Navigating the landscape of higher education is as much a financial challenge as it is an academic one. For many prospective students and their families, the “sticker price” of a college degree can be overwhelming, often leading to a lifetime of debt. However, one of the most significant levers in personal finance for students is the distinction between in-state and out-of-state tuition. Understanding what in-state tuition is, how it works, and how to qualify for it is a critical component of a sound financial strategy for anyone looking to optimize their educational investment.

Understanding the Financial Fundamentals of In-State Tuition

At its core, in-state tuition is a discounted rate of tuition offered by public colleges and universities to students who are legal residents of the state where the institution is located. This financial structure is not a random discount; it is a direct reflection of the social contract between a state government and its citizens.

Defining In-State vs. Out-of-State Costs

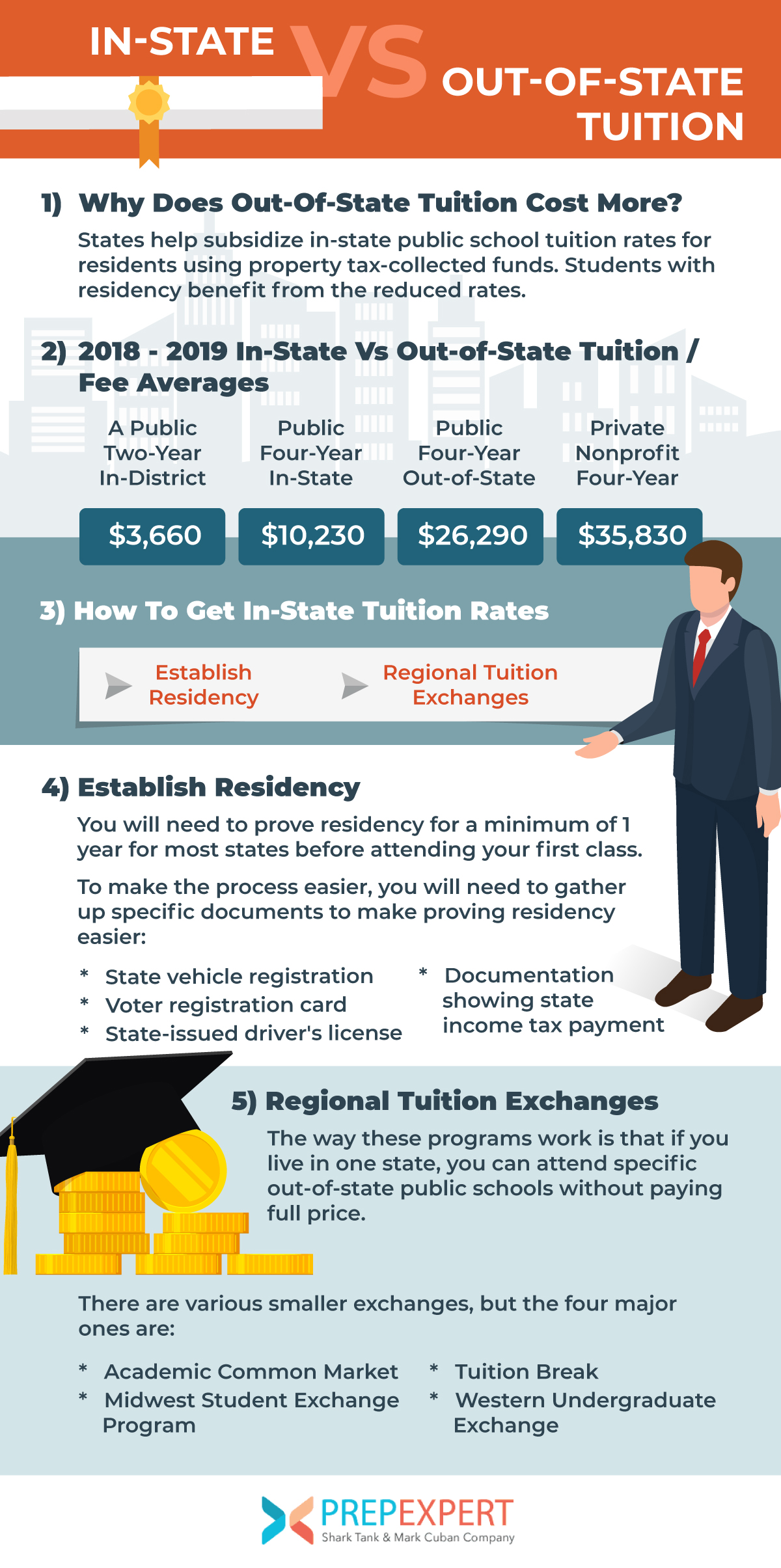

The price discrepancy between in-state and out-of-state tuition is often staggering. On average, out-of-state students pay two to three times more for the same credits, the same professors, and the same degree as their in-state peers. From a personal finance perspective, this is a massive price premium. In-state tuition represents a subsidized rate, whereas out-of-state tuition reflects something closer to the actual market cost of the education, often with an added premium to help bolster the university’s budget.

