In the modern landscape of personal finance, the ability to move money efficiently and securely is paramount. Whether you are setting up a direct deposit for a new job, paying your monthly rent through an online portal, or initiating a wire transfer to an investment account, you will inevitably encounter a request for two specific pieces of information: your account number and your routing number.

While most people are familiar with their account number—the unique identifier for their specific funds—the routing number often remains a bit of a mystery. Knowing exactly where to find your routing number and understanding its function is a fundamental skill in financial literacy. This guide will walk you through the various ways to locate this number, the logic behind its structure, and how to use it safely within the digital banking ecosystem.

Understanding the Routing Number: More Than Just a String of Digits

To manage your money effectively, it is helpful to understand what a routing number actually is. Formally known as an ABA Routing Transit Number (RTN), this nine-digit code acts as a specialized “address” for financial institutions.

What is an ABA Routing Number?

The system was developed by the American Bankers Association (ABA) in 1910. Its original purpose was to facilitate the physical sorting and shipment of paper checks. Today, in our digital-first world, it serves as the primary way the Federal Reserve and electronic payment networks identify which bank is responsible for a transaction. Every bank and credit union in the United States has at least one routing number assigned to it. Larger institutions may even have multiple routing numbers based on the geographic region where the account was opened or the specific type of transaction being processed.

Why Your Routing Number Matters for Your Finances

The routing number is the backbone of the United States payment system. Without it, the “plumbing” of our financial world would fail. It is required for:

- Direct Deposits: Ensuring your paycheck or government benefits land in the correct bank.

- Automatic Bill Pay: Allowing utility companies or mortgage lenders to pull funds directly from your institution.

- ACH Transfers: Moving money between different banks, such as transferring funds from a traditional savings account to a high-yield online savings account.

- Tax Refunds: The IRS requires both your routing and account numbers to issue electronic refunds.

Top 5 Ways to Locate Your Routing Number Quickly

If you find yourself in the middle of a financial application and need your routing number immediately, there are several reliable places to look. Depending on whether you prefer physical documents or digital tools, you can find this information in seconds.

