When evaluating the cost of a Tesla, the sticker price is merely the starting point of a complex financial equation. For the modern consumer, purchasing a Tesla is less about buying a traditional vehicle and more about managing a high-tech asset that interacts uniquely with personal taxes, energy markets, and long-term maintenance budgets. In the realm of personal finance and smart investing, understanding the total cost of ownership (TCO) is essential to determining whether an electric vehicle (EV) fits your fiscal strategy.

As Tesla continues to fluctuate its pricing models to respond to market demand and manufacturing efficiencies, potential owners must look beyond the MSRP. This guide breaks down the multi-layered financial commitments of Tesla ownership, from initial capital outlay to the long-term ROI of going electric.

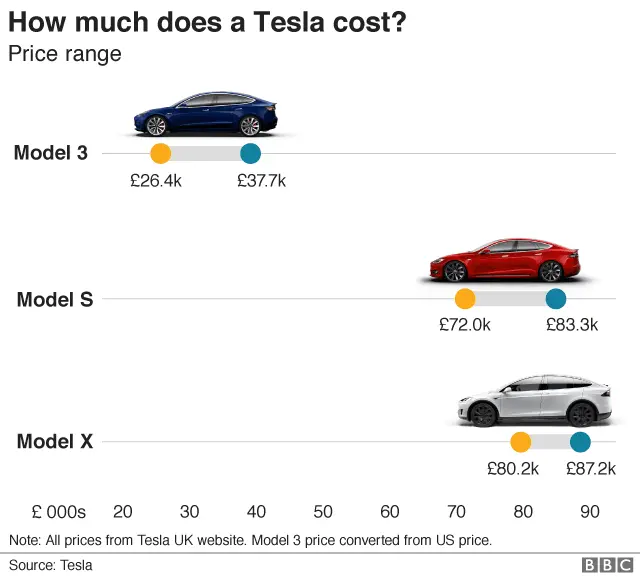

1. Navigating the Variable Pricing Landscape of Tesla Models

The first step in any significant financial acquisition is understanding the range of the initial investment. Tesla’s product lineup covers a broad spectrum, ranging from entry-level luxury sedans to high-performance SUVs. However, unlike traditional dealerships, Tesla utilizes a direct-to-consumer model with dynamic pricing that can change overnight.

Model 3 and Model Y: The Entry-Level Financial Commitments

The Model 3 and Model Y represent the most accessible points of entry for most buyers. As of the current market cycle, the Model 3 serves as the “budget-friendly” option, typically starting in the high-$30,000 to low-$40,000 range for the Rear-Wheel Drive (RWD) trim. For those requiring more utility, the Model Y—the world’s best-selling vehicle—usually commands a premium of $5,000 to $7,000 over the Model 3. From a personal finance perspective, these models offer the most aggressive depreciation hedges due to their high demand in the secondary market.

Model S and Model X: The Luxury Asset Tier

For high-net-worth individuals or those with significant business transportation budgets, the Model S and Model X represent the flagship tier. These vehicles typically start between $75,000 and $80,000, with “Plaid” performance variants exceeding $100,000. When investing at this level, the buyer is not just paying for a car but for cutting-edge air suspension, tri-motor powertrains, and prestige. However, from an investment standpoint, these higher-priced models often see steeper initial depreciation curves compared to their more affordable counterparts.

The Hidden Costs: Software and Customization

One must account for the “add-ons” that can inflate the final invoice. Tesla’s controversial Full Self-Driving (FSD) capability is a significant line item, often costing between $8,000 and $12,000 (or a monthly subscription fee). Additionally, premium paint colors, upgraded wheels, and interior configurations can easily add another $5,000 to the total. When calculating your loan-to-value ratio, it is vital to distinguish between functional hardware and software upgrades that may or may not retain value during a resale.

2. Tax Credits, Incentives, and Net Acquisition Costs

The actual cost of a Tesla is frequently lower than the price shown on the configurator, thanks to a complex web of government incentives. For the savvy financial planner, timing the purchase to maximize these benefits is key to reducing the net cost of the asset.

The Federal Clean Vehicle Credit

Under the Inflation Reduction Act (IRA), many Tesla models qualify for a $7,500 federal tax credit. However, this is not a universal discount. There are strict price caps—$55,000 for sedans and $80,000 for SUVs—and rigorous income limits for the buyer ($150,000 for individuals, $300,000 for joint filers). Effectively, this credit acts as an immediate equity boost, lowering the principal amount of a loan if applied at the point of sale.