When you look at the balance sheet of a public university, the in-state rate is designed to make higher education accessible to the local workforce. For a student, choosing an in-state institution is often the single most effective way to reduce the “cost of goods sold” regarding their degree, effectively increasing their future net worth by minimizing initial liabilities.

Why the Price Gap Exists: The Role of Taxpayer Funding

To understand the “why” behind in-state tuition, one must look at state tax structures. Public universities receive a portion of their funding from state tax revenues. Because residents of that state pay income, sales, and property taxes, they are essentially pre-paying for the public university system.

From a financial planning standpoint, in-state tuition is a return on investment for the taxes a family has paid over the years. Out-of-state students, who have not contributed to that specific state’s tax pool, are charged a higher rate to compensate for the lack of state-level subsidy. This makes in-state tuition a unique financial benefit reserved for those who have a documented financial and legal history within a specific jurisdiction.

Establishing Residency: The Path to Financial Eligibility

Qualifying for in-state tuition is not as simple as having a mailing address in a specific state. Because the financial stakes are so high, universities have rigorous standards to ensure that students are true residents rather than “educational tourists” who have moved solely for the discount.

Domicile and the 12-Month Rule

Most states require a student to demonstrate “domicile”—a legal term meaning the place you intend to make your permanent home—for at least 12 consecutive months prior to enrollment. This is a crucial timeline for financial planning. If a family is considering a move to a different state to take advantage of lower tuition rates, they must account for this one-year waiting period.

During this time, the student or their guardians must prove that their move was for reasons other than just obtaining a cheaper education. This might include full-time employment within the state or other long-term commitments. Failing to meet this 12-month threshold can result in a “non-resident” classification, which can cost a student tens of thousands of dollars in the first year alone.

Documentation Needed to Prove Residency

Proving residency is an exercise in meticulous record-keeping. To secure the in-state rate, institutions typically require a “preponderance of evidence.” This includes, but is not limited to:

- State Income Tax Returns: Showing that you have filed taxes as a resident.

- Driver’s License and Vehicle Registration: Swapping these over to the new state as soon as possible is a key indicator of intent.

- Voter Registration: Demonstrating civic engagement in the local community.

- Lease Agreements or Mortgages: Physical proof of a permanent residence.

From a money management perspective, the effort required to gather this documentation is well worth the “hourly rate” of the savings achieved. If an in-state discount saves $20,000 per year, the few hours spent organizing paperwork become some of the most profitable hours a student or parent will ever spend.

Common Pitfalls in Residency Reclassification

One of the biggest financial mistakes students make is assuming they can easily switch from out-of-state to in-state status after their freshman year. Most universities make this incredibly difficult. If you enter as an out-of-state student, the burden of proof to show that your “intent” has changed is very high. Simply living in a dorm does not count toward residency. Understanding these nuances is vital to avoid a four-year financial commitment that is significantly higher than originally budgeted.

Strategic Alternatives: Tuition Reciprocity and Financial Waivers

While qualifying for in-state tuition usually depends on residency, there are sophisticated financial “loopholes” and programs designed to help students bypass the high cost of out-of-state tuition. These are essential tools for any student’s financial toolkit.

