Launching a new venture is often romanticized as an act of pure creativity or a pursuit of technological innovation. However, beneath the surface of every disruptive startup and successful local enterprise lies a cold, hard truth: a business is a financial entity. Without a robust capital structure, a sustainable revenue model, and meticulous cash flow management, even the most brilliant ideas will eventually run dry. To start a business in the modern economy is to build a financial engine that generates more value than it consumes.

This guide focuses exclusively on the “Money” niche of entrepreneurship. We will move past the aesthetics of branding and the mechanics of product development to focus on the fiscal pillars required to take a business from a conceptual cost center to a profitable asset.

Securing Capital and Funding Strategies

The first hurdle for any entrepreneur is the acquisition of “dry powder”—the capital necessary to move from the drawing board to the marketplace. How you choose to fund your business will dictate your level of control, the speed of your growth, and your eventual exit strategy.

Bootstrapping vs. External Investment

Bootstrapping—funding your business through personal savings and early sales—remains the most common way to start. The primary advantage is total equity retention; you answer only to yourself and your customers. Financially, it forces a lean operation, which often leads to more disciplined spending. However, the limitation of bootstrapping is the “speed to market.” If your industry is capital-intensive or requires rapid scaling to capture a network effect, personal funds may prove insufficient.

Conversely, external investment involves trading equity for capital. This path is suitable for high-growth potential businesses. By bringing in outside money, you exchange a piece of the pie for a much larger oven. The challenge here is the dilution of ownership and the fiduciary responsibility to prioritize investor returns, which can sometimes conflict with long-term operational stability.

Navigating Venture Capital and Angel Investors

For businesses with the potential for 10x or 100x returns, Angel Investors and Venture Capitalists (VCs) are the primary sources of funding. Angel investors are typically high-net-worth individuals who provide seed capital in exchange for convertible debt or ownership equity. They are often more patient than VCs and may provide mentorship.

Venture Capital, however, is a different beast. VCs manage pooled money from institutional investors and look for businesses that can reach an IPO or a massive acquisition. When seeking VC funding, your business plan must be backed by rigorous financial modeling. You aren’t just selling a product; you are selling a financial instrument. You must be able to demonstrate a clear path to “Series A” and beyond, showing how every dollar of investment will be leveraged to increase the company’s valuation.

Crowdfunding and Alternative Lending

The democratization of finance has introduced crowdfunding as a viable entry point. Platforms like Kickstarter (reward-based) or WeFunder (equity-based) allow you to test market demand while simultaneously raising capital. This serves as a dual-purpose tool: it provides the funds to manufacture or launch while proving to future investors that there is a paying audience for your solution.

Additionally, for businesses with consistent revenue but a need for growth capital, alternative lending and Revenue-Based Financing (RBF) are becoming popular. Unlike traditional bank loans that require heavy collateral, RBF providers take a percentage of future gross revenues until a predetermined amount is paid back. This aligns the cost of capital with your business’s performance.

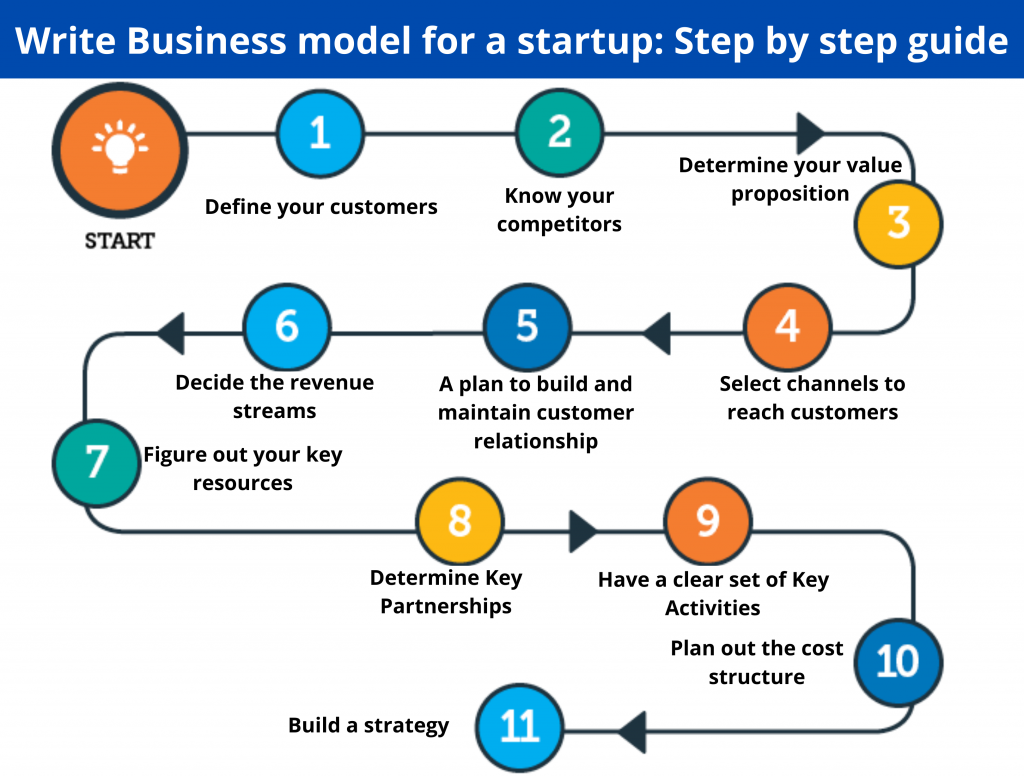

Designing a Sustainable Business Model

Once capital is secured, the focus shifts to the internal mechanics of the business. A business model is essentially a map of how money flows in and out of your organization. Without a clear understanding of your unit economics, growth can actually lead to bankruptcy—a phenomenon known as “growing broke.”

