For veterans, active-duty service members, and eligible surviving spouses, the VA home loan program represents one of the most significant financial benefits earned through military service. Unlike conventional financing, VA loans offer unique advantages, most notably the ability to purchase a home with zero down payment and no private mortgage insurance (PMI). However, the question of “what is the interest rate on a VA loan” is rarely answered with a single number. Instead, it involves a complex interplay of secondary market forces, lender-specific overlays, and the individual borrower’s financial profile.

In the realm of personal finance, understanding the mechanics of these rates is essential for making an informed investment in real estate. While the Department of Veterans Affairs (VA) guarantees a portion of the loan, it does not set the interest rates. Private lenders—banks, credit unions, and mortgage companies—determine the rates based on various economic factors. This guide explores the architecture of VA loan interest rates, how they compare to the broader market, and strategies for securing the most competitive terms.

The Fundamentals of VA Loan Interest Rates

To understand VA loan rates, one must first recognize that the VA is an insurer, not a lender. The “rate” is the cost of borrowing capital, and it is influenced heavily by the global bond market.

How VA Rates Are Determined

VA loan rates are largely driven by the performance of Mortgage-Backed Securities (MBS), specifically those guaranteed by Ginnie Mae (the Government National Mortgage Association). When investors buy Ginnie Mae bonds, they are essentially providing the liquidity that allows lenders to issue VA loans. If the demand for these bonds is high, interest rates tend to stay lower.

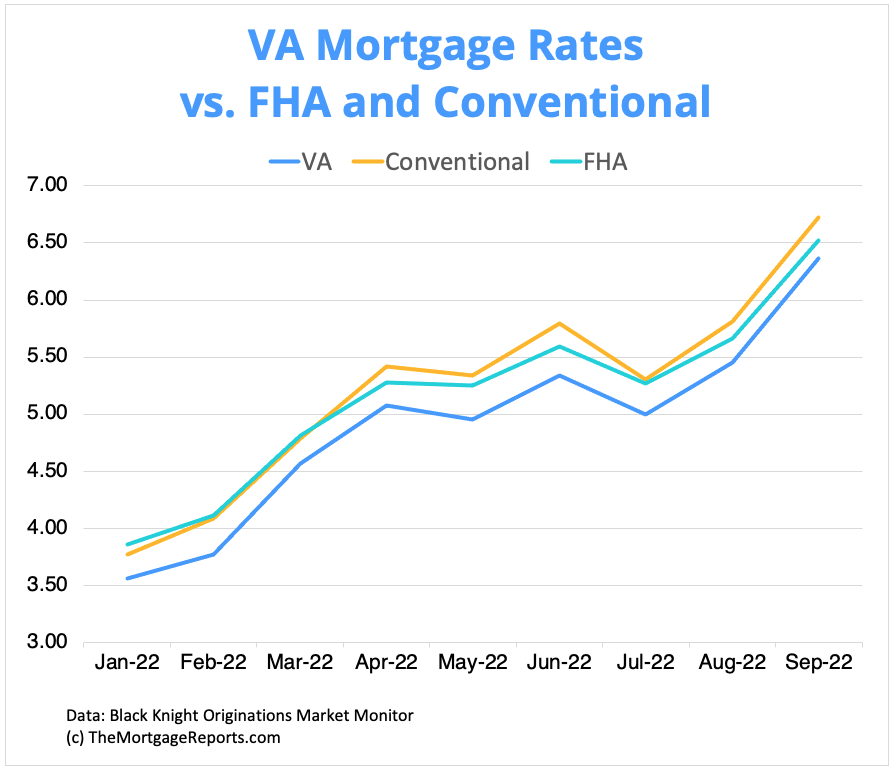

Because VA loans are backed by the federal government, they are considered lower risk for lenders. If a borrower defaults, the VA reimburses the lender for a portion of the loss. This safety net allows lenders to offer interest rates that are typically 0.25% to 0.50% lower than conventional mortgage rates.

VA Rates vs. Conventional and FHA Loans

When comparing VA loans to conventional or FHA (Federal Housing Administration) loans, the VA option almost always wins on a “net effective rate” basis. While a conventional loan might require a 20% down payment to avoid PMI, a VA loan requires no such insurance despite the 0% down requirement. When you factor in the absence of a monthly PMI premium, the total monthly cost of a VA loan is often significantly lower than a conventional loan with the same nominal interest rate.

Key Factors That Influence Your Specific VA Interest Rate

While market trends provide the baseline, your personal financial health determines the final quote you receive from a loan officer. In the world of money management, these variables are known as “risk factors.”

The Role of Credit Scores in VA Lending

Technically, the VA does not mandate a minimum credit score. However, because private lenders take on the remaining risk not covered by the VA guarantee, they implement “overlays.” Most lenders look for a minimum FICO score ranging from 580 to 620.

