In the modern landscape of personal finance, the speed at which money moves is often just as important as the amount being moved. Venmo has transitioned from a niche social payment app to a foundational financial tool for millions of users, facilitating everything from splitting dinner bills to paying rent and receiving professional payments. However, as users integrate Venmo more deeply into their financial lives, a critical question arises: how long does a Venmo transfer actually take?

Understanding the nuances of transfer speeds is essential for effective cash flow management. Whether you are waiting for funds to cover an upcoming bill or moving a side-hustle payment into your primary savings account, the timing of these transactions is governed by a mix of banking regulations, internal security protocols, and the specific service tier you choose.

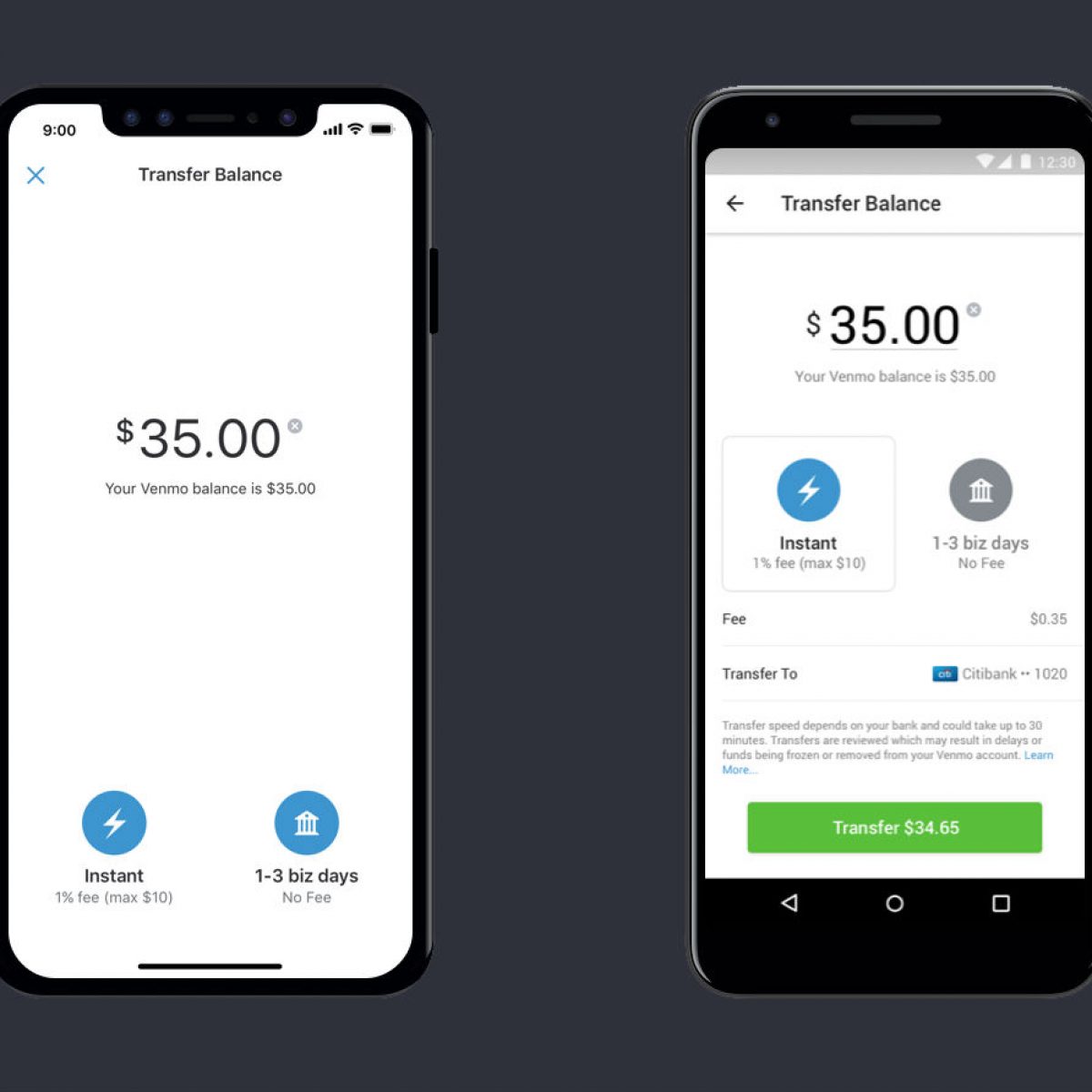

Understanding Venmo’s Transfer Mechanics: Instant vs. Standard

Venmo offers two primary methods for moving money from your Venmo balance to your linked bank account or debit card. Each serves a different financial need and carries its own set of expectations regarding speed and cost.

The Standard Bank Transfer (1–3 Business Days)

The standard transfer is the default option for most users. It is a cost-effective way to move funds, as Venmo currently offers this service for free. These transfers are processed through the Automated Clearing House (ACH) network, which is the same system used for direct deposits and automated bill payments across the United States.

While Venmo initiates the transfer request almost immediately, the “1 to 3 business days” window is largely dependent on the communication between Venmo’s financial partner and your specific bank. If you initiate a transfer on a Monday morning, you can typically expect the funds to arrive by Wednesday or Thursday. However, because the ACH system does not process transactions on weekends or federal holidays, a transfer initiated on a Friday evening may not reflect in your bank account until the following Tuesday or Wednesday.

The Instant Transfer Feature (Minutes, for a Fee)

For those who require immediate liquidity, Venmo provides the “Instant Transfer” option. This feature allows users to send money to an eligible U.S. bank account or a supported Visa/Mastercard debit card within minutes. In most cases, the funds are available in the destination account in less than 30 minutes, though technical issues with the receiving bank can occasionally extend this to an hour.

