In the modern era of digital banking, the tools we use to manage our personal finances have become increasingly streamlined. However, this convenience often brings about a layer of confusion regarding the technical details of our accounts. One of the most common questions individuals ask when setting up direct deposits or making online payments is: “Where is the routing number on my debit card?”

The short answer is that, in almost all cases, a routing number is not printed on a physical debit card. While your debit card is a vital key to accessing your funds, it serves a different functional purpose than the routing and account numbers that identify your financial institution. Understanding the distinction between these identifiers is crucial for effective personal finance management, ensuring that your transactions are processed accurately and securely.

Demystifying Financial Identifiers: Routing Numbers vs. Debit Card Numbers

To navigate the world of personal finance effectively, one must understand the specific roles of the various numbers associated with a bank account. A common misconception among new account holders is that the long string of digits on the front or back of a debit card is the only information needed for all types of transactions.

What Exactly is a Routing Number?

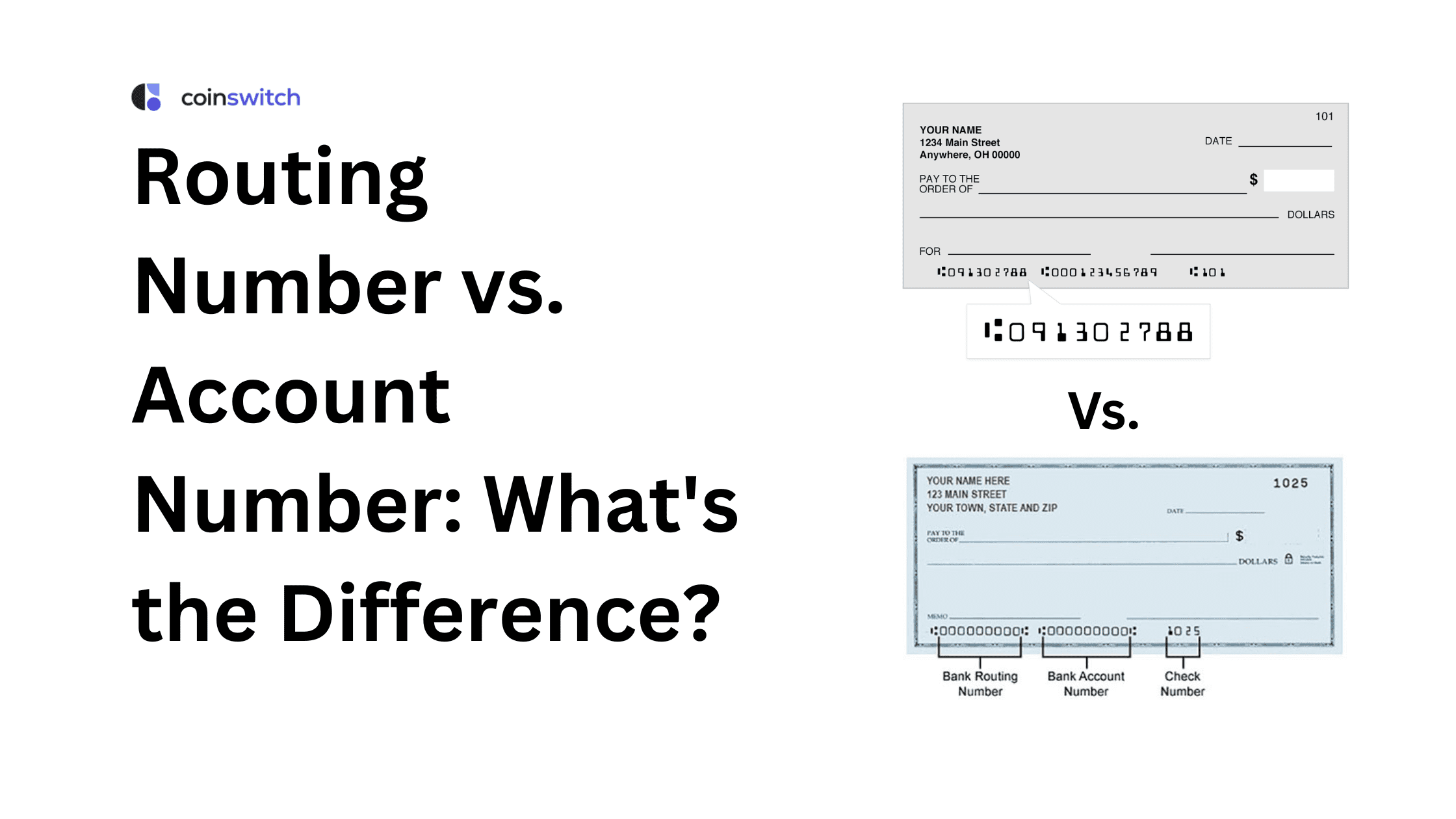

A routing number, often referred to as an ABA (American Bankers Association) routing transit number (RTN), is a nine-digit code used to identify a specific financial institution within the United States. Established in 1910, this system was designed to facilitate the sorting and shipment of paper checks. Today, it serves as the primary address for electronic transactions.

The nine digits are not random; they represent the Federal Reserve bank or processing center that services the institution, the bank itself, and a check digit used for verification. In the context of “money” management, the routing number tells the financial system exactly where to “route” the funds during a transfer.

The Anatomy of a Debit Card

A debit card is a transactional tool linked to a checking or savings account. The primary number on the card—usually 16 digits—is the Permanent Account Number (PAN). This number is unique to the piece of plastic (or the digital wallet entry) and is used primarily for point-of-sale transactions and online shopping through credit card processing networks like Visa or Mastercard.