A higher credit score directly correlates with a lower interest rate. For example, a borrower with a 760 credit score may be offered a rate significantly lower than someone with a 640 score. This is because the lender perceives the high-score borrower as less likely to default, requiring less “risk premium” added to the base rate.

Loan Duration and Type (Fixed vs. ARM)

The structure of the loan also dictates the rate.

- Fixed-Rate VA Loans: These are the most common, usually in 15-year or 30-year terms. A 15-year VA loan typically carries a lower interest rate than a 30-year loan because the lender is exposed to interest rate risk for a shorter period.

- Adjustable-Rate Mortgages (ARM): These offer a lower “introductory” rate for a set period (like 5 years), after which the rate adjusts based on market indexes. While ARMs can save money in the short term, they carry the risk of higher payments in the future if market rates rise.

Market Volatility and Economic Indicators

Broader economic health plays a pivotal role. Mortgage rates are closely tied to the 10-year Treasury yield. When the Federal Reserve raises the federal funds rate to combat inflation, mortgage rates generally trend upward. Conversely, in a sluggish economy, rates may drop to encourage borrowing and spending. For a veteran looking to buy, keeping an eye on inflation reports and Fed announcements is a crucial part of timing the market.

Hidden Costs and Savings: Beyond the Interest Rate

A mortgage is more than just an interest rate; it is a total cost of capital. To accurately calculate the “money” aspect of a VA loan, one must account for the VA Funding Fee and the unique savings structure of the program.

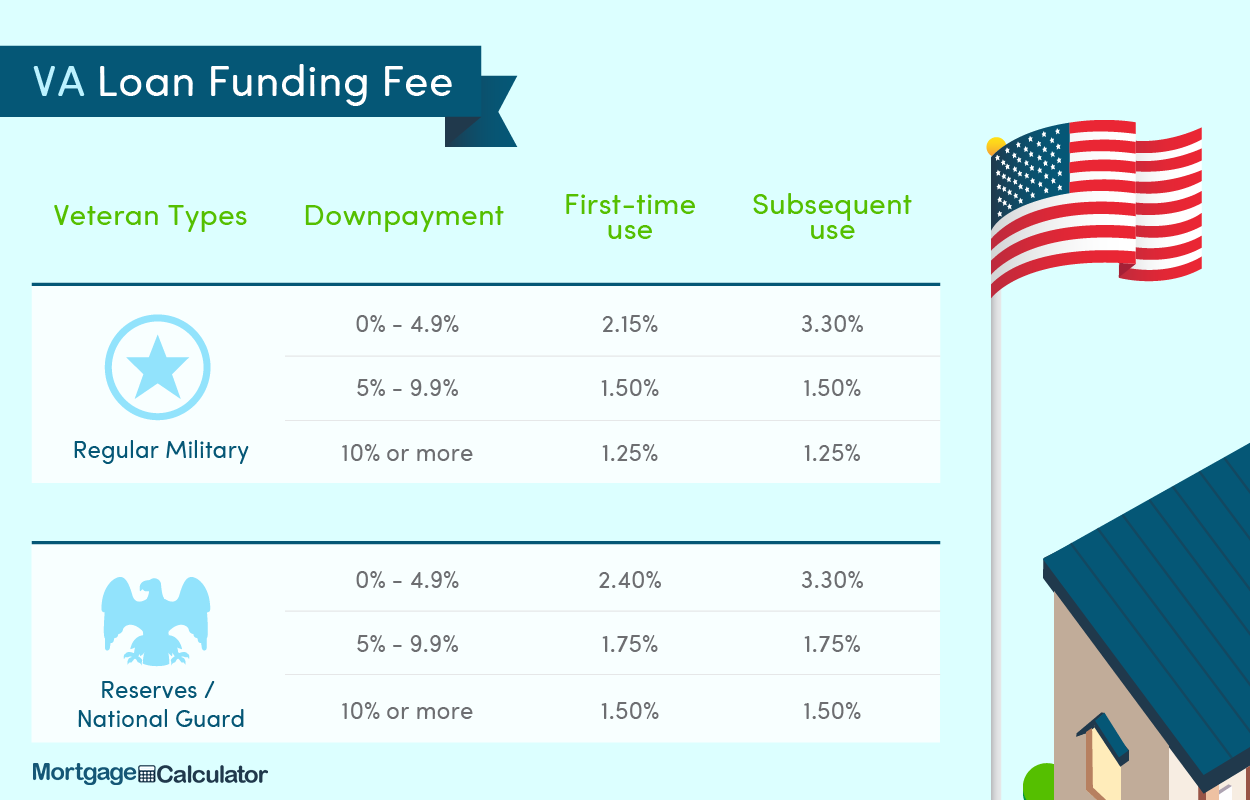

The VA Funding Fee Explained

Since VA loans do not require PMI, the program is sustained by the VA Funding Fee. This is a one-time payment made to the Department of Veterans Affairs to help reduce the cost of the program to taxpayers. The fee varies based on the down payment amount and whether it is the veteran’s first time using the benefit.

