Navigating the landscape of government-sponsored healthcare requires a firm grasp of complex financial terminology. For millions of Americans, the gateway to affordable healthcare is Medicaid, a program whose eligibility is primarily determined by a specific financial metric: Modified Adjusted Gross Income, or MAGI. While the term may sound like dense tax jargon, it is the fundamental “yardstick” used to ensure that healthcare subsidies and coverage reach those who meet specific fiscal criteria under the Affordable Care Act (ACA).

Understanding MAGI is not just a matter of compliance; it is a critical component of personal financial planning. Because Medicaid eligibility hinges on this figure, knowing how to calculate it—and understanding what income sources influence it—can be the difference between securing comprehensive coverage and facing a significant gap in healthcare access.

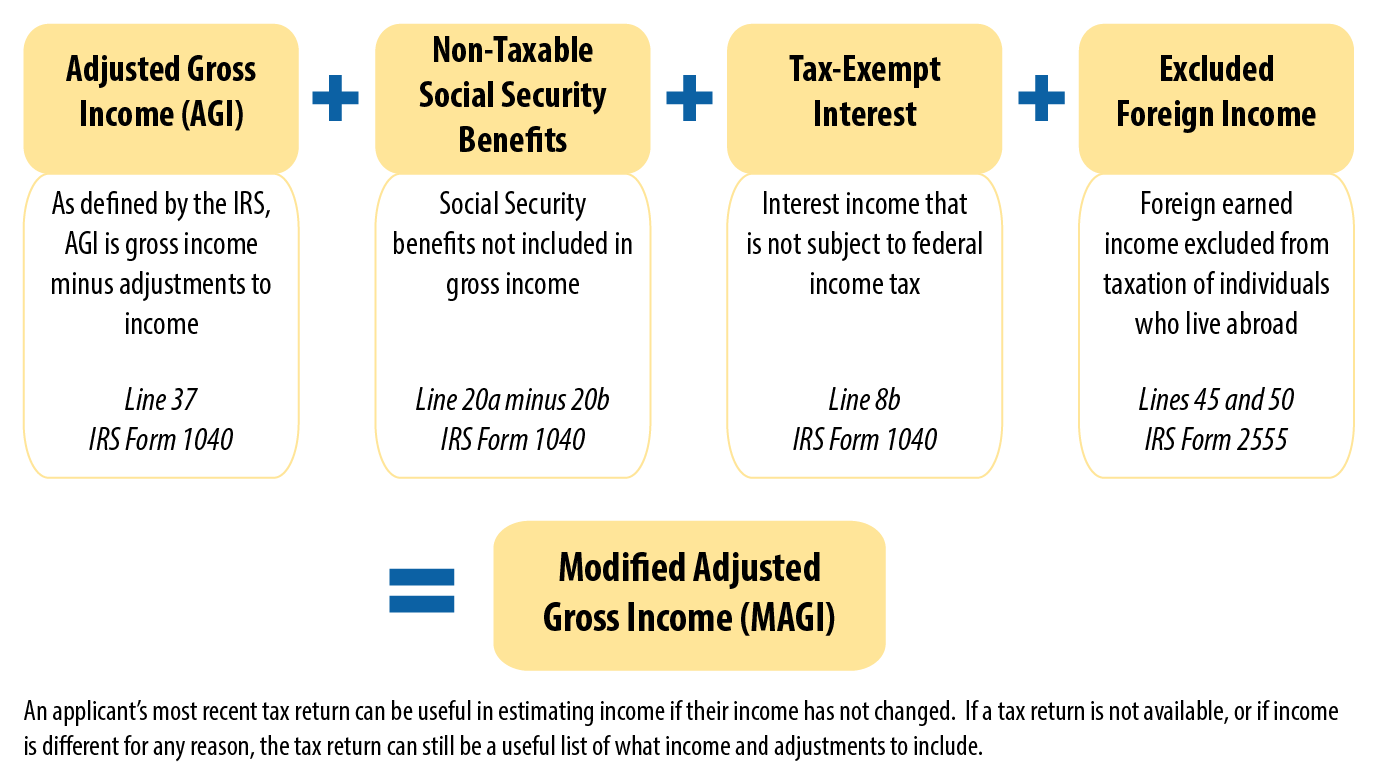

The Foundation: Defining MAGI in a Financial Context

To understand Modified Adjusted Gross Income, one must first understand its predecessor: Adjusted Gross Income (AGI). In the world of personal finance, AGI is the total income you earn in a year minus specific “above-the-line” deductions. These deductions include items such as student loan interest, alimony payments (for older divorces), and contributions to traditional IRAs.

From Gross Income to AGI

Your financial journey begins with Gross Income. This encompasses everything from your hourly wages and annual salary to dividends, capital gains, and business income. From this “top-line” number, the IRS allows you to subtract certain expenses to arrive at your AGI. This figure is found on line 11 of the IRS Form 1040. For many federal programs, AGI is the standard measure of wealth; however, for Medicaid, the government requires a more nuanced view, leading to the “Modified” portion of the equation.

The “Modified” Component

The “Modification” in MAGI refers to adding back specific types of income that are typically tax-exempt or excluded from your AGI. For the purposes of Medicaid and the ACA, MAGI is generally defined as your AGI plus three specific items:

- Untaxed Foreign Income: Any earned income from abroad that was excluded from your gross income.

- Tax-Exempt Interest: Interest earned on municipal bonds or other tax-exempt investments.

- Non-Taxable Social Security Benefits: While a portion of Social Security is often untaxed, the MAGI calculation for Medicaid pulls the full amount back into the spotlight.

By including these items, the government creates a more standardized snapshot of a household’s actual liquid resources, ensuring that individuals with significant tax-exempt assets are evaluated fairly alongside those with traditional taxable wages.

