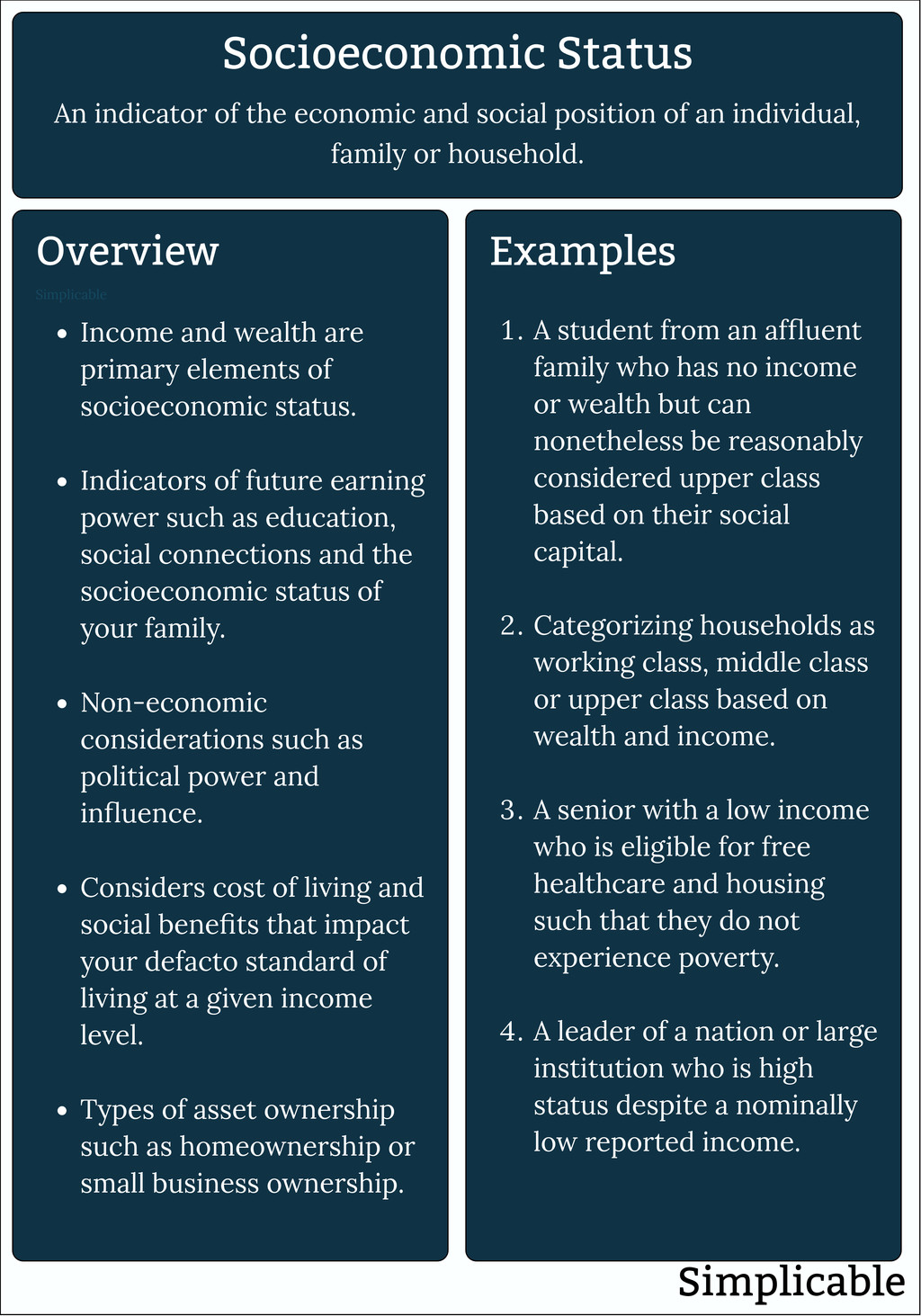

Socio-economic status (SES) is often discussed in sociological circles, but its most profound impact is felt within the realm of personal finance and wealth management. At its core, socio-economic status is a combined total measure of a person’s work experience and of an individual’s or family’s economic and social position in relation to others. In the world of money, understanding SES is not just about identifying where one stands on the ladder; it is about recognizing the systemic factors, psychological influences, and financial opportunities that define one’s ability to build, maintain, and transfer wealth.

For the modern investor or professional, SES serves as a baseline for financial behavior. It dictates risk tolerance, access to capital, and the quality of financial education one receives. To truly master one’s finances, one must first deconstruct the components of socio-economic status and understand how these variables interact with the global market.

Defining the Metrics: The Pillars of Socio-Economic Status

Socio-economic status is traditionally measured by three primary variables: income, education, and occupation. While these factors are interconnected, each plays a distinct role in shaping an individual’s financial trajectory.

Income vs. Net Worth: More Than Just a Paycheck

In the context of money, income is the most visible marker of SES. It represents the flow of resources—wages, salaries, profits, and rents. However, a high income does not automatically equate to a high socio-economic status if it is not converted into net worth. Net worth, or the sum of all assets minus liabilities, is the truer measure of economic stability. High-SES individuals often focus on asset accumulation (stocks, real estate, business equity) rather than just high-consumption lifestyles. Understanding this distinction is the first step in moving from a cycle of “earning to spend” to “earning to invest.”

Educational Attainment: The ROI of Knowledge

Education is frequently cited as the most significant predictor of long-term financial success. From a “Money” niche perspective, education is an investment in human capital. It provides the specialized skills necessary to command higher wages and the critical thinking skills required to navigate complex financial markets. Higher levels of education often correlate with higher financial literacy—the ability to understand how money works, how to manage it, and how to invest it wisely. This “knowledge ROI” (Return on Investment) creates a compounding effect over a lifetime, as educated individuals are generally more adept at leveraging tax advantages and compound interest.