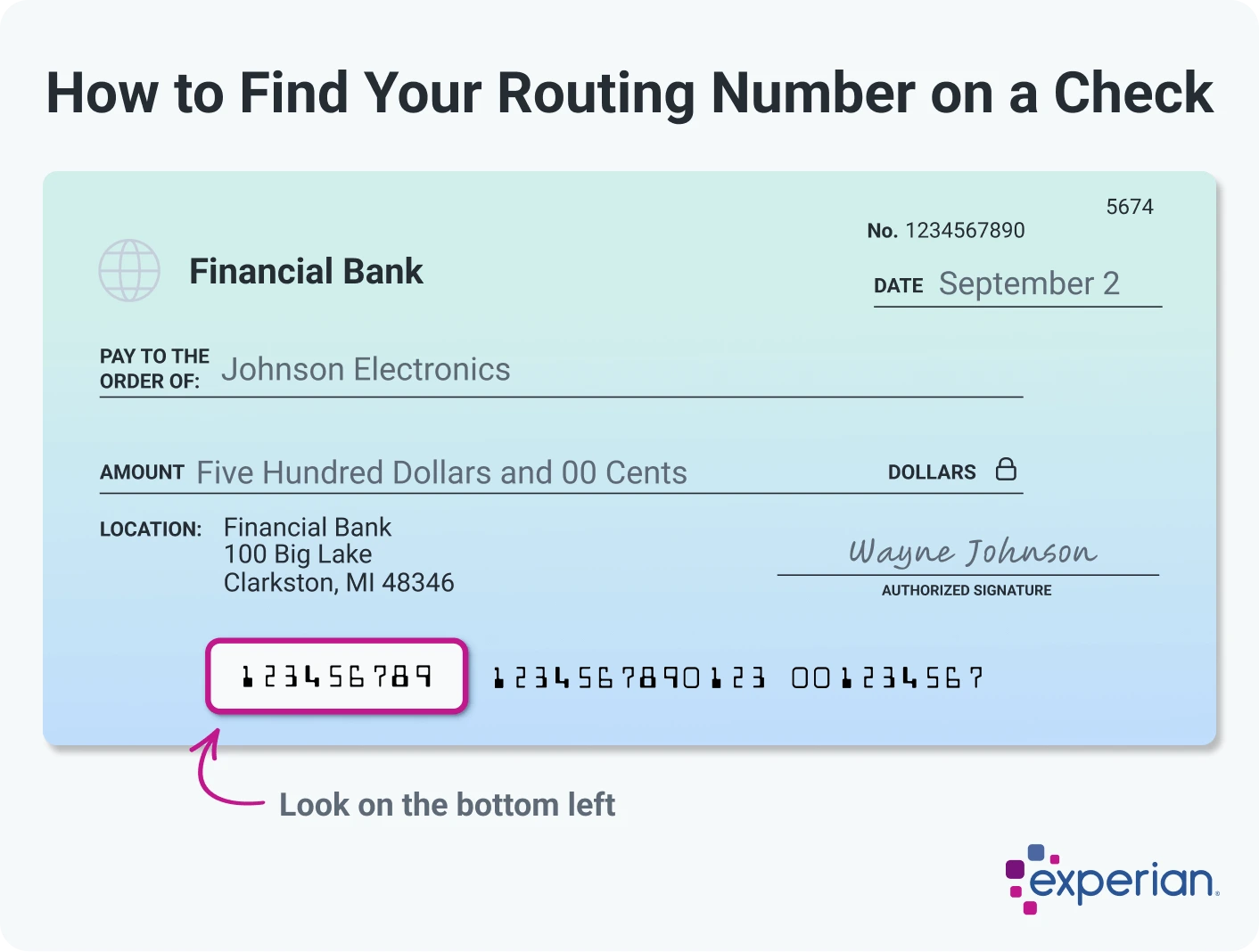

The Physical Check: The Most Traditional Method

If you still use a physical checkbook, finding your routing number is incredibly straightforward. If you look at the bottom of one of your checks, you will see a string of numbers printed in a specialized font known as MICR (Magnetic Ink Character Recognition).

- The Routing Number: This is almost always the first set of nine digits on the far left. It is flanked by a specific symbol that looks like a colon and a dash.

- The Account Number: This is usually the second set of numbers in the center.

- The Check Number: This is the shortest set of numbers, typically found on the far right, matching the number in the top right corner of the check.

Mobile Banking Apps and Online Portals

In the era of “Money Tech,” most consumers have moved away from paper checks. Fortunately, your routing number is easily accessible through your bank’s digital interface. Once you log in to your mobile app or online banking dashboard:

- Navigate to Account Details: Click on the specific checking or savings account you wish to use.

- Look for “Account Info” or “Details”: Most apps have a “Show Details” or an “i” icon that will reveal both your full account number and the routing number.

- Search Features: Many modern banking apps have a search bar. Simply typing “routing number” into the help or search section will often trigger a pop-up with the necessary digits.

Bank Statements and Official Correspondence

Your monthly bank statement—whether received via mail or downloaded as a PDF—is a legal document that contains all your pertinent financial identifiers. Look at the top of the first page, near your name and address. You will typically find a summary section that lists the account type, the partial account number, and the full nine-digit routing number.

Differentiating Between Routing and Account Numbers

One of the most common hurdles in personal finance management is the confusion between the routing number and the account number. Getting these mixed up can lead to rejected payments, late fees, or even funds being sent to the wrong person.

Common Mistakes to Avoid

A frequent error occurs when individuals assume their debit card number is their account number. In reality, the sixteen-digit number on your plastic card is a separate identifier used specifically for the Visa or Mastercard payment networks. It is not used for ACH transfers or direct deposits.

Another common mistake is using a routing number from an old checkbook after a bank merger. If your bank was acquired by a larger institution, your routing number likely changed. Always ensure you are using the most current information provided by your bank to avoid transaction failures.

When to Use Which Number

Think of the routing number as the “Zip Code” and the account number as the “Street Address.”

- The Routing Number tells the financial system: “Go to Bank of America in the California region.”

- The Account Number tells the system: “Once you are at that bank, put this money into John Doe’s specific bucket.”

When setting up a side hustle on a platform like Etsy or Shopify, or setting up a personal brokerage account at a firm like Vanguard or Fidelity, you will always be asked for both. The routing number identifies the “where,” and the account number identifies the “who.”

Security and Best Practices in the Digital Banking Age

Because the combination of your routing and account numbers can be used to withdraw funds, protecting this information is a critical component of your digital financial security.

Keeping Your Financial Information Safe

While your routing number is technically public information (anyone can look up a bank’s routing number online), your account number is private. When combined, they provide a direct line to your cash.

- Avoid Public Wi-Fi: Never log in to your banking portal to find your routing number while on an unsecured public network.

- Be Wary of Phishing: Your bank will never call or text you asking for your routing and account numbers. They already have that information.

- Shred Old Documents: If you find old checks or bank statements while cleaning, ensure they are shredded. Simply tossing them in the trash leaves you vulnerable to identity theft.

What to Do if Your Information is Compromised

If you suspect that your banking details have been leaked, the first step is to contact your financial institution’s fraud department. In many cases, they will need to close the existing account and issue a new account number. While your routing number will remain the same (as it is tied to the bank, not you), the new account number will act as a fresh start, cutting off any unauthorized access.

Specialized Routing Numbers: International and Wire Transfers

As you progress in your financial journey, you may find that a standard nine-digit routing number isn’t enough. Certain transactions require specialized codes.

Domestic vs. International Transfers (SWIFT/BIC)

The ABA routing number is a United States-specific system. If you are receiving money from an employer in Europe or sending a gift to a relative in Asia, the routing number will not work. Instead, you will need a SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or a BIC (Bank Identifier Code). These are 8 to 11 characters long and identify banks on a global scale.

Why Wire Transfers Often Require a Different Number

Many people are surprised to learn that their “ACH routing number” is different from their “Wire routing number.”

- ACH (Automated Clearing House): Used for standard transactions like direct deposits and bill payments. These usually take 1–3 business days.

- Wire Transfers: Used for large, immediate transactions, such as a down payment on a house.

Banks often use a separate, dedicated routing number for wire transfers to ensure they are processed through the high-speed “Fedwire” system. Before initiating a wire, always check your bank’s website specifically for their “Wire Transfer Routing Number” to ensure the funds are not delayed.

By mastering these small but significant details of banking, you place yourself in a much stronger position to manage your wealth. The routing number may seem like a trivial string of digits, but it is the essential key that unlocks the fluidity of your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.