In the complex ecosystem of global economics, few numbers carry as much weight for the average consumer and business owner as the prime lending rate. Often referred to simply as the “prime rate,” this figure serves as the foundational benchmark for a vast array of credit products, from the interest on your credit card to the cost of a small business loan. Understanding what the prime lending rate is today—and how it fluctuates—is essential for anyone looking to navigate the waters of personal finance, real estate, or corporate investment.

As of the current economic climate, the prime rate is a reflection of the broader efforts by central banks to balance growth against inflation. While the specific number changes in response to central bank policy, its influence remains constant, acting as the starting point from which most commercial banks determine their lending costs.

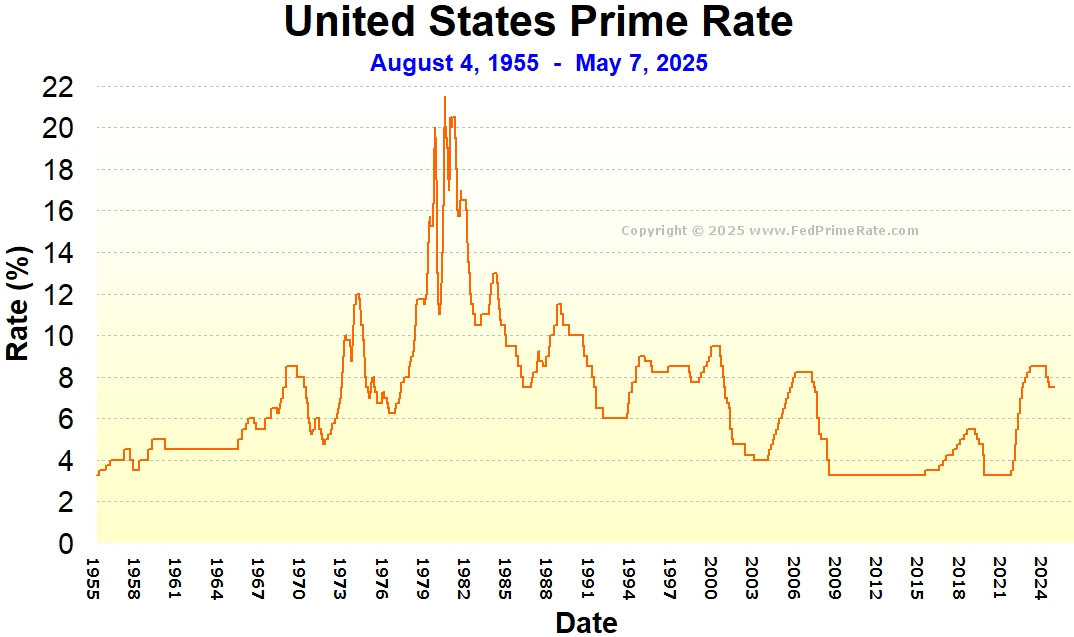

Understanding the Prime Lending Rate: The Foundation of Borrowing

To understand where the prime rate stands today, one must first understand what it represents. At its core, the prime lending rate is the interest rate that commercial banks charge their most creditworthy corporate customers. It is the “base” rate; essentially, it is the lowest rate at which a bank is willing to lend money without losing its profit margin or taking on excessive risk.

The Standard Calculation: Fed Funds + 3%

In the United States, the prime rate is directly tied to the federal funds target rate, which is set by the Federal Open Market Committee (FOMC). By long-standing convention, the prime rate is typically set at 3 percentage points (or 300 basis points) above the federal funds rate. For example, if the Federal Reserve sets the target range for the federal funds rate at 5.25% to 5.50%, the prime rate will almost universally be adjusted to 8.50%. This 3% spread covers the bank’s operating costs and provides a baseline profit margin.

The Role of the Wall Street Journal (WSJ) Prime Rate

While individual banks can technically set their own prime rates, the industry looks to the Wall Street Journal as the definitive source. The WSJ surveys the 30 largest banks in the United States and publishes the “Prime Rate” when at least 23 of those 30 banks (or 75%) have changed their rate. This ensures a level of uniformity across the financial sector, preventing massive discrepancies in borrowing costs from one major institution to another.

Why “Prime” Customers Get the Best Deals

The term “prime” refers to the high quality of the borrower. These are typically large corporations with impeccable credit histories, deep cash reserves, and low default risks. For the average consumer, the prime rate acts as a floor. Most personal loans, credit cards, and mortgages are priced as “Prime plus X%.” Your personal credit score determines how much “X” is added to that base rate.

Why the Prime Rate Changes: The Hand of the Federal Reserve

The prime rate is not a static figure; it is a dynamic tool used to manage the temperature of the economy. When the economy is “overheating”—meaning inflation is rising too quickly—the Federal Reserve raises interest rates to discourage spending and borrowing. Conversely, when the economy is sluggish, the Fed lowers rates to stimulate investment.

Federal Reserve Monetary Policy and Inflation

The primary driver of today’s prime rate is the Federal Reserve’s “dual mandate”: to promote maximum employment and stable prices. In recent years, high inflation levels have forced the Fed to aggressive action. By raising the federal funds rate, they automatically trigger a rise in the prime rate. This makes it more expensive for businesses to expand and for consumers to buy on credit, which theoretically slows down the demand that drives up prices.