Occupational Prestige and Stability

The nature of one’s work influences SES through both income level and social capital. Professional occupations often come with benefits that go beyond a salary, such as employer-sponsored retirement plans, stock options, and comprehensive insurance. These “hidden” financial perks significantly bolster a person’s socio-economic standing by reducing out-of-pocket costs and accelerating wealth building. Furthermore, certain occupations provide networking opportunities—social capital—that can lead to exclusive investment deals or business partnerships that are unavailable to those in lower-SES brackets.

The Financial Lifecycle: How SES Influences Wealth Accumulation

Socio-economic status does not just describe where you are; it influences how you move forward. The financial lifecycle of an individual is heavily dictated by their SES, affecting everything from their first bank account to their estate planning.

Access to Credit and Cost of Borrowing

One of the most significant financial disparities driven by SES is the cost of capital. Individuals with higher SES typically have better credit scores, more collateral, and a history of financial stability. This grants them access to lower interest rates on mortgages, business loans, and lines of credit. Conversely, those in lower-SES brackets often face “poverty premiums,” where they pay more for basic financial services and carry higher-interest debt. Recognizing this disparity is crucial for anyone looking to optimize their debt-to-income ratio and use leverage effectively as a wealth-building tool.

The Psychological Component of Money Management

SES profoundly shapes a person’s “money mindset.” Those raised in high-SES environments often view money as a tool for growth and expansion. They are taught to take calculated risks and look toward long-term horizons. In contrast, individuals from lower-SES backgrounds may develop a “scarcity mindset,” where the focus is on immediate survival and short-term liquidity. This psychological barrier can lead to risk aversion, preventing people from participating in the stock market or other volatile but high-yielding investments. Transitioning to a higher socio-economic tier often requires a conscious shift in psychological framing—from protecting what you have to strategically growing what you can.

Investment Horizons: How Status Shapes Portfolio Construction

Your socio-economic status dictates not only how much you can invest but also what you can invest in. The investment landscape is not a level playing field; it is tiered based on the resources and sophistication of the investor.

Risk Mitigation for Different Economic Brackets

For a low-to-mid-SES individual, a single market downturn can be catastrophic if they lack a robust emergency fund. Therefore, their investment strategy must prioritize liquidity and capital preservation. High-SES individuals, however, usually have multiple safety nets, allowing them to engage in “asymmetric risk”—investments where the potential upside far outweighs the downside, even if the probability of success is lower. This ability to withstand short-term losses in exchange for long-term gains is a hallmark of high-SES wealth management.

Barriers to Entry in High-Yield Markets

Certain investment vehicles are gated by socio-economic markers. For example, becoming an “accredited investor” in the United States requires a specific level of income or net worth. This status opens the door to private equity, venture capital, and hedge funds—asset classes that often outperform the public markets. Understanding SES allows an investor to see these requirements not as permanent barriers, but as milestones to be achieved through disciplined saving and strategic career growth.

The Path to Upward Mobility: Bridging the Economic Gap

While socio-economic status provides a snapshot of one’s current standing, it is not a life sentence. Upward mobility is the cornerstone of the personal finance philosophy. By identifying the levers of SES, individuals can systematically improve their financial position.

Strategic Financial Literacy

The democratization of financial information through technology has made it possible for anyone to acquire the knowledge once reserved for the elite. Strategic financial literacy involves more than just budgeting; it involves understanding tax codes, estate laws, and market mechanics. By treating financial education as a secondary occupation, individuals can bridge the gap created by their initial SES. The goal is to use information as a multiplier for every dollar earned.

Networking and Social Capital in Business

Money rarely moves in a vacuum; it moves through people. Upward socio-economic mobility is often accelerated by “proximity to power.” For entrepreneurs and professionals, this means intentionally building social capital. Attending industry conferences, joining professional organizations, and seeking mentorship from those in higher-SES brackets can provide insights and opportunities that are not available in textbooks. In the business world, your network is often a leading indicator of your future net worth.

Navigating Macroeconomic Trends through an SES Lens

Finally, it is essential to understand how broader economic shifts affect different socio-economic groups differently. A professional approach to money requires an awareness of these macro-trends.

Inflation’s Disproportionate Impact

Inflation is often called a “hidden tax” that hits lower-SES households the hardest. Because these households spend a larger percentage of their income on necessities like food and fuel, they have less flexibility to absorb price increases. Higher-SES individuals, conversely, often own inflation-hedged assets like real estate or equities, which may actually increase in value during inflationary periods. To combat this, investors must focus on acquiring “productive assets” that retain value regardless of the currency’s purchasing power.

Building Resilience Against Economic Volatility

Economic cycles are inevitable. Those with a high socio-economic status are usually better positioned to weather recessions because they have diversified income streams and liquid reserves. For those aiming to increase their SES, the priority must be building “financial resilience.” This means avoiding high-interest consumer debt, maintaining an emergency fund that covers 6-12 months of expenses, and continuously upskilling to ensure employability in a changing job market.

In conclusion, socio-economic status is more than a label; it is a complex framework of income, education, and social standing that governs our relationship with money. By understanding the mechanics of SES, we can better navigate the challenges of the financial world, exploit opportunities for growth, and ultimately build a legacy of wealth that transcends our starting point. Whether you are looking to break into a new investment tier or simply secure your family’s future, a deep understanding of socio-economic status is an indispensable tool in your financial arsenal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.