For first-time users with zero down, the fee is typically 2.15% of the loan amount. While this fee can be rolled into the loan—meaning it doesn’t have to be paid upfront—it does increase the total principal, which in turn increases the total interest paid over the life of the loan. Notably, veterans with a service-connected disability rating of 10% or higher are exempt from this fee, providing a massive financial advantage.

The Benefit of No Private Mortgage Insurance (PMI)

In conventional financing, if you put down less than 20%, you must pay PMI, which can cost between 0.5% and 1.5% of the loan amount annually. On a $400,000 home, that could be an extra $200 to $400 per month. Because VA loans eliminate this requirement, the borrower’s purchasing power is significantly increased. Even if a VA loan’s nominal interest rate were identical to a conventional rate, the VA loan would still be the superior financial tool due to the absence of PMI.

Closing Costs and Lender Credits

VA guidelines strictly limit the types of closing costs a veteran can pay. Lenders are also allowed to offer “lender credits”—where the lender pays part of the closing costs in exchange for a slightly higher interest rate. This is a strategic choice: would you rather have a 6.5% rate and pay $0 at closing, or a 6.0% rate and pay $6,000 upfront? For those with limited liquid cash but stable income, taking a slightly higher rate in exchange for credits is a valid financial strategy.

Strategies to Secure the Lowest Possible VA Interest Rate

Securing a low rate is not a matter of luck; it is a matter of preparation and aggressive shopping.

Comparing Multiple Lenders

The single most effective way to lower your interest rate is to shop around. Because the VA does not set rates, different lenders will offer different deals. A large national bank might have higher overhead and thus higher rates, while a specialized online VA lender or a local credit union might offer more competitive terms. It is recommended to get at least three official Loan Estimates to compare the “APR” (Annual Percentage Rate), which includes both the interest rate and the fees.

Buying Down the Rate with Discount Points

Borrowers can “buy down” their interest rate by paying discount points at closing. One point equals 1% of the loan amount. For example, on a $300,000 loan, paying $3,000 upfront might lower your interest rate by 0.25%.

To determine if this is a wise financial move, calculate the “break-even point.” If the lower rate saves you $50 a month, and the point costs $3,000, it will take 60 months (5 years) to break even. If you plan to stay in the home for 10 years, buying points is a great investment; if you plan to move in 3 years, it is a waste of capital.

Improving Your Debt-to-Income (DTI) Ratio

While credit score is vital, your DTI ratio—the percentage of your gross monthly income that goes toward debt—also affects lender confidence. Lenders generally prefer a DTI of 41% or lower for VA loans, though they can go higher with “compensating factors.” Reducing credit card balances or paying off a car loan before applying for a mortgage can make you a more attractive borrower, potentially qualifying you for a better “tier” of interest rates.

The Future of VA Loans in a Changing Economic Landscape

Real estate is a long-term asset, and the VA loan program provides tools to manage that asset even after the initial purchase.

Refinancing Options: IRRRL and Cash-Out

If you purchase a home when interest rates are high, you are not necessarily stuck with that rate for 30 years. The VA Interest Rate Reduction Refinance Loan (IRRRL), also known as a VA Streamline, allows veterans to refinance to a lower rate with minimal paperwork and no appraisal. This is one of the most powerful financial tools in the VA arsenal, allowing homeowners to lower their monthly expenses as soon as market conditions improve.

Additionally, the VA Cash-Out Refinance allows veterans to tap into their home’s equity to pay off high-interest debt, fund home improvements, or bolster an investment portfolio. Since VA cash-out rates are typically lower than personal loan or credit card rates, this can be a savvy move for debt consolidation.

Long-term Financial Planning with a VA Loan

Ultimately, the interest rate on a VA loan is the “price” of the capital you are using to build wealth through homeownership. By leveraging the 0% down payment and lower-than-market rates, veterans can keep more of their money in other investments—such as a 401(k), TSP, or brokerage account—where it can grow at a rate higher than the mortgage interest cost.

In conclusion, while the question “what is the interest rate on a VA loan” has a fluctuating answer based on the economy, the program consistently offers the most favorable terms in the American mortgage market. By understanding the factors that drive these rates and employing strategic financial behaviors, veterans can maximize the value of this hard-earned benefit, ensuring long-term fiscal stability and the successful realization of the American dream of homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.