In addition to the card number, you will find an expiration date and a CVV (Card Verification Value) security code. While these are essential for “pulling” money from your account during a purchase, they do not identify the bank in the same way a routing number does.

Why Your Routing Number is Rarely Printed on Your Card

The reason routing numbers are absent from debit cards is rooted in both security and functionality. A debit card is a replaceable tool; if you lose it, the bank issues a new card with a new 16-digit number, but your underlying bank account remains the same.

The routing number and your personal account number are the foundational “address” of your money. If these were printed on every debit card, a lost card would not only compromise your ability to make card transactions but would also expose your primary banking coordinates, making it easier for bad actors to attempt unauthorized ACH (Automated Clearing House) transfers or forge checks.

The Functional Role of Routing Numbers in Personal Finance

While your debit card is your go-to for daily spending, the routing number is the backbone of your broader financial life. It is the silent engine behind the scenes of most significant financial movements.

Facilitating Direct Deposits and Automatic Payments

For most employees, the most important use of a routing number is the setup of direct deposit. When you provide your employer with your routing and account numbers, you are essentially providing a roadmap for your paycheck to travel from the corporate treasury to your personal balance.

Similarly, routing numbers are essential for “recurring wealth” management. When you set up automatic transfers to a high-yield savings account or an investment brokerage, the system uses the routing number to ensure the money moves between the correct institutions. This is a “push” or “pull” mechanism that bypasses the debit card networks entirely, often resulting in lower fees and higher reliability for large sums.

Domestic Wire Transfers and ACH Payments

In the realm of business finance and personal real estate transactions, routing numbers are indispensable. For example, when paying a mortgage or making a down payment, a wire transfer is often required. A wire transfer requires the bank’s routing number to ensure the funds arrive instantly and securely.

ACH payments—the system used for utility bills, insurance premiums, and peer-to-peer transfers (like those found in some older banking apps)—also rely on the routing number. Understanding this distinction helps you choose the right tool for the job: use the debit card for the grocery store, but use the routing number for your monthly rent or mortgage.

The Importance of Accuracy in Financial Transactions

In personal finance, a single digit can be the difference between a successful investment and a logistical nightmare. Because routing numbers are part of a closed system, entering an incorrect digit can result in a “returned” transaction, which often incurs a fee from both the sending and receiving institutions.

Unlike a debit card transaction, which is approved or declined in real-time, ACH and wire transfers based on routing numbers can take hours or days to process. If the information is incorrect, your money could be held in “suspense” accounts, delaying essential payments like credit card bills or loan installments.

How to Locate Your Routing Number Without a Physical Check

Since the routing number isn’t on your debit card, you might wonder where to find it, especially if you belong to the growing demographic that no longer carries a physical checkbook. Fortunately, modern financial tools make this information readily available.

Utilizing Online Banking and Mobile Apps

The fastest way to find your routing number is through your bank’s mobile app or online portal. Once you log in, navigate to the “Account Details” or “Summary” section of your checking account. Most banks will display the routing number alongside your account number.

Some banks even provide a “Direct Deposit” tab that generates a pre-filled PDF form containing all the necessary routing information. This is a highly secure way to retrieve the data, as it ensures you are looking at the official numbers provided by the institution.

Checking Your Monthly Bank Statements

For those who prefer a paper trail or digital documents, monthly bank statements are an excellent resource. Your statement will typically list the routing number in the header or the account information summary at the top of the first page. Keeping a digital copy of your most recent statement on a secure drive is a good personal finance habit, as it provides a quick reference for these numbers when you are offline.

Contacting Customer Support and Official Bank Websites

If you are unable to access your app or statements, most banks list their routing numbers publicly on their official websites. Since routing numbers identify the institution, not the individual person, they are not considered private information in isolation.

However, be cautious: large national banks often have different routing numbers for different states or different types of transactions (e.g., one for paper checks and another for electronic wires). Always ensure you are looking at the routing number specific to your region and account type.

Security Protocols: Protecting Your Account and Routing Information

Because the combination of a routing number and an account number provides direct access to the “source” of your funds, protecting this information is a cornerstone of financial security.

Recognizing Common Financial Fraud Tactics

Phishing is the most common threat. Scammers may send emails or texts posing as your bank, asking you to “verify” your routing and account numbers. It is important to remember that your bank already has this information; they will never ask you to provide it via an unsecured link.

Another risk is “check washing,” where criminals steal paper checks from mailboxes and use chemicals to erase the payee and amount, leaving the routing and account numbers intact at the bottom. This is one reason why many financial experts recommend using electronic transfers and routing numbers via secure portals rather than mailing physical checks.

Best Practices for Sharing Your Banking Details

When you must share your routing and account numbers—such as for a new job or to set up a utility—only do so through secure, encrypted portals. Avoid sending these numbers via standard email or text messages. If you are setting up a payment over the phone, ensure you are the one who initiated the call to a verified, official number for the company in question.

What to Do if Your Information is Compromised

If you suspect that your routing and account numbers have fallen into the wrong hands, the response is different than if you simply lost your debit card. While a lost debit card can be “frozen” and replaced in minutes, a compromised account/routing pair usually requires closing the entire bank account and opening a new one.

This is a significant undertaking, as it involves redirecting all direct deposits and updating every automatic bill payment. Therefore, maintaining a high level of vigilance over who has access to these numbers is a vital part of protecting your overall financial health.

In conclusion, while the search for a routing number on a debit card may lead to a dead end, the journey reveals the sophisticated structure of our financial system. Your debit card is your tool for the present—for the daily coffee and the weekend errands. Your routing number is your tool for the future—for the paychecks, the investments, and the long-term bills that build your financial foundation. By understanding the roles of each, you can manage your money with greater confidence, precision, and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.