The prospect of a “no tax on tips” policy has rapidly shifted from a fringe economic theory to a central pillar of modern American fiscal discourse. For millions of service industry workers—ranging from restaurant servers and bartenders to hair stylists and rideshare drivers—the potential for tax-exempt gratuities represents a monumental shift in personal finance. However, as with all significant changes to the internal revenue code, the transition from a campaign promise to a tangible line item on a tax return is a complex journey fraught with legislative hurdles and economic debate.

To understand when such a policy might go into effect and how it would impact the financial landscape, one must look beyond the headlines and examine the mechanics of federal tax law, the current legislative environment, and the projected economic consequences.

The Legislative Landscape: From Campaign Promise to Federal Law

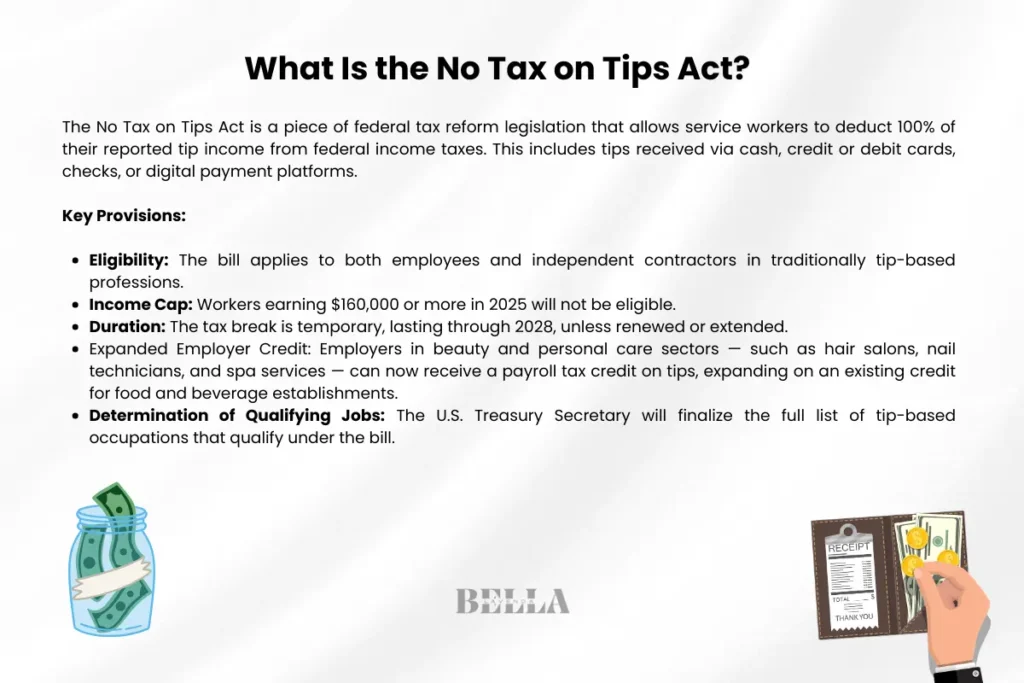

The concept of eliminating federal income tax on tips gained significant momentum during the 2024 election cycle. While the proposal has received bipartisan interest, it is currently in the “legislative proposal” stage. This means that, as of today, tips remain fully taxable under federal law. For this policy to go into effect, it must navigate the rigorous process of the U.S. Congress.

The Origin and Momentum of the “No Tax on Tips” Movement

The movement is rooted in the idea of providing immediate relief to low-to-middle-income earners. Proponents argue that tips are a unique form of income—often unpredictable and supplementary—and that taxing them places an undue burden on those in the service sector. Unlike a standard salary, tips are a direct gift from a customer for service rendered, and advocates suggest that exempting them would stimulate local economies by putting more liquid capital directly into the hands of consumers.

The Congressional Hurdle: The “No Tax on Tips Act”

For any change in tax law to occur, a bill must be introduced, passed by both the House of Representatives and the Senate, and signed by the President. Several versions of a “No Tax on Tips Act” have been discussed or introduced in preliminary forms. The timeline for implementation depends heavily on the composition of the next Congress. If a unified government prioritizes this in a 2025 legislative session, the earliest we could see a change in withholding would likely be for the 2025 or 2026 tax year. However, if the bill faces gridlock or requires extensive amendments to address budget deficits, the timeline could extend several years into the future.

Financial Impact for Service Industry Workers

If a “no tax on tips” policy is enacted, the immediate impact on personal finance for tipped employees would be profound. Currently, tipped employees are required to report 100% of their gratuities to their employers, who then withhold federal income tax, Social Security, and Medicare taxes (FICA) based on that total.

Federal Income Tax vs. Payroll Tax (FICA)

One of the most critical distinctions in the current proposals is whether the exemption applies only to federal income tax or also to payroll taxes. If the policy only eliminates federal income tax, workers would still see deductions for Social Security and Medicare. This is a vital point for financial planning: Social Security benefits in retirement are calculated based on your taxed earnings. If tips are exempt from payroll taxes, workers might see higher take-home pay today but lower social security checks in the future. Financial analysts suggest that a balanced policy might exempt the income tax while maintaining the payroll tax to protect the long-term solvency of the social safety net.

Projected Increase in Take-Home Pay

For a worker earning $20,000 a year in tips, the elimination of federal income tax could result in an annual savings of $2,000 to $5,000, depending on their total income bracket and deductions. This increase in disposable income represents a “pay raise” that doesn’t come from the employer’s pocket, potentially reducing the pressure on small businesses to raise base wages in an inflationary environment. For the individual, this extra cash flow could be the difference between living paycheck to paycheck and being able to contribute to a high-yield savings account or an emergency fund.

Macroeconomic Consequences and the Federal Deficit

![]()

While the microeconomic benefits to the worker are clear, the broader financial implications for the U.S. economy are a subject of intense scrutiny by the Congressional Budget Office (CBO) and independent fiscal watchdogs.

The Cost of Implementation: Budget Projections

Taxing tips generates billions of dollars in federal revenue annually. Removing this revenue stream creates a “tax gap” that must be accounted for. Estimates suggest that a full exemption of tips from federal income tax could cost the Treasury between $150 billion and $250 billion over a decade. In a time of rising national debt, economists are debating whether the economic stimulus provided by increased consumer spending will be enough to offset the loss in direct tax revenue.

Potential Shifts in Compensation Structures

A significant concern for the business finance world is the “reclassification risk.” If tips become tax-free, there is a strong financial incentive for both employers and employees to shift as much compensation as possible into the “tip” category. We might see industries that traditionally use flat salaries—such as consulting or legal services—attempting to restructure their fees as “gratuities” to avoid taxation. This would lead to “tax base erosion,” where the government loses revenue from sectors far beyond the service industry. To prevent this, any legislation would need strict definitions of what constitutes a “tip” versus a “service fee” or “commission.”

Implementation Challenges and Regulatory Oversight

Even if the law is passed tomorrow, the operational shift for businesses and the Internal Revenue Service (IRS) would be massive. The transition period would require new reporting standards and updated payroll software.

Defining “Tips” to Prevent Tax Loopholes

From a regulatory standpoint, the IRS would need to establish clear, airtight definitions. Is a mandatory 18% gratuity for large parties a “tip” or a “service charge”? Currently, the IRS views mandatory service charges as regular wages, not tips. If tips become tax-exempt, the distinction becomes a multi-billion dollar question. Business owners would need to audit their point-of-sale (POS) systems and accounting practices to ensure they are compliant with the new definitions to avoid heavy penalties or audits.

The Role of the IRS in Enforcing New Guidelines

The IRS has historically struggled with “tip underreporting,” particularly in cash-heavy environments. A “no tax on tips” policy might actually encourage more accurate reporting, as there would no longer be a financial penalty for disclosing the full amount of gratuities earned. However, the agency would still need to monitor for “income shifting,” where high-earning executives might attempt to label bonuses as tips. This would necessitate a new era of tax enforcement and perhaps an increase in the number of auditors focusing on small-to-medium-sized business payrolls.

Strategic Financial Planning for a Post-Tax Tip Era

For individuals working in the service sector, the prospect of tax-exempt tips requires a proactive approach to personal finance. If and when this policy goes into effect, it shouldn’t just be seen as extra spending money, but as a tool for long-term wealth building.

Adjusting Withholding and Tax Liability

If tips become exempt, workers who also have a secondary source of income (such as a W-2 day job or investment income) will need to carefully recalibrate their tax withholdings. The sudden shift in taxable income could change their tax bracket or eligibility for certain credits, like the Earned Income Tax Credit (EITC). Consulting with a financial advisor or using professional tax software will be essential to ensure that the “tax-free” status of tips doesn’t inadvertently lead to an underpayment of taxes on other income sources.

Long-term Savings and Retirement Planning

The greatest opportunity presented by a “no tax on tips” policy is the ability to accelerate retirement savings. If a worker saves 15% to 20% more of their income due to tax exemptions, that capital can be diverted into a Roth IRA or a 401(k). Because tips are often paid out daily or weekly, setting up an automated transfer from a checking account to a brokerage account can turn the tax savings into a compounded nest egg. In the “Money” niche, the consensus is clear: the most successful individuals aren’t just those who earn more, but those who strategically manage the “spread” between their gross income and their tax liability.

In conclusion, while the “no tax on tips” policy is not yet in effect, its potential implementation marks a significant milestone in fiscal policy. The timeline rests in the hands of the legislative branch, likely beginning in the 2025 session. For the savvy service worker or business owner, staying informed on these developments is not just about following the news—it’s about preparing for a fundamental shift in how income is earned, reported, and invested in the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.