Tax season is often met with a sense of dread, but it is also one of the most critical periods for personal financial management. Understanding how to lower your taxable income is not about evasion; it is about tax avoidance—the legal application of the tax code to minimize your liability and maximize your net worth. By lowering your Adjusted Gross Income (AGI), you not only pay less to the government but often qualify for additional credits and deductions that are phased out at higher income levels.

Effectively managing your tax burden requires a proactive, year-round approach. From leveraging retirement accounts to understanding the nuances of investment losses, this guide explores the most effective strategies to shield your hard-earned money from excessive taxation.

1. Maximizing Contributions to Tax-Advantaged Retirement Accounts

The most direct way to lower your taxable income is to divert money into “pre-tax” retirement accounts. When you contribute to these accounts, the IRS essentially ignores that portion of your income for the current tax year.

The Power of 401(k) and 403(b) Plans

For most employees, the 401(k) (for-profit) or 403(b) (non-profit) is the primary tool for tax reduction. As of 2024, the contribution limit is $23,000, with an additional $7,500 catch-up contribution for those aged 50 and older. If you earn $100,000 and contribute the maximum $23,000, your taxable income immediately drops to $77,000. This shift can sometimes move you into a lower tax bracket entirely, providing immediate relief.

Traditional IRAs and Eligibility

While Roth IRAs are excellent for tax-free growth, they do not lower your current taxable income because contributions are made with after-tax dollars. To lower your current bill, you must look toward a Traditional IRA. Contributions to a Traditional IRA may be tax-deductible depending on your income level and whether you or your spouse are covered by a retirement plan at work. It is a vital tool for those who may not have access to an employer-sponsored plan.

Specialized Accounts for the Self-Employed

If you are a freelancer, consultant, or small business owner, your options for lowering taxable income are even more robust. Tools like the Simplified Employee Pension (SEP) IRA or the Solo 401(k) allow for much higher contribution limits than standard individual accounts. For a Solo 401(k), you can contribute as both the employer and the employee, potentially shielding upwards of $69,000 (plus catch-up contributions) from taxes in a single year, significantly reducing your business’s taxable profit.

2. Leveraging Health and Education Savings Vehicles

Beyond retirement, the tax code provides several “pockets” where you can store money for specific life expenses while simultaneously reducing your taxable income.

The Triple Tax Advantage of HSAs

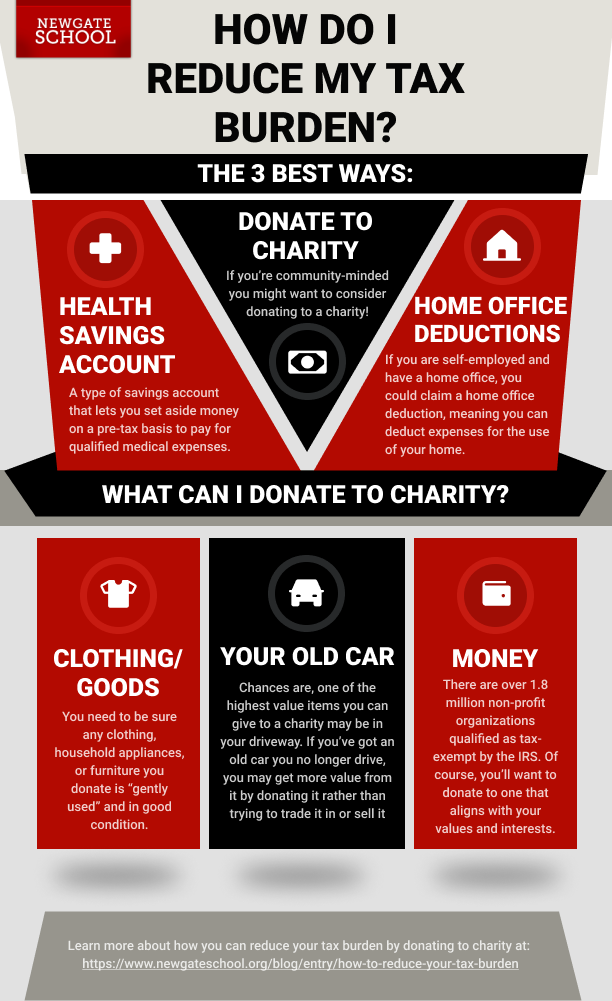

The Health Savings Account (HSA) is widely considered the most tax-efficient vehicle in the American financial system. To qualify, you must be enrolled in a High Deductible Health Plan (HDHP). The HSA offers a “triple tax advantage”:

- Contributions are 100% tax-deductible (or made pre-tax through payroll), lowering your taxable income.

- The money grows tax-free through investments.

- Withdrawals for qualified medical expenses are tax-free.