Calculating Your MAGI: A Step-by-Step Financial Breakdown

Calculating your MAGI for Medicaid requires a systematic approach to your annual finances. Because Medicaid eligibility is often processed through state exchanges or the federal marketplace, accuracy is paramount to avoid “clawbacks” or loss of coverage.

Step 1: Aggregating Taxable Income

The first step is totaling all sources of taxable income. For most individuals, this includes W-2 wages, tips, and self-employment income (net of business expenses). However, it also extends to unemployment compensation, taxable Social Security benefits, and distributions from retirement accounts. It is a common misconception that only “earned” income counts; in reality, passive income plays a significant role in your MAGI.

Step 2: Applying Statutory Deductions

Once your gross income is established, you apply the deductions allowed for AGI. For the savvy financial planner, this is where strategic moves can impact eligibility. Contributions to a Health Savings Account (HSA) or a traditional 401(k) reduce your gross income, which in turn lowers your AGI. Since MAGI is built upon AGI, these retirement and health savings vehicles serve a dual purpose: they build long-term wealth while simultaneously helping you stay within Medicaid’s income thresholds.

Step 3: Reincorporating Excluded Figures

The final step is the “add-back.” This is where you look at your tax-exempt interest and non-taxable Social Security. It is important to note that Supplemental Security Income (SSI) is not included in MAGI, as it is a needs-based program rather than an insurance-based benefit. Once these figures are added back to your AGI, you have your MAGI for the taxable year.

Household Composition and Its Impact on Eligibility

A common error in personal finance management is assuming that MAGI is an individual metric. In the context of Medicaid, MAGI is calculated at the household level. This means that the income of everyone you claim as a dependent on your tax return—and often the income of a spouse—must be factored into the total.

Defining the Medicaid Household

For tax purposes, your household consists of the filer, their spouse, and any dependents. For Medicaid purposes, the rules are largely the same but can vary based on whether you are a “tax filer” or a “non-filer.” If you are a tax filer, your MAGI household includes everyone you list on your return. If you are a non-filer (someone not required to file taxes due to low income), the household usually includes the individual, their spouse, and any children living in the home.

The Federal Poverty Level (FPL) Correlation

The reason MAGI is so vital is its relationship with the Federal Poverty Level (FPL). Medicaid eligibility is usually expressed as a percentage of the FPL. For example, in states that expanded Medicaid under the ACA, the limit is typically 138% of the FPL.

As of current fiscal standards, the dollar amount for 138% of the FPL increases with each additional household member. Therefore, a MAGI of $20,000 might disqualify a single individual but make a family of four eligible for significant benefits. Understanding this ratio is essential for families who are on the cusp of eligibility and need to manage their income or deductions to maintain coverage.

Income Inclusions and Exclusions: What Counts?

Clarity on what constitutes income is the cornerstone of financial literacy. When it comes to MAGI for Medicaid, the rules on what to include and what to ignore are strict.

Common Income Inclusions

- Wages and Salaries: Every dollar earned through traditional employment.

- Investment Income: Interest, dividends, and capital gains (even if they are reinvested).

- Business Income: Net profit from a side hustle or small business.

- Pensions and Annuities: Taxable distributions from private or employer-sponsored plans.

- Rental Income: Profit derived from real estate holdings after expenses.

Notable Exclusions

Conversely, there are several “financial inflows” that do not count toward your MAGI. These exclusions are designed to protect vulnerable populations and ensure that certain types of assistance are not penalized.

- Child Support Received: Unlike alimony (in certain cases), child support is not considered taxable income and is excluded from MAGI.

- Gifts and Inheritances: While these may have tax implications for the giver or the estate, they generally do not count as annual income for the recipient.

- Workers’ Compensation: Payments received for injury or illness sustained on the job are typically excluded.

- Veterans’ Benefits: Most VA benefits, including disability and pensions, are excluded from the MAGI calculation.

Knowing these exclusions allows individuals to accurately report their finances without artificially inflating their income, which could lead to an unnecessary denial of benefits.

Strategic Financial Planning and Medicaid

For those in the “middle ground”—individuals whose income fluctuates near the eligibility line—managing MAGI becomes a tactical financial exercise.

Managing Fluctuating Income

Freelancers, seasonal workers, and small business owners often face “lumpy” income. Since Medicaid eligibility is often checked monthly or annually depending on the state, a single high-earning month could theoretically jeopardize coverage. Strategic planners often use deductible expenses—such as equipment purchases for a business or allowable retirement contributions—to smooth out their MAGI over the fiscal year.

The Impact of Life Changes

Marriage, divorce, the birth of a child, or a dependent moving out of the house all trigger a recalculation of household MAGI. In the world of business finance and personal accounting, these are “qualifying life events.” From a financial perspective, a change in household size effectively changes the denominator of the FPL equation. A professional financial advisor will often suggest reviewing MAGI immediately following any major life change to ensure that healthcare costs remain predictable and manageable.

Long-Term Wealth vs. Short-Term Eligibility

One of the most profound aspects of the MAGI-based system is that it focuses on income rather than assets. In many Medicaid categories (specifically those under the ACA expansion), there is no “asset test.” This means a person could theoretically have significant savings in a bank account or equity in a primary residence and still qualify for Medicaid if their MAGI (annual income flow) is below the threshold. This allows individuals to preserve their wealth and retirement savings while still accessing necessary healthcare during periods of low income.

In conclusion, Modified Adjusted Gross Income is the financial pulse of the Medicaid system. By understanding how AGI is modified, how household size scales the requirements, and which income sources are excluded, individuals can navigate the healthcare system with professional precision. MAGI is more than a number on a tax form; it is a vital tool for ensuring financial stability and health security in an increasingly complex economic environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.