Cost Structure and Revenue Streams

A professional financial strategy requires a granular breakdown of costs. Fixed costs (rent, salaries, software subscriptions) must be balanced against variable costs (raw materials, shipping, transaction fees). The goal is to reach the “break-even point” as quickly as possible.

On the revenue side, diversification is key to financial resilience. Relying on a single revenue stream is a risk. Are there opportunities for recurring revenue (subscriptions)? Can you offer premium add-ons? By mapping out multiple revenue streams, you create a buffer against market volatility. For example, a service-based business might add a digital product or a tiered maintenance plan to ensure steady cash flow during off-peak months.

Unit Economics: Understanding Your Margin

The most critical metric for any startup is the relationship between Customer Acquisition Cost (CAC) and Lifetime Value (LTV).

- CAC: How much do you spend on marketing, sales, and outreach to acquire one customer?

- LTV: How much total net profit will that customer generate over the duration of their relationship with your business?

In a healthy business, the LTV should be at least three times the CAC (LTV:CAC > 3:1). If your cost to acquire a customer is higher than the profit they generate, your business is a “leaky bucket.” No amount of funding can fix a business model where the unit economics are fundamentally broken. Professional entrepreneurs obsess over these numbers, constantly looking for ways to lower CAC through organic growth or increase LTV through retention and upselling.

Scalability and Long-term Valuation

Financial sustainability is not just about staying in the black; it’s about building equity value. Investors and buyers look for “scalable” models—those where revenue can grow exponentially while costs grow only linearly. Software and digital products are classic examples of high-scalability models. If you are starting a service-based business, scalability often comes from “productizing” your services or leveraging technology to reduce the man-hours required per unit of revenue. The ultimate goal is to build an entity that has a high “multiple” of earnings (EBITDA), making it an attractive asset for a future exit.

Financial Management and Operational Excellence

With the model in place, the day-to-day survival of the business depends on operational finance. This is where many entrepreneurs fail—not because they lacked a good idea, but because they lost track of their bank balance.

Cash Flow Management: The Lifeblood of Early-Stage Ventures

There is a profound difference between “profit” and “cash flow.” A business can be profitable on paper (accrual accounting) but have zero dollars in the bank because customers haven’t paid their invoices yet. Cash flow management involves timing your outflows (payables) and inflows (receivables) to ensure you always have enough liquidity to meet your obligations.

A common strategy for startups is to negotiate longer payment terms with suppliers while requiring immediate payment from customers. This “negative working capital” cycle effectively allows your suppliers to finance your growth. Regularly updating a 13-week cash flow forecast is a non-negotiable habit for any serious business owner.

Tax Planning and Legal Structuring

The legal structure you choose (LLC, S-Corp, C-Corp, or Sole Proprietorship) has massive implications for your tax liability and your ability to raise money. For instance, a C-Corp is often preferred by VCs because of its standardized share structure and potential for Qualified Small Business Stock (QSBS) tax exemptions.

Proper tax planning is not about evasion; it’s about optimization. By understanding deductible business expenses, R&D tax credits, and depreciation, you can significantly reduce your “burn rate” (the speed at which you spend your capital). Professional financial advice in the first year can often save a business tens of thousands of dollars in unnecessary tax payments, which can then be reinvested into growth.

Financial Reporting and KPI Tracking

You cannot manage what you do not measure. A professional startup should have a “dashboard” of Key Performance Indicators (KPIs) updated weekly. These include:

- Burn Rate: How much cash are you losing each month?

- Runway: Based on your current cash and burn rate, how many months do you have before you run out of money?

- Gross Margin: The percentage of revenue remaining after COGS (Cost of Goods Sold).

- Accounts Receivable Turnover: How quickly are your customers paying you?

Utilizing cloud-based financial tools like QuickBooks or Xero, integrated with specialized forecasting software, allows for real-time visibility into these metrics.

Scaling the Bottom Line

Starting a business is about survival; growing a business is about strategic reinvestment and wealth creation. Once the business is stable, the financial focus shifts from “not dying” to “thriving.”

Reinvesting Profits for Growth

A common mistake among first-time founders is pulling too much money out of the business too early for personal use. To scale, a significant portion of the net profit should be reinvested. This could mean hiring key personnel who can take over operational tasks, investing in more efficient equipment, or increasing the marketing budget to capture a larger market share. The “Money” mindset views profit not as a personal paycheck, but as fuel for the engine.

Preparing for an Exit Strategy

Even at the startup stage, a sophisticated entrepreneur keeps an eye on the exit. Whether it’s an acquisition by a larger competitor, a management buyout, or an IPO, your financial records must be “audit-ready” from day one. Clean books, clear contracts, and a proven history of profitability or strategic growth increase the valuation of your business significantly.

An exit strategy is the ultimate realization of the business as a financial asset. It is the moment where the years of managing margins, optimizing taxes, and securing capital culminate in a significant liquidity event. By treating the business as a financial product from the start, you ensure that when the time comes to sell, the value you’ve created is undeniable and highly compensated.

In conclusion, starting a business is an exercise in financial engineering. While passion and product are the spark, money is the fuel and the frame. By mastering the art of capital acquisition, unit economics, and cash flow management, you transform a risky venture into a sustainable, wealth-generating enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.