The trade-off for this speed is a fee—typically 1.75% of the transfer amount, with a minimum fee and a maximum cap. For individuals managing tight budgets or businesses needing to pay a vendor immediately, this fee is often viewed as a necessary cost of doing business. From a personal finance perspective, it is a premium service for accelerated liquidity.

Factors That Influence Your Transfer Speed

While Venmo provides general timelines, several external and internal variables can influence exactly when your money becomes accessible. Being aware of these factors can help you avoid financial bottlenecks.

Bank Processing Times and Federal Holidays

The banking industry still operates on a legacy schedule that contrasts with the “always-on” nature of digital apps. Even if Venmo processes your request instantly, your bank may have specific “cutoff times.” If you initiate a standard transfer after your bank’s daily cutoff (often 2:00 PM or 5:00 PM local time), the bank may not begin processing it until the following business day.

Furthermore, federal holidays—such as Labor Day, Juneteenth, or Bank Holidays—completely halt the ACH cycle. When planning for month-end expenses, it is vital to account for these “dead days” in the banking calendar to ensure your transfers land when you need them.

Security Reviews and Account Verification

Venmo is a regulated financial service provider, meaning it must comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Occasionally, a transfer may take longer than the standard window because it has been flagged for a manual security review.

These reviews are more common if you are transferring a significantly larger amount than usual, if you are sending money to a new bank account, or if there is suspicious activity on your profile. While these delays can be frustrating, they are a necessary component of digital security, protecting both the user and the financial ecosystem from fraudulent transfers.

Weekend Bottlenecks and Clearing Cycles

One of the most common misconceptions in personal finance is that digital transfers are processed 24/7. While the request is digital, the clearing of funds is often batch-processed. Standard transfers initiated over the weekend will sit in a “pending” queue until the first business day of the week. For users who rely on Venmo for weekend gig-economy income, this means that a Saturday afternoon transfer might not be accessible until Tuesday morning.

Cost-Benefit Analysis: When to Pay for Speed

In the realm of personal finance, every fee matters. Deciding between a standard and an instant transfer requires a quick cost-benefit analysis of your current financial situation.

Calculating the 1.75% Fee

The current fee for an Instant Transfer is 1.75%, with a minimum of $0.25 and a maximum of $25. To put this into perspective:

- Transferring $100 costs $1.75.

- Transferring $1,000 costs $17.50.

- Transferring $5,000 costs the capped amount of $25.

If you are transferring $1,000, paying $17.50 just to have the money 48 hours earlier might not be the most efficient use of your capital unless you are facing a late fee on a bill that exceeds that amount. However, for a $5,000 transfer, the $25 cap makes the fee much more palatable as a percentage of the total (only 0.5%).

Alternatives for High-Volume Business Users

For those using Venmo for business, the accumulation of transfer fees can significantly eat into profit margins. Business owners should look into scheduling their transfers. By maintaining a “float” or a buffer in their business checking account, they can utilize the free 1–3 day standard transfer consistently, avoiding the need for instant transfers and saving hundreds of dollars in fees annually.

Security Protocols and Fund Safety During Transit

A frequent concern during the 1–3 day waiting period for a standard transfer is the safety of the funds. Once the money leaves your Venmo balance, it enters the “intermediary” stage of the banking system.

The Role of the Clearing House (ACH)

The ACH network is one of the most secure financial pipelines in the world. When you initiate a standard transfer, Venmo sends a digital instruction to its partner bank, which then batches that instruction with millions of others. This batch is sent to the Clearing House, which then routes the funds to your specific bank. This multi-step verification is why the process takes several days, but it is also why it is incredibly secure. The delay is effectively a “cooling-off” period that allows banks to verify that the funds exist and that the transaction is authorized.

What to Do if Your Transfer is Delayed

If a transfer exceeds the three-business-day window, the first step is to check your email for any notifications from Venmo regarding a “flagged” transaction or a request for additional identity verification. If no such request exists, the delay is likely on the receiving bank’s end. Some smaller credit unions or local banks have slower internal posting cycles than national institutions. Contacting your bank’s ACH department can often provide clarity on whether the funds are “pending” in their system.

Optimizing Your Personal Finance Workflow with Venmo

To master your money, you must master the tools you use to move it. Integrating Venmo effectively into your financial workflow requires a proactive approach to transfer times.

Best Practices for Cash Flow Management

The most successful strategy for using Venmo is the “Weekly Sweep.” Instead of transferring money every time you receive a small payment, let your balance accumulate and perform one standard transfer every Tuesday or Wednesday. This ensures the money arrives by Friday, providing you with liquidity for the weekend without ever having to pay an instant transfer fee.

Additionally, always maintain a small buffer in your linked bank account. If you know you have an automated rent payment coming out on the 1st of the month, you should initiate your Venmo transfer no later than the 25th of the previous month. This accounts for potential weekends, holidays, or unexpected security reviews.

Moving Funds Between Multiple Accounts

Many users now use Venmo as a bridge between different financial institutions. If you receive money on Venmo but want to move it to a high-yield savings account that isn’t directly linked, you must first transfer it to your primary checking account and then move it to the savings account. This “double hop” can take up to a week. For long-term financial health, ensure you are calculating these multi-step timelines to maximize the interest-earning potential of your money.

By understanding that a Venmo transfer is not just a button press but a coordinated movement across the legacy banking system, you can better manage your expectations and your wallet. Whether you choose the speed of an Instant Transfer or the cost-savings of a Standard Transfer, knowledge of the “how” and “how long” is the key to digital financial literacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.