In the modern landscape of personal finance, digital wallets have evolved from convenient novelties into essential tools for daily liquidity. Venmo, a subsidiary of PayPal, has become the de facto standard for peer-to-peer (P2P) transactions in the United States, processing hundreds of billions of dollars annually. However, for many users, the seamless experience of sending and receiving money is occasionally interrupted by a frustrating phenomenon: the payment hold.

When Venmo places a hold on your money, it can disrupt your personal cash flow, delay bill payments, or create anxiety regarding the security of your capital. Understanding why these holds occur requires a look into the intersection of financial regulations, risk management algorithms, and the operational mechanics of digital banking. This article explores the various reasons your funds might be inaccessible and how to navigate the complexities of digital payment platforms.

The Mechanics of Venmo’s Holding Policy

To understand why your money is being held, one must first understand how Venmo functions as a financial intermediary. Unlike a traditional wire transfer, which moves through the Federal Reserve’s plumbing, Venmo operates as a private ledger. When someone sends you money, the “balance” reflects on your screen almost instantly, but the actual movement of underlying assets takes longer.

Standard Transfers vs. Instant Transfers

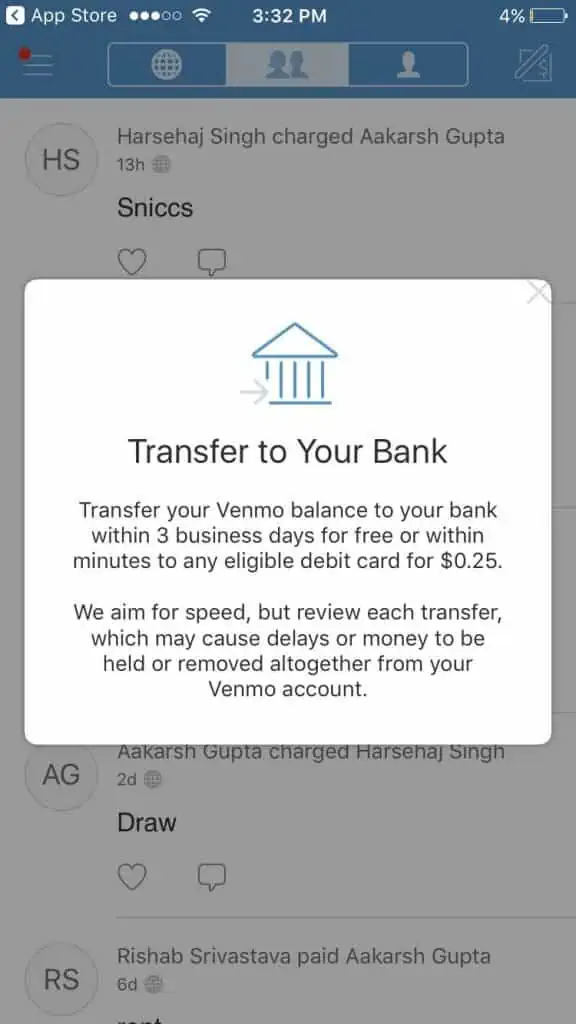

The most common reason for a perceived “hold” is simply the standard processing time of the ACH (Automated Clearing House) network. When you initiate a standard transfer from your Venmo balance to your bank account, it typically takes one to three business days. During this window, the money is in transit—it has left Venmo’s ledger but has not yet been cleared by your bank’s internal systems.

Venmo offers an “Instant Transfer” feature for a small percentage fee, which utilizes the Real-Time Payments (RTP) network or pushed debit card transactions. If you opt for the standard version, the money isn’t being “held” out of malice; it is subject to the legacy speeds of the American banking system.

The Role of the Venmo Balance

Another layer of complexity involves the Venmo balance itself. If you have not verified your identity according to federal standards, Venmo may hold funds within your account without allowing you to “spend” them using a Venmo debit card or transfer them to others. In this scenario, the money is technically there, but your access is restricted until you meet specific financial tool requirements. This acts as a temporary escrow, ensuring that the platform remains compliant with financial oversight bodies.

Why Your Money is Flagged: Security and Regulatory Compliance

Digital payment platforms are not just tech companies; they are “Money Service Businesses” (MSBs). As such, they are subject to stringent federal laws designed to prevent financial crimes. When a hold is placed on a specific transaction, it is often the result of an automated system flagging the movement of funds for manual review.

Anti-Money Laundering (AML) and KYC Regulations

Under the USA PATRIOT Act and other federal mandates, financial institutions are required to implement “Know Your Customer” (KYC) and “Anti-Money Laundering” (AML) protocols. These regulations require Venmo to verify the identity of its users and monitor transactions for patterns that suggest illegal activity.

If you receive a large sum of money from a new contact, or if your account activity suddenly spikes in volume, Venmo’s algorithm may trigger a hold. This is a defensive measure to ensure the funds are not being laundered or used to facilitate illicit trades. While it feels like an inconvenience to the legitimate user, these holds are a legal requirement for Venmo to maintain its license to operate.

Identifying Suspicious Activity and Potential Fraud

Venmo’s security systems are designed to protect both the sender and the receiver. If a transaction appears out of character for your typical spending habits—such as a login from a new geographic location followed by a high-value transfer—the system may place the funds on hold or “freeze” the account.

Furthermore, if the person who sent you money has a history of disputed charges or is using a compromised credit card, Venmo will hold the funds to prevent a “chargeback” scenario. If Venmo were to release the money to you immediately and the sender’s bank later clawed it back as a fraudulent transaction, Venmo would be left with a financial loss. The hold serves as a buffer period to ensure the source of the funds is legitimate.