State and Local Rebates

Beyond federal support, many states offer additional financial “carrots.” States like California, Colorado, and Massachusetts have historically offered rebates ranging from $1,500 to $5,000. Some utility companies also provide rebates for installing home charging stations. When these are stacked, the “true” price of a Model 3 can drop significantly, sometimes rivaling the cost of a mid-range internal combustion engine (ICE) vehicle like a Honda Accord or Toyota Camry.

Business Deductions and Section 179

For business owners and freelancers, a Tesla purchase can serve as a powerful tax shield. If the vehicle (particularly the heavier Model X) is used more than 50% for business purposes, it may qualify for accelerated depreciation under Section 179 or bonus depreciation. This allows business owners to deduct a significant portion of the purchase price in the first year, drastically altering the after-tax cost of the vehicle.

3. Operational Expenditures: Charging vs. Fueling

The most compelling financial argument for a Tesla is the shift from variable fuel costs to relatively stable electricity costs. This is where the long-term “profitability” of the purchase is realized.

The Electricity Arbitrage

On average, charging a Tesla at home costs significantly less than fueling a gasoline vehicle. While gas prices are subject to geopolitical volatility, residential electricity rates are generally more stable. For example, if gas is $3.50 per gallon and your ICE car gets 25 MPG, you spend $0.14 per mile. A Tesla Model 3 averaging 4 miles per kWh at an electricity rate of $0.15 per kWh costs roughly $0.04 per mile. Over 100,000 miles, this $0.10 per mile difference translates to $10,000 in direct savings.

Supercharging and Public Infrastructure

While home charging is the most cost-effective method, long-distance travel requires the Tesla Supercharger network. Supercharging is more expensive than home charging—often priced similarly to gasoline on a per-mile basis. For those who frequently travel long distances, the “fuel savings” diminish. It is essential to audit your driving habits to see if your geographic location and lifestyle allow for the maximum “electricity arbitrage.”

Insurance Premiums and the “Tesla Tax”

A critical, often overlooked cost in the “Money” niche is insurance. Teslas are frequently more expensive to insure than comparable ICE vehicles. This is due to high repair costs, the specialized nature of aluminum bodywork, and the high cost of sensor-laden components. Potential owners should obtain insurance quotes before purchasing, as an extra $500 to $1,000 per year in premiums can eat into the fuel savings mentioned above.

4. Maintenance, Longevity, and Resale Value

In traditional personal finance, a car is a depreciating liability. However, the maintenance profile of an EV differs drastically from a gasoline car, altering the long-term wealth impact.

Reduced Maintenance Schedules

Tesla vehicles have no oil changes, spark plugs, timing belts, or emissions checks. The regenerative braking system also significantly extends the life of brake pads and rotors. Aside from tires and cabin air filters, the first five years of Tesla ownership are remarkably low-cost. From a cash-flow perspective, this eliminates the “emergency repair” spikes that often plague older gasoline vehicles.

Battery Degradation and Long-Term Value

The most significant “risk” in the Tesla financial model is the battery. While Tesla guarantees its batteries for 8 years or 100,000 to 150,000 miles, the long-term health of the battery will dictate the car’s resale value. Data suggests that Tesla batteries retain about 90% of their capacity after 200,000 miles, which is promising for long-term equity. However, if a battery replacement is needed out of warranty, the cost can range from $10,000 to $20,000, effectively totaling the vehicle’s remaining value.

Market Volatility and Depreciation

Historically, Teslas held their value better than almost any other brand. However, recent aggressive price cuts by Tesla to maintain market share have caused a “repricing” in the used car market. For the investor-owner, this means the days of “flipping” a Tesla for a profit are over. Today, a Tesla should be viewed as a 5-to-10-year asset. The goal is to maximize the “utility value” of the car over its lifespan rather than relying on high residual value for a quick trade-in.

Conclusion: The Financial Verdict

So, how much does a Tesla car cost? The answer is not a single number but a financial trajectory. While the initial capital requirement remains high—typically between $40,000 and $100,000—the net cost is mitigated by federal tax credits, significant operational savings, and a simplified maintenance schedule.

For a person with a high annual mileage and the ability to charge at home, a Tesla often presents a lower Total Cost of Ownership than a gasoline car with a lower sticker price. However, for those with low mileage or high insurance brackets, the “Tesla Premium” may take much longer to recoup. Ultimately, buying a Tesla is a move away from the “pay-as-you-go” model of gasoline and repairs toward a “front-loaded” investment model. If you have the liquidity to handle the higher purchase price or the credit to secure a low-interest loan, the long-term financial benefits of the Tesla ecosystem remain a compelling case for the modern, budget-conscious driver.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.