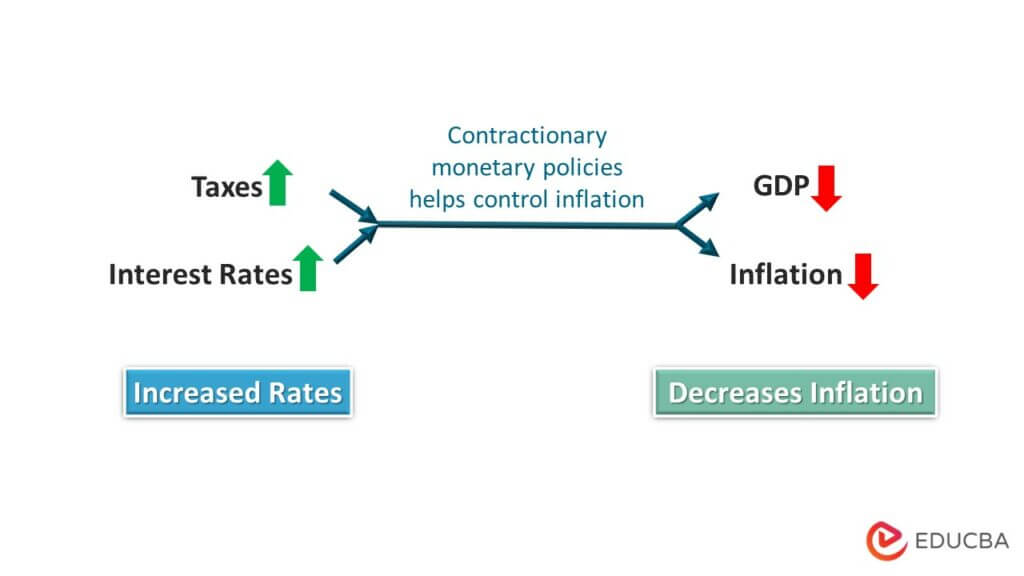

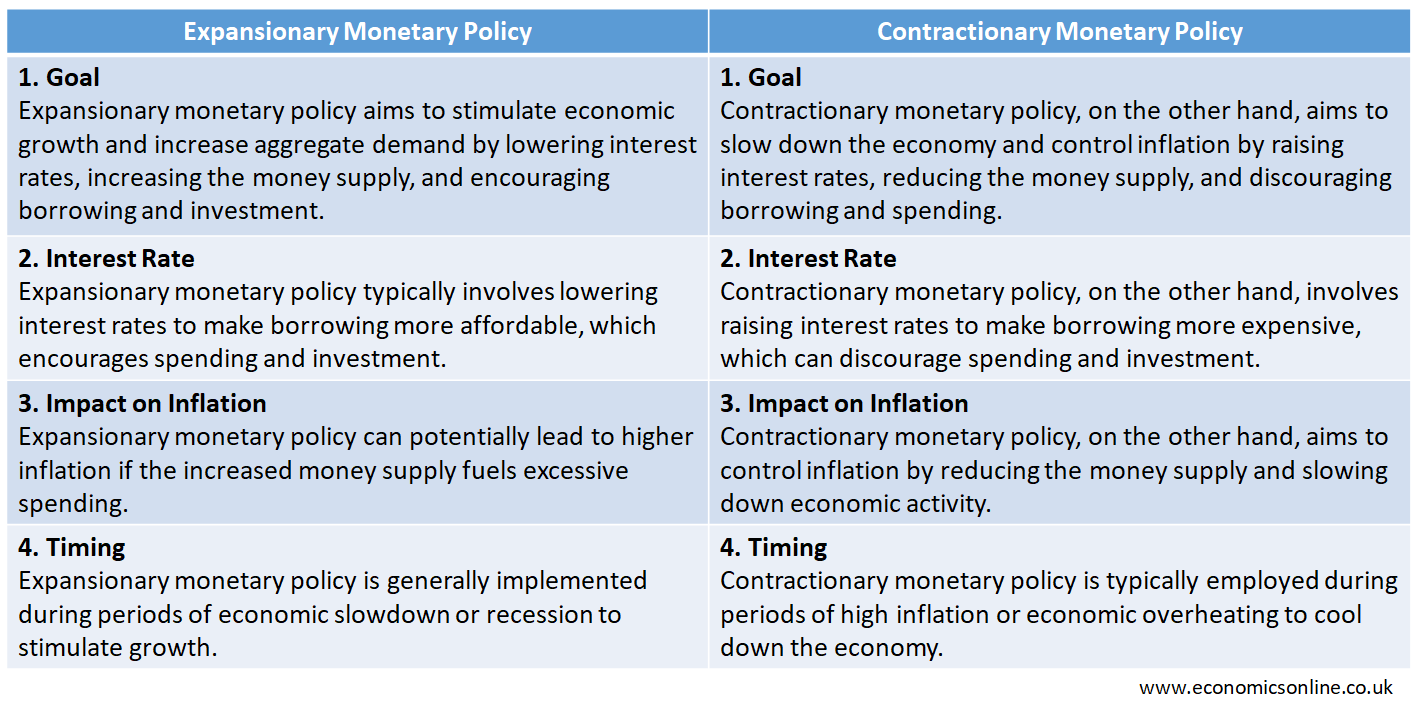

Contractionary monetary policy is a fundamental tool used by central banks to manage a nation’s economy. Often referred to as “tightening,” this policy involves reducing the money supply and increasing interest rates to combat rising inflation and prevent the economy from overheating. While it might sound counterintuitive for a government to want to “slow down” growth, this strategy is essential for maintaining long-term price stability and ensuring that the purchasing power of a currency remains intact.

In the world of finance and investing, understanding contractionary policy is vital. It dictates the cost of borrowing, the performance of the stock market, and the yield on savings accounts. This article explores the mechanics of contractionary monetary policy, the reasons central banks implement it, and the profound impact it has on both personal and business finance.

The Primary Mechanisms of Contractionary Monetary Policy

Central banks, such as the Federal Reserve in the United States, use three primary levers to execute contractionary policy. Each of these methods works by making money “tighter” or more expensive to obtain, thereby reducing the overall level of spending in the economy.

Increasing Interest Rates

The most visible tool of contractionary policy is the adjustment of the benchmark interest rate—often called the federal funds rate in the U.S. When the central bank raises this rate, it becomes more expensive for commercial banks to borrow money from each other. Consequently, these banks pass the higher costs on to consumers and businesses. This leads to higher interest rates on mortgages, auto loans, credit cards, and business lines of credit. By increasing the cost of borrowing, the central bank incentivizes saving over spending, which naturally slows down economic activity.

Open Market Operations (Selling Securities)

Central banks also manage the money supply through Open Market Operations (OMO). In a contractionary phase, the central bank sells government securities (bonds) to institutional investors and banks. When these entities buy the bonds, they pay the central bank with cash, which is then effectively removed from circulation. This reduction in the “monetary base” limits the amount of capital available for banks to lend, further tightening the financial environment.

Raising Reserve Requirements