Common Scenarios Leading to Funds Being Placed on Hold

Beyond the broad strokes of regulation, there are several specific, day-to-day scenarios that can trigger a hold on your money. Recognizing these can help you manage your expectations and adjust your financial planning accordingly.

New Account Limitations

For new users, Venmo often implements a “probationary” period. During the first few weeks of account ownership, or until a certain number of successful transactions have been completed, Venmo may hold incoming funds for an extended period. This allows the platform to build a risk profile for the user. Once you have established a history of legitimate behavior and have successfully linked and verified a bank account, these holds typically become less frequent.

Large or Unusual Transaction Volumes

Every user has an internal “velocity limit” assigned by the platform’s risk engine. If you typically use Venmo to split $20 pizza bills and suddenly receive a $3,000 transfer for “rent” or “car sale,” the system will likely flag the transaction. High-value transfers are the most common cause of multi-day holds. In these cases, Venmo may require additional documentation or a simple cooling-off period to ensure the transaction isn’t a result of social engineering fraud or an accidental overpayment.

Disputes and Reversals

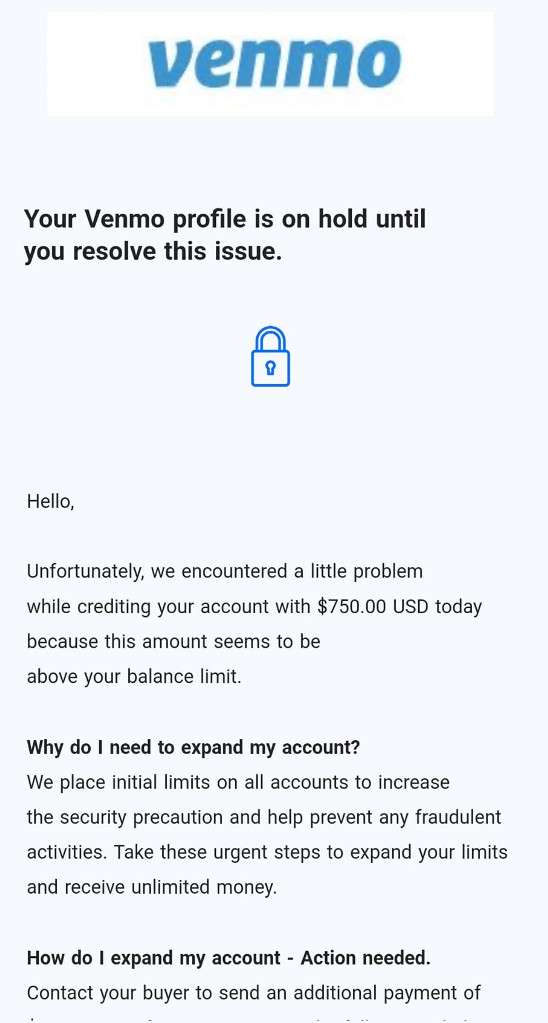

If a sender contacts their bank to dispute a transaction made to you, Venmo will immediately place a hold on those funds (or an equivalent amount in your balance). This is common in “accidental” payment scams, where a stranger sends you money and asks you to send it back, only for their original payment to be reversed a few days later. If the money is in a “hold” status due to a dispute, it remains in a financial limbo until the platform’s dispute resolution team determines the rightful owner.

How to Prevent and Resolve Payment Holds

While some holds are inevitable due to systemic processing times, many can be avoided or resolved quickly through proactive account management. Treating your Venmo account with the same level of diligence as a traditional bank account is the best way to ensure liquidity.

Verifying Your Identity for Higher Limits

The single most effective way to reduce holds is to complete the identity verification process. This involves providing your full legal name, date of birth, and Social Security Number (SSN). Once verified, you move into a higher tier of trust within the ecosystem. This not only increases your weekly spending and transfer limits but also reduces the likelihood of “compliance holds” triggered by KYC triggers.

Best Practices for Business vs. Personal Profiles

A frequent mistake users make is using a personal profile for commercial transactions. If you are selling goods or services, you should use a Venmo Business Profile. Transactions processed through a business profile are subject to “Seller Protection,” but they also come with different holding patterns.

For business owners, Venmo may hold funds for up to 21 days—similar to PayPal’s model—to ensure the buyer receives their item and doesn’t file a dispute. If you use a personal account for business and the algorithm detects it (through keywords in memos like “shipping” or “invoice”), the account may be flagged for a terms-of-service violation, leading to a long-term hold on all funds.

The Future of Digital Liquidity and Peer-to-Peer Payments

The friction of “held” money is a byproduct of a financial system in transition. As the United States moves toward more modern infrastructures like FedNow (the Federal Reserve’s instant payment service), the gap between a digital “send” and a bank “clear” will continue to narrow.

However, as long as fraud remains a threat, risk-based holds will remain a part of the digital finance landscape. Users must recognize that Venmo is not merely a social app but a sophisticated financial tool. By maintaining a verified account, staying within typical transaction patterns, and understanding the regulatory environment, you can minimize the time your money spent in “holding” and ensure that your digital capital remains as liquid as possible.

In conclusion, while “why is Venmo holding my money” is a question born of frustration, the answer is usually rooted in a combination of banking legacy, federal law, and fraud prevention. By navigating these rules with a professional approach to your personal finances, you can turn a digital wallet into a reliable pillar of your financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.