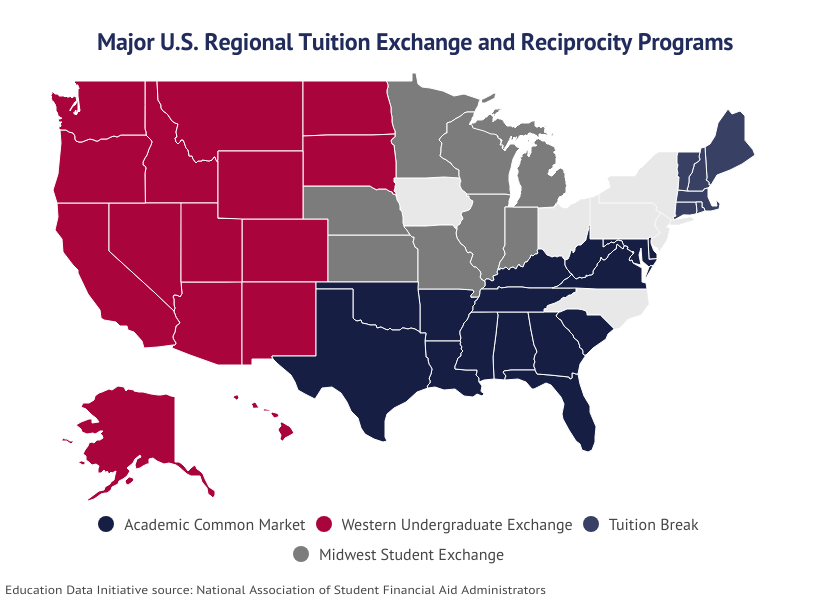

Regional Tuition Exchange Programs

Many states have realized that it is mutually beneficial to share educational resources. This has led to the creation of regional reciprocity agreements. For example:

- Western Undergraduate Exchange (WUE): Students in participating western states can attend out-of-state public universities for no more than 150% of the in-state rate.

- Midwest Student Exchange Program (MSEP): A similar program for the Midwest region.

- Southern Regional Education Board (SREB) Academic Common Market: This allows students to pay in-state rates for specific majors not offered in their home state.

By utilizing these programs, a student can find a middle ground—paying more than in-state, but significantly less than the standard out-of-state rate. This “discounting” strategy allows for greater geographic flexibility without the full financial burden of non-resident fees.

Military and Legacy Exemptions

Financial planning for education should also account for specific status-based waivers. Many states offer in-state tuition to active-duty military members, veterans, and their dependents regardless of how long they have lived in the state. Furthermore, some universities offer “legacy” waivers where children of alumni can qualify for in-state or reduced rates. Identifying these opportunities early in the college search process can save a family a fortune, effectively acting as a guaranteed scholarship.

The Long-Term Financial Impact of Choosing In-State Education

When we analyze the choice of in-state tuition through the lens of personal finance, the focus shifts from the immediate cost to the long-term wealth-building potential. The “opportunity cost” of a more expensive out-of-state degree can be measured in decades of lost investment potential.

Reducing the Student Debt Burden

The primary advantage of in-state tuition is the drastic reduction in the need for student loans. If a student saves $15,000 a year by staying in-state, that is $60,000 less in principal debt over four years. However, the real saving is much higher when you factor in interest. At a 6% interest rate over a 10-year repayment term, that $60,000 in savings actually prevents nearly $80,000 in total payments.

Lower debt levels upon graduation mean a higher “disposable income” in one’s 20s. This allows for earlier entry into the housing market, the ability to start a business, or the freedom to take a lower-paying but more fulfilling “dream job” that might have been impossible with a $1,000-a-month loan payment.

Return on Investment (ROI) and Career Trajectory

In the world of business finance, ROI is king. When applying this to education, the “return” is the salary earned after graduation, and the “investment” is the tuition paid. Many in-state public universities are top-tier research institutions that rival private or out-of-state schools in terms of prestige and networking.

If a student can achieve a $70,000 starting salary with a degree that cost $40,000 (in-state) versus the same salary with a degree that cost $120,000 (out-of-state), the in-state path is the vastly superior financial decision. The “brand” of the school rarely makes up for a 3x difference in cost unless the student is entering a very niche field like high-end management consulting or investment banking.

Planning Your Financial Future with In-State Savings

Choosing the in-state route is not just about spending less; it is about what you do with the money you don’t spend. A proactive financial strategy involves redirecting those potential tuition dollars into assets that grow.

Integrating Tuition Savings into a 529 Plan Strategy

For parents, if a child qualifies for in-state tuition, the funds remaining in a 529 College Savings Plan can be a powerful financial tool. Recent changes in tax law (such as the SECURE 2.0 Act) allow for a portion of unused 529 funds to be rolled over into a Roth IRA for the beneficiary. This means that by choosing a lower-cost in-state education, a parent can jumpstart their child’s retirement savings, giving them a massive head start in the world of compound interest.

Using Saved Capital for Early Career Investing

For the student who works during college or has personal savings, the lower cost of in-state tuition means more “capital” available to invest in the market during their formative years. Investing even small amounts in an index fund while still in school—made possible by lower tuition bills—can lead to significant wealth over 40 years.

In conclusion, in-state tuition is more than just a lower price tag; it is a strategic financial advantage. By understanding residency requirements, leveraging reciprocity agreements, and focusing on the long-term ROI, students and families can secure a high-quality education without compromising their future financial security. In the world of personal finance, the decision to go “in-state” is often the most impactful investment move a young adult can make.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.