Economic Growth and Market Sentiment

Beyond inflation, the prime rate is influenced by general economic health. In times of robust GDP growth, the prime rate may remain elevated to prevent a “bubble.” However, if indicators show a potential recession—such as rising unemployment or a contraction in manufacturing—the Fed will likely signal a “pivot,” lowering rates to make money “cheaper” and encourage businesses to start hiring and spending again.

The Lag Effect on Consumer Interest Rates

It is important to note that when the Federal Reserve moves, the prime rate moves almost instantly. Most major banks update their prime rates within 24 to 48 hours of an FOMC announcement. This “lag” is virtually non-existent for the prime rate, though it may take several billing cycles for the change to manifest on a consumer’s credit card statement or a variable-rate mortgage adjustment.

How the Prime Rate Affects Your Personal Finances

For the individual investor or household, the prime rate is more than just a macroeconomic indicator—it is a direct factor in the monthly budget. Because so many consumer products are “variable-rate,” a shift in the prime rate can lead to immediate changes in disposable income.

Credit Cards and Variable APRs

Perhaps the most direct impact is felt on credit card balances. Most credit cards have a variable Annual Percentage Rate (APR) that is tied to the prime rate. If you look at your credit card agreement, you will likely see a formula such as “Prime + 12.99%.” If the prime rate is 8.50%, your interest rate is 21.49%. If the Fed raises rates and the prime rate jumps to 8.75%, your APR automatically climbs to 21.74%. Over time, these incremental shifts can cost consumers thousands of dollars in additional interest payments.

HELOCs (Home Equity Lines of Credit)

Homeowners with a HELOC are particularly sensitive to prime rate movements. Unlike a traditional fixed-rate mortgage, a HELOC is almost always a variable-rate product tied to the prime rate. When the prime rate is low, a HELOC is a very cheap way to finance home improvements. However, in a rising-rate environment, the monthly interest-only payments on a HELOC can skyrocket, putting pressure on homeowners who have borrowed significantly against their equity.

Business Loans and Commercial Lines of Credit

For entrepreneurs and small business owners, the prime rate determines the cost of doing business. Many commercial loans are structured as “Prime + 1” or “Prime + 2.” A high prime rate means that the cost of capital is higher, which might lead a business to delay purchasing new equipment, hiring new staff, or expanding into new markets. Conversely, a falling prime rate can provide the financial “oxygen” a small business needs to scale.

Strategies to Navigate a High-Interest Environment

When the prime lending rate is high, as it has been in recent cycles, consumers and businesses must adapt their financial strategies to protect their bottom lines. Managing debt effectively requires a proactive approach rather than a passive one.

Debt Consolidation and Refinancing

One of the most effective ways to mitigate the impact of a high prime rate is to move away from variable-rate debt. If you have significant credit card debt or a HELOC, it may be prudent to consolidate those balances into a fixed-rate personal loan. While the interest rate on a personal loan is still influenced by the current economy, the fixed nature of the loan protects you from future hikes in the prime rate, providing predictable monthly payments.

Prioritizing High-Interest Variable Debt

In a high-rate environment, the “Avalanche Method” of debt repayment becomes even more critical. This strategy involves paying the minimum on all debts but putting every extra dollar toward the debt with the highest interest rate—which is almost certainly a variable-rate credit card tied to the prime rate. By eliminating the most expensive debt first, you reduce the “compounding” effect that high prime rates have on your balance.

Improving Your Credit Score to Secure Better Margins

While you cannot control the prime rate, you can control the margin that lenders add to it. A borrower with a 780 credit score might be offered “Prime + 2%,” while someone with a 620 score might be offered “Prime + 10%.” By improving your credit score—through timely payments, low credit utilization, and correcting errors on your credit report—you can effectively “lower” your personal interest rate even if the national prime rate remains high.

The Future Outlook: What to Expect in the Coming Months

Predicting the prime rate today requires a close eye on the Federal Reserve’s “dot plot” and various economic indicators. As we look toward the future, the trajectory of the prime rate will depend on several key factors.

Analyzing Economic Indicators

The prime rate will likely remain elevated until the Federal Reserve sees “clear and convincing” evidence that inflation is returning to its 2% target. Investors should watch the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index. If these numbers trend downward, the Fed will eventually have the room to lower the federal funds rate, which will, in turn, lower the prime rate.

Expert Predictions for Rate Cuts vs. Hikes

Market analysts are constantly debating the timing of the next “rate cut.” While the prime rate has seen significant peaks recently, many economists believe that as the economy cools, we will see a gradual series of reductions. However, these cuts are rarely as fast as the hikes. The Fed often takes an “escalator up, elevator down” approach—or sometimes, a slow “staircase” down—to ensure they don’t reignite inflation by making money too cheap too quickly.

In conclusion, the prime lending rate is the heartbeat of the financial system. Whether you are looking to buy a home, start a business, or simply manage your monthly credit card bill, the prime rate dictates the terms of your engagement with the economy. By staying informed about the Federal Reserve’s movements and understanding the mechanics of how the prime rate is calculated, you can make more informed, strategic decisions about your money, ensuring that you are not just a spectator to economic shifts, but a prepared participant.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.