Navigating the landscape of business finance requires a keen understanding of various tax obligations that go beyond simple income tax. For any entrepreneur or financial manager in the United States, the Federal Unemployment Tax Act (FUTA) represents a critical component of payroll management. While often overshadowed by Social Security and Medicare taxes, the FUTA tax rate is a fundamental pillar of the American social safety net, providing the necessary funding for state unemployment insurance agencies. Understanding how this rate is calculated, who is responsible for it, and how to minimize the financial burden through tax credits is essential for maintaining a healthy bottom line and ensuring regulatory compliance.

What is FUTA and How Does the Tax Rate Work?

At its core, the Federal Unemployment Tax Act (FUTA) is a federal law that imposes a payroll tax on employers. Unlike many other payroll taxes where the cost is shared between the employer and the employee, FUTA is strictly an employer-paid tax. The funds collected through this tax are used to oversee and administer unemployment insurance programs and job service programs across all states.

The Legal Framework of the Federal Unemployment Tax Act

FUTA was established to ensure that workers who lose their jobs through no fault of their own have access to temporary financial assistance. The federal government uses these funds to provide grants to state governments, which then manage the actual distribution of unemployment benefits. From a business finance perspective, FUTA is a mandatory operating expense that must be accounted for in every hiring decision. It is governed by the Internal Revenue Service (IRS), and failure to adhere to its regulations can lead to significant financial penalties and legal complications for a business.

Who is Responsible for Paying FUTA?

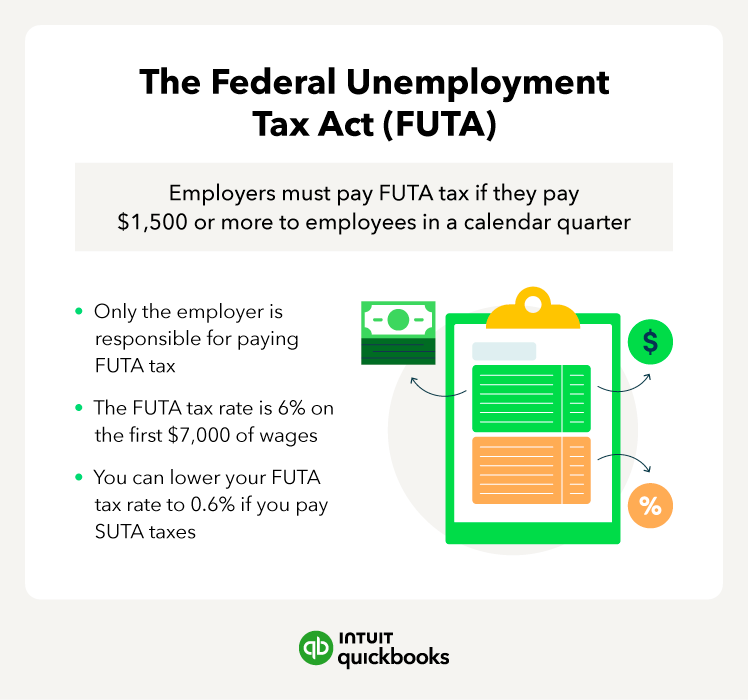

Determining whether your business is liable for FUTA is the first step in financial planning. Generally, you are required to pay FUTA tax if you meet one of two primary criteria set by the IRS. First, the “General Test” applies if you paid wages of $1,500 or more to employees in any calendar quarter during the current or preceding year. Second, if you had one or more employees for at least some part of a day in any 20 or more different weeks during the year, you are liable. It is important to note that “employees” include full-time, part-time, and temporary workers, but generally exclude independent contractors.

The Current FUTA Tax Rate and Wage Base

As of the current tax year, the nominal FUTA tax rate is 6.0%. However, this percentage is not applied to an employee’s entire annual salary. Instead, it is only applied to the first $7,000 paid to each employee as wages during the year. This $7,000 threshold is known as the “federal wage base.” Once an employee’s cumulative earnings for the year exceed $7,000, the employer stops paying FUTA tax on that specific individual. This means the maximum federal tax per employee, before any credits, is $420 ($7,000 x 0.06). For businesses with high turnover or many seasonal employees, these costs can accumulate quickly, making it a vital figure in annual budgeting.

Navigating the FUTA Tax Credit and Effective Rates

While the statutory rate of 6.0% might seem high, the reality for most businesses is much more manageable. The federal government provides a mechanism to prevent “double taxation,” as employers also have to pay State Unemployment Tax (SUTA). This mechanism comes in the form of a substantial tax credit.

The 5.4% Tax Credit Explained

To incentivize businesses to pay their state unemployment taxes on time, the IRS allows a maximum credit of 5.4% against the 6.0% FUTA tax rate. To qualify for the full 5.4% credit, a business must pay its state unemployment taxes in full and on time. If the business resides in a state that is not in “credit reduction” status (which we will discuss shortly), the credit effectively reduces the federal tax burden significantly. This credit is designed to ensure that the bulk of unemployment funding stays at the state level where benefits are actually administered.

Calculating Your Effective FUTA Tax Liability

When the 5.4% credit is applied to the 6.0% statutory rate, the “effective” FUTA tax rate becomes 0.6%. This is the figure most business owners use when forecasting their payroll expenses. When calculated against the $7,000 wage base, the maximum effective FUTA tax per employee is $42 ($7,000 x 0.006). This reduction from $420 to $42 per employee highlights the importance of staying compliant with state-level unemployment tax requirements. If a business fails to pay its SUTA on time, it may lose part or all of this credit, which could increase its federal tax liability by up to tenfold.

Understanding FUTA Credit Reductions

A nuance that often catches financial planners off guard is the “Credit Reduction.” If a state’s unemployment fund lacks the reserves to pay out benefits, it may borrow money from the federal government. If the state fails to repay these loans within a specified timeframe (usually two years), the federal government recoups the money by reducing the 5.4% FUTA tax credit for employers in that state. A credit reduction effectively raises the FUTA tax rate for businesses in that specific jurisdiction. For example, if a state has a 0.3% credit reduction, the effective FUTA rate for employers in that state would be 0.9% (0.6% standard + 0.3% reduction) instead of 0.6%. Monitoring state financial health is, therefore, a subtle but necessary part of corporate financial strategy.

Compliance, Filing, and Financial Deadlines

Effective money management requires not just knowing what you owe, but knowing when and how to pay it. The IRS has strict guidelines for reporting and depositing FUTA taxes, and staying on top of these deadlines is crucial for avoiding interest charges and penalties.

Master Form 940: The Annual Federal Unemployment Tax Return

Employers report their annual FUTA tax liability using IRS Form 940. This form summarizes the total wages paid, the amount of wages exempt from FUTA, the total tax due, and the adjustments for state unemployment tax credits. Form 940 is generally due by January 31st for the preceding calendar year. However, if you have deposited all your FUTA tax when due, you may have until February 10th to file the return. Accurate completion of Form 940 is vital, as it reconciles your federal payments with your state credits, ensuring you aren’t overpaying or underpaying.

Quarterly vs. Annual Deposit Requirements

While Form 940 is filed annually, the tax itself is often due more frequently. The frequency of your deposits depends on the amount of your FUTA tax liability. If your FUTA tax liability is $500 or less in a cumulative quarter, you are not required to make a deposit; instead, you can carry it over to the next quarter. Once your cumulative liability exceeds $500, you must deposit the tax by the last day of the month following the end of that quarter. If your total liability for the year is under $500, you can simply pay the tax along with your Form 940 filing in January. Digital payments are now the standard, typically handled through the Electronic Federal Tax Payment System (EFTPS).

Common Pitfalls and How to Avoid Penalties

One of the most common mistakes in business finance regarding FUTA is miscalculating the wage base for employees who leave and are replaced. Since the tax applies to the first $7,000 of each employee’s wages, hiring three people for the same position sequentially throughout the year (due to turnover) results in a higher tax burden than keeping one person in that position. Additionally, forgetting to account for credit reductions in specific states can lead to underpayment. To avoid penalties, businesses should utilize automated payroll software or work with a dedicated tax professional who can track these fluctuating state-level variables.

Strategic Financial Planning for Unemployment Taxes

Beyond mere compliance, understanding the FUTA rate is about strategic financial management. Every dollar spent on taxes is a dollar not invested in growth, so optimizing how you handle these liabilities is a hallmark of sophisticated business finance.

Budgeting for Payroll Taxes in Your Business Model

When calculating the “true cost” of a new hire, a savvy business owner looks beyond the gross salary. You must factor in the “employer burden,” which includes FICA (Social Security and Medicare), SUTA, and FUTA. Because the FUTA tax is front-loaded—meaning it is usually paid off early in the year as employees reach the $7,000 threshold—businesses often experience higher payroll costs in Q1 and Q2. Recognizing this seasonal dip in cash flow allows for better liquidity management and ensures that the business remains stable even during months of higher tax outflows.

The Interplay Between FUTA and SUTA

FUTA and SUTA are inextricably linked. In many ways, the federal tax acts as an enforcement mechanism for state taxes. Because the federal credit is dependent on state compliance, businesses must prioritize their SUTA obligations to keep their FUTA rate at the 0.6% minimum. Furthermore, some states have much higher wage bases than the federal $7,000 (some exceeding $40,000). A comprehensive financial strategy involves looking at the combined impact of both taxes to determine the most tax-efficient locations for expanding operations or hiring remote staff.

Long-term Impact on Cash Flow Management

In the grand scheme of a multi-million dollar corporation, $42 per employee might seem negligible. However, for small to mid-sized enterprises (SMEs) with dozens or hundreds of employees, these figures add up. Moreover, the administrative cost of compliance—tracking credits, managing Form 940, and ensuring timely deposits—represents a significant investment of time or professional fees. By automating these processes and integrating FUTA projections into the annual budget, businesses can transform a complex regulatory requirement into a predictable, manageable line item. Ultimately, mastering the FUTA rate is about more than just paying a tax; it’s about demonstrating the financial discipline required to build a sustainable and legally sound enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.