Navigating the complexities of the U.S. tax code can often feel like a daunting task for even the most seasoned investors. However, buried within the thousands of pages of legislative text are specific provisions designed to encourage investment and provide significant tax relief. One such provision, which rose to prominence following the Tax Cuts and Jobs Act (TCJA) of 2017, is the Section 199A dividend.

For individual investors, particularly those with exposure to Real Estate Investment Trusts (REITs) or specialized mutual funds, understanding Section 199A is not just a matter of compliance—it is a critical component of maximizing after-tax returns. This guide explores the mechanics of Section 199A dividends, how they function within the broader Qualified Business Income (QBI) framework, and how you can leverage them to optimize your financial portfolio.

The Fundamentals of Section 199A and the QBI Deduction

To understand what a Section 199A dividend is, one must first understand the broader legislative context from which it emerged. Section 199A was introduced as a cornerstone of the 2017 tax reform, aimed primarily at providing a tax break to owners of “pass-through” businesses.

The Origin: The Tax Cuts and Jobs Act of 2017

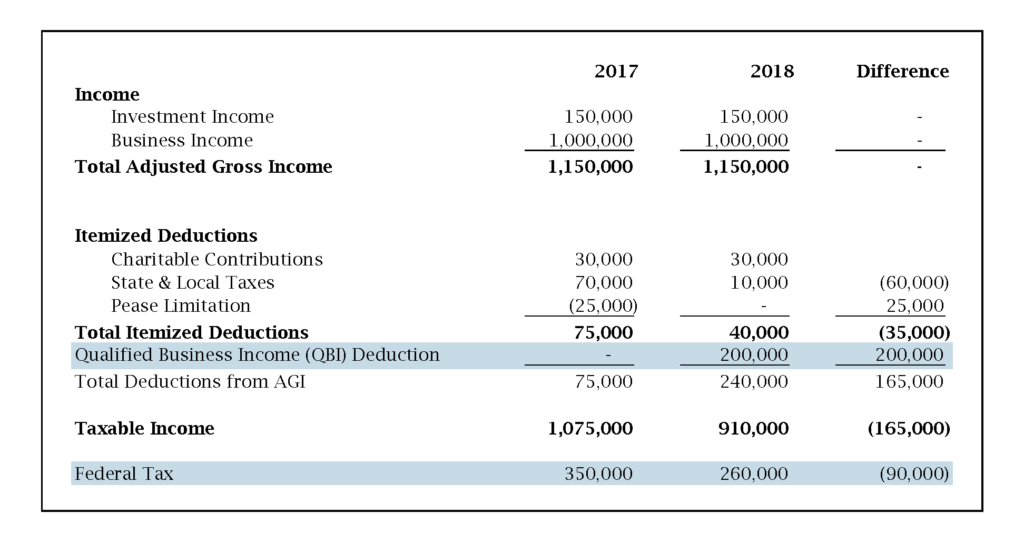

Prior to 2017, C-corporations were taxed at a significantly higher rate than they are today. When the TCJA slashed the corporate tax rate to a flat 21%, lawmakers realized that small businesses and pass-through entities (such as S-corporations, partnerships, and sole proprietorships) would be at a competitive disadvantage. To level the playing field, Section 199A was created, allowing eligible taxpayers to deduct up to 20% of their “Qualified Business Income” (QBI) from their taxable income.

Defining the Section 199A Dividend

While much of the discussion surrounding Section 199A focuses on small business owners, the provision also includes a specific category for investors: the “Qualified REIT Dividend.” In the context of your tax forms and brokerage statements, this is commonly referred to as a Section 199A dividend.

Unlike standard dividends paid by traditional C-corporations, which are typically taxed at either preferential capital gains rates (qualified dividends) or ordinary income rates (non-qualified dividends), Section 199A dividends represent income passed through from entities that do not pay corporate-level income tax. By designating these as 199A dividends, the IRS allows individual taxpayers to claim a 20% deduction on this specific portion of their investment income, effectively lowering the tax burden.

How REITs and Mutual Funds Generate 199A Dividends

The presence of a Section 199A dividend on your tax return is usually the result of your involvement in the real estate market or specific types of pooled investment vehicles.

The Role of Real Estate Investment Trusts (REITs)

REITs are the primary engine behind Section 199A dividends. A REIT is a company that owns, operates, or finances income-producing real estate. To maintain their status as a REIT and avoid paying corporate income tax, these entities are required by law to distribute at least 90% of their taxable income to shareholders in the form of dividends.

Because the REIT itself does not pay federal income tax on the profits it distributes, the IRS historically taxed these dividends at the recipient’s ordinary income tax rate. Section 199A changes this dynamic. By classifying these distributions as “qualified REIT dividends,” the tax code allows investors to exclude 20% of that income from their taxable total, acknowledging the pass-through nature of the REIT structure.

Pass-through Treatment in Mutual Funds and ETFs

Many investors do not own individual REIT stocks but still see Section 199A dividends on their 1099-DIV forms. This occurs because mutual funds and Exchange-Traded Funds (ETFs) act as conduits. If a mutual fund holds shares in a REIT and receives qualified REIT dividends, it can pass the tax character of those dividends through to its own shareholders.

This “conduit treatment” ensures that small investors who use diversified funds are not penalized compared to wealthy investors who might hold direct real estate interests. When the fund sends out its year-end tax summaries, it will break out the portion of the total distribution that qualifies for the Section 199A deduction, allowing the investor to apply the 20% reduction to that specific amount.

Calculating the Tax Advantages: The 20% Deduction

The primary appeal of the Section 199A dividend is its ability to significantly lower the effective tax rate on investment income. However, the math behind the deduction is specific and requires a clear understanding of your overall tax picture.