Though used less frequently than interest rate adjustments, central banks can also change the reserve requirements for commercial banks. The reserve requirement is the percentage of total deposits that a bank must keep in its vaults or at the central bank rather than lending out. By raising this requirement, the central bank forces commercial banks to hold onto more cash, which reduces the amount of money available for consumer and business loans.

Why Central Banks Implement Contractionary Strategies

At first glance, slowing down an economy seems like an odd objective for policymakers. However, unbridled growth can lead to systemic instabilities that are far more damaging than a temporary slowdown.

Taming Inflation and Preserving Purchasing Power

The primary driver for contractionary policy is inflation. When the demand for goods and services outstrips supply, prices rise. While a small amount of inflation (usually around 2%) is considered healthy, “runaway” or “hyper-inflation” can erode the value of savings and make it impossible for businesses to plan for the future. By reducing the money supply and making borrowing more expensive, the central bank reduces aggregate demand, which helps stabilize prices and protects the consumer’s purchasing power.

Cooling an Overheated Economy

An economy is “overheated” when it is expanding at an unsustainable rate. This often manifests as excessively low unemployment rates that lead to wage-price spirals—where companies raise wages to attract workers, then raise prices to cover the higher labor costs. Contractionary policy acts as the “brakes” for the economy, ensuring that growth remains at a steady, sustainable pace rather than peaking and leading to a catastrophic crash.

Preventing Asset Bubbles

Excessively low interest rates can lead to “easy money,” which often flows into speculative assets rather than productive investments. This can create bubbles in the real estate market, the stock market, or even the cryptocurrency space. By tightening the money supply, the central bank makes it more expensive to leverage investments, which helps deflate these bubbles before they burst and threaten the stability of the entire financial system.

The Impact on Personal and Business Finance

Contractionary monetary policy is not just a theoretical concept discussed in boardrooms; it has a direct and immediate impact on the wallets of everyday citizens and the balance sheets of corporations.