Unlike a Flexible Spending Account (FSA), the money in an HSA rolls over every year, making it a powerful long-term wealth-building tool that slashes your tax bill today.

Flexible Spending Accounts (FSAs)

If you do not have an HDHP, you likely have access to an FSA. This allows you to set aside pre-tax dollars for healthcare or dependent care (childcare) expenses. While these are usually “use it or lose it” accounts, they provide an immediate reduction in your taxable income. For parents, the Dependent Care FSA is particularly potent, allowing up to $5,000 to be excluded from taxable income to pay for daycare or after-school programs.

529 Plans and State Tax Deductions

While 529 college savings plans use after-tax dollars at the federal level, many states offer a state income tax deduction or credit for contributions. While this doesn’t lower your federal taxable income, it can significantly lower your state-level liability, keeping more money in your family’s pocket for future education costs.

3. Strategic Itemized Deductions and Charitable Giving

Every taxpayer must choose between taking the standard deduction or itemizing their deductions on Schedule A. To lower your taxable income below the standard deduction threshold, you must find enough “qualified” expenses to make itemizing worthwhile.

The “Bunching” Strategy for Charitable Contributions

Charitable giving is a cornerstone of tax planning. However, with the standard deduction being relatively high, individual annual donations may not always provide a tax benefit. “Bunching” is a strategy where you combine two or more years’ worth of planned donations into a single tax year. By doing this, you exceed the standard deduction threshold in the “on” year, significantly lowering your taxable income, and then take the standard deduction in the “off” years.

Donor-Advised Funds (DAFs)

A Donor-Advised Fund is a specialized financial account that allows you to make a charitable contribution and receive an immediate tax deduction, but then recommend grants from the fund to charities over time. This is an excellent tool for someone who has a high-income year (perhaps due to a bonus or the sale of a business) and needs to lower their taxable income significantly and quickly without rushing the decision of which charities to support.

Mortgage Interest and State and Local Taxes (SALT)

For homeowners, the mortgage interest deduction remains a primary way to lower taxable income. Additionally, taxpayers can deduct up to $10,000 of state and local taxes (the SALT deduction), which includes property taxes and either state income taxes or sales taxes. When combined with charitable giving, these deductions often make it beneficial to itemize, further eroding the amount of income subject to federal tax.

4. Investment Strategies: Tax-Loss Harvesting and Capital Gains

Your investment portfolio is not just a tool for growth; it is also a tool for tax management. The way you realize gains and losses can have a massive impact on your final tax bill.

Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that are currently at a loss to offset capital gains realized elsewhere in your portfolio. If your losses exceed your gains, you can use the excess to offset up to $3,000 of your ordinary income (like your salary). Any remaining losses can be carried forward to future years. This is a sophisticated way to “find” deductions in a volatile market.

Holding for Long-Term Capital Gains

The duration for which you hold an asset changes how it is taxed. Assets held for less than a year are taxed at ordinary income rates (up to 37%). Assets held for more than a year are taxed at long-term capital gains rates, which are significantly lower (0%, 15%, or 20% depending on income). By strategically waiting to sell assets until the one-year mark, you lower the “effective” tax on your income, even if the gross income remains the same.

Municipal Bonds for Tax-Exempt Interest

For investors in high tax brackets, municipal bonds (issued by states or cities) offer a unique advantage: the interest earned is usually exempt from federal income tax and, in many cases, state and local taxes as well. While the nominal interest rate might be lower than corporate bonds, the “tax-equivalent yield” is often higher because none of that income is chipped away by the IRS.

5. Maximizing Business Expenses and the QBI Deduction

In the modern economy, many individuals have side hustles or small businesses. This opens up a new realm of “above-the-line” deductions that lower your AGI directly.

The Home Office and Business Expense Deductions

If you are self-employed, every legitimate business expense reduces your taxable income dollar-for-dollar. This includes a portion of your home (the home office deduction), equipment, marketing, and professional development. Proper record-keeping is essential here; by meticulously tracking expenses, you ensure that you aren’t paying taxes on money that was actually a cost of doing business.

The Qualified Business Income (QBI) Deduction

Created by the Tax Cuts and Jobs Act, the QBI deduction allows many sole proprietors, partners, and S-corporation owners to deduct up to 20% of their qualified business income from their taxes. This is a “below-the-line” deduction that can significantly lower the taxable income of small business owners without requiring any actual cash outlay.

Conclusion: The Importance of Proactive Planning

Lowering your taxable income is a multifaceted endeavor that touches every corner of your financial life—from how you save for retirement to how you manage your investments and your business. The most effective strategies are those implemented long before the December 31st deadline. By understanding the mechanics of AGI and utilizing the various credits and deductions provided by the tax code, you can ensure that you are paying your fair share—but not a penny more. Always consult with a qualified tax professional or financial advisor to ensure these strategies align with your specific financial situation and the latest IRS regulations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.