How the Deduction Reduces Your Effective Tax Rate

The Section 199A deduction is a “below-the-line” deduction, meaning it reduces your taxable income but does not reduce your Adjusted Gross Income (AGI).

For example, if an investor in the 37% tax bracket receives $10,000 in Section 199A dividends, they are entitled to a deduction of 20%, which is $2,000. Instead of paying 37% tax on the full $10,000 ($3,700), they only pay 37% tax on $8,000 ($2,960). This reduces the effective tax rate on that dividend income from 37% to 29.6%. For many investors, this makes REITs and other 199A-eligible investments far more attractive than they were under previous tax regimes.

Limitations and Phase-outs for High Earners

While the 20% deduction on REIT dividends is generally more straightforward than the deduction for business owners, it is still subject to certain overall limitations. The total QBI deduction (which includes Section 199A dividends) cannot exceed 20% of the taxpayer’s taxable income minus any net capital gains.

Furthermore, while the “wage and property” limitations that restrict business owners often do not apply to the REIT dividend portion of Section 199A, it is essential to monitor your total taxable income. If your income exceeds certain thresholds, the calculation can become more complex, particularly if you are also claiming QBI from a self-owned business or partnership.

Navigating Tax Forms: Identifying 199A Dividends on Your 1099-DIV

For most investors, the first time they encounter the term “Section 199A” is during tax season when they receive their annual reporting documents from their brokerage.

Box 5: The Magic Number for Investors

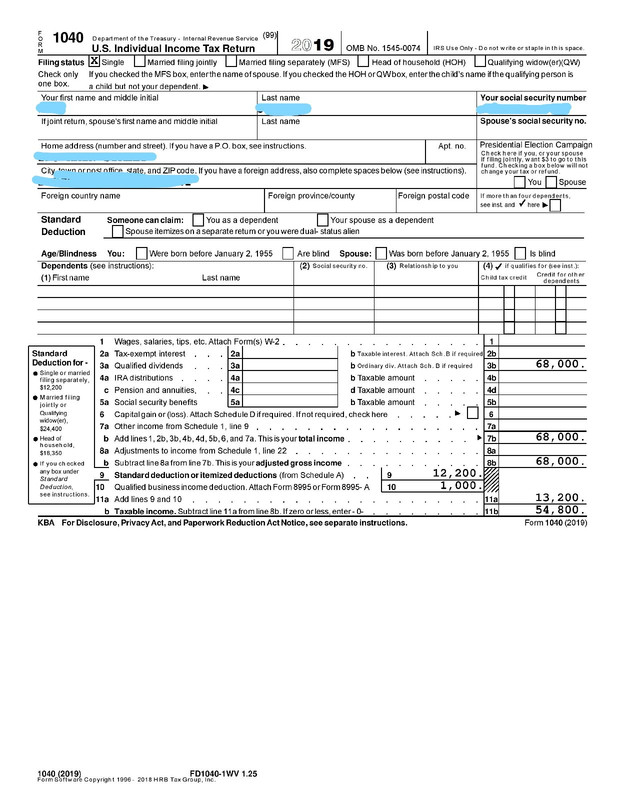

When you receive Form 1099-DIV, you will see various boxes representing different types of distributions. Box 1a shows total ordinary dividends, and Box 1b shows qualified dividends. However, to find your Section 199A information, you must look at Box 5, labeled “Section 199A dividends.”

The amount listed in Box 5 is already included in the total ordinary dividends shown in Box 1a. You do not add Box 5 to your income; rather, Box 5 tells you how much of the amount in Box 1a is eligible for the 20% deduction. It is a subset of your total dividends that receives special treatment.

Filing Requirements and Form 8995

To actually claim the deduction, you cannot simply report the income and hope for the best. Taxpayers must typically use IRS Form 8995 (Qualified Business Income Deduction Simplified Computation) or Form 8995-A if their income is above certain thresholds.

Form 8995 is where you aggregate your Section 199A dividends from all sources. You will list the total qualified REIT dividends, calculate 20% of that value, and then ensure it fits within the overall taxable income limits. The resulting figure is then transferred to your Form 1040, reducing your final taxable income before the tax rate is applied.

Investment Strategy: Integrating 199A Dividends into Your Portfolio

Understanding the tax mechanics of Section 199A is only half the battle; the real value lies in using this knowledge to make smarter investment decisions.

Asset Location: Taxable vs. Tax-Advantaged Accounts

One of the most critical decisions an investor makes is “asset location”—deciding which investments to hold in taxable brokerage accounts versus tax-advantaged accounts like IRAs or 401(k)s.

Historically, tax experts recommended holding REITs in IRAs because their dividends were taxed at high ordinary income rates. However, with the introduction of the Section 199A deduction, the “cost” of holding REITs in a taxable account has decreased. Since the 199A deduction is only available for taxable income, holding a REIT in a taxable account allows you to utilize the 20% deduction. If you hold that same REIT in an IRA, the deduction is effectively wasted because the income isn’t taxed anyway (until withdrawal). For high-net-worth individuals, this may shift the calculus on where to place real estate-heavy funds.

Long-term Wealth Building through Tax Efficiency

The Section 199A dividend is currently scheduled to expire, or “sunset,” at the end of 2025, along with many other provisions of the TCJA, unless Congress acts to extend it. For the proactive investor, this creates a window of opportunity to maximize tax-efficient growth.

By focusing on investments that yield Section 199A dividends, you are essentially receiving a government-subsidized boost to your yield. When combined with the power of compounding, the 20% reduction in tax liability can lead to significantly higher portfolio values over time. As part of a diversified financial strategy, monitoring these dividends allows you to keep more of what you earn, reinvesting the tax savings back into the market to accelerate your journey toward financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.