The Rising Cost of Consumer Debt

For the individual, the most immediate effect of contractionary policy is felt in the cost of credit. As the central bank raises rates, the Annual Percentage Rate (APR) on credit cards typically rises in lockstep. Mortgages also become more expensive, which can cool the housing market as fewer people can afford the monthly payments on a new home. For those with variable-rate loans, contractionary policy can significantly increase monthly expenses, forcing households to tighten their own budgets.

Business Expansion and Capital Expenditure

For businesses, contractionary policy changes the math on investment. When the cost of capital increases, projects that seemed profitable at a 3% interest rate may no longer be viable at 7%. As a result, companies often delay the construction of new factories, pause the acquisition of new equipment, and slow down their hiring processes. This reduction in corporate spending is a key goal of the policy, as it helps lower the overall demand for labor and materials.

The Silver Lining: Higher Returns for Savers

While borrowers suffer under contractionary policy, savers often benefit. During periods of low interest rates (expansionary policy), traditional savings accounts and Certificates of Deposit (CDs) often offer negligible returns. However, as the central bank tightens, commercial banks eventually raise the interest rates they offer to depositors to attract more capital. This makes “risk-free” investments more attractive, providing a reliable income stream for retirees and conservative investors.

How Tightening Affects Financial Markets and Investing

Investors must pay close attention to the central bank’s “hawkish” signals—terms used to describe a preference for contractionary policy. The transition from a loose to a tight monetary environment can create significant volatility across all asset classes.

Stock Market Valuations and the Discount Rate

The stock market generally reacts negatively to contractionary policy, at least in the short term. There are two main reasons for this. First, higher interest rates increase the “discount rate” used by analysts to value future earnings. When the discount rate is higher, the present value of those future earnings is lower, leading to lower stock prices—particularly for high-growth tech companies. Second, because borrowing is more expensive, corporate profit margins can shrink, making stocks less attractive relative to other assets.

Bond Yields and Fixed Income

In the bond market, there is an inverse relationship between interest rates and bond prices. When the central bank raises rates, newly issued bonds offer higher coupons (interest payments). Consequently, older bonds with lower interest rates become less valuable, and their market price drops. However, for new investors, contractionary policy offers an opportunity to lock in higher yields on government and corporate debt, providing a safer alternative to the volatile equity markets.

Currency Strength and Global Trade

Contractionary policy often leads to a stronger domestic currency. When a central bank raises interest rates, it attracts foreign capital from investors seeking higher returns on that currency’s debt. As demand for the currency increases, its value rises against other global currencies. While a strong currency makes foreign goods cheaper for domestic consumers, it makes domestic exports more expensive for the rest of the world, which can impact the profitability of multi-national corporations.

Balancing the Scales: The Risks of Over-Tightening

The challenge for any central bank is timing. If they tighten too slowly, inflation can become “entrenched,” requiring even more drastic measures later. If they tighten too quickly or too aggressively, they risk pushing the economy into a recession.

The Threat of Recession and “Hard Landings”

The goal of contractionary policy is often described as a “soft landing”—slowing inflation without causing a significant spike in unemployment or a contraction in the Gross Domestic Product (GDP). However, the history of monetary policy shows that soft landings are difficult to achieve. If the central bank makes credit too expensive too quickly, consumer spending can collapse, leading to business failures and mass layoffs. This transition from a controlled slowdown to a full-blown recession is a constant concern for economists.

The Unemployment Lag

Monetary policy is often described as having “long and variable lags.” It can take six to eighteen months for an interest rate hike to fully work its way through the economy and affect consumer behavior. This creates a danger that the central bank might keep raising rates because they don’t see immediate results, only to realize later that they have “over-tightened,” causing more economic pain than was necessary to stop inflation.

Conclusion

Contractionary monetary policy is a vital, albeit painful, necessity in the cycle of modern economics. By raising interest rates, selling government securities, and increasing reserve requirements, central banks can effectively rein in inflation and prevent the formation of dangerous asset bubbles.

For the individual investor or business owner, contractionary policy serves as a signal to shift strategies. It is a time to prioritize debt reduction, focus on cash flow, and perhaps take advantage of higher yields in fixed-income markets. While the transition away from “easy money” can be turbulent for the stock market and the housing sector, the ultimate goal of contractionary policy is to ensure a stable financial foundation that allows for sustainable prosperity in the years to come. Understanding these mechanics allows market participants to navigate periods of tightening with greater confidence and strategic foresight.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.