Navigating the American tax system is often straightforward for traditional W-2 employees, whose employers withhold taxes from every paycheck. However, for the millions of Americans participating in the “1099 economy”—freelancers, small business owners, independent contractors, and investors—the responsibility of tax withholding shifts from the employer to the individual. This shift necessitates a deep understanding of estimated tax payments.

Failing to manage these payments correctly can lead to significant financial stress, including hefty underpayment penalties and a massive, unexpected bill come April. This guide provides a professional roadmap for managing your quarterly tax obligations, ensuring your business and personal finances remain on solid ground.

Understanding the Foundation of Estimated Tax Payments

The United States operates on a “pay-as-you-go” tax system. This means the Internal Revenue Service (IRS) requires tax payments to be made as income is earned throughout the year, rather than in one lump sum at the end of the fiscal year. While W-2 employees fulfill this through payroll withholding, those with other income sources must use Form 1040-ES to calculate and pay their share.

Who Is Required to Make Estimated Payments?

Generally, you must make estimated tax payments if you expect to owe at least $1,000 in taxes for the current year after subtracting your federal income tax withholding and refundable credits. This applies to sole proprietors, partners, and S-corporation shareholders. If you are a freelancer or a side-hustler earning significant income outside of a traditional job, you likely fall into this category. Additionally, if you receive significant income from interest, dividends, alimony, or capital gains, you may be required to pay estimated taxes even if you have a full-time job.

The “Safe Harbor” Rule

To protect taxpayers from penalties due to unpredictable income, the IRS provides “Safe Harbor” guidelines. Generally, you will not face an underpayment penalty if you pay at least 90% of the tax shown on your current year’s return or 100% of the tax shown on your return for the prior year, whichever is smaller. For high-income earners (those with an adjusted gross income over $150,000), the prior-year safe harbor requirement increases to 110%. Understanding these benchmarks is critical for financial planning, as they provide a clear target for your quarterly outlays.

Consequences of Underpayment

Ignoring estimated tax obligations is not merely a matter of delayed payment; it carries a financial cost. The IRS charges interest-based penalties for underpayment, calculated based on how much you owed and how late the payment was. Even if you are due a refund at the end of the year, you can still be penalized if your quarterly payments were insufficient or late during the earlier periods of the year.

Calculating Your Quarterly Tax Liability

One of the most daunting aspects of estimated taxes is the calculation process. Because you are paying tax on money you are currently earning, you must forecast your annual income with reasonable accuracy.

Estimating Adjusted Gross Income (AGI)

The first step is to estimate your total income, deductions, and credits for the year. For established businesses, using last year’s tax return as a baseline is the most effective strategy. However, if your business is growing rapidly or facing a downturn, you must adjust these figures. Start by calculating your gross business income and subtracting necessary and ordinary business expenses—such as marketing, software subscriptions, and home office costs—to arrive at your net profit.

Accounting for Self-Employment Tax

For many, the most significant “surprise” in the world of independent income is the self-employment tax. When you are an employee, you pay 7.65% of your income toward Social Security and Medicare, and your employer matches that 7.65%. When you are self-employed, you are both the employer and the employee, meaning you are responsible for the full 15.3%. When calculating your estimated payments, you must include this self-employment tax in addition to your standard income tax.

Utilizing Form 1040-ES

The IRS provides a specific worksheet within Form 1040-ES (Estimated Tax for Individuals) to help you navigate these calculations. This worksheet guides you through the process of