA’s price action because of the high volume of algorithmic trading. When the stock begins to fall, traders look for “support levels”—price points where the stock has historically stopped falling and started rising. If the stock breaks through a key moving average (like the 50-day or 200-day moving average), it can trigger a wave of automated selling, accelerating the dip. Understanding these levels can help investors differentiate between a healthy correction and a fundamental breakdown of the bull case.

Long-term Bull Thesis vs. Short-term Volatility

Ultimately, the reason NVIDIA stock is down usually boils down to a disconnect between short-term market mechanics and long-term fundamental growth. For the long-term investor, periodic pullbacks are a feature of the market, not a bug. They serve to flush out “weak hands” and reset valuations to more sustainable levels.

The core financial question remains: is the demand for accelerated computing still growing? As long as enterprises continue to transition from traditional CPUs to GPUs to power the next generation of software, NVIDIA’s cash-generating machine remains intact. However, in the high-stakes world of investing, the path to the top is rarely a straight line. The current “dip” is simply the market’s way of recalibrating the price of the world’s most sought-after technology in an ever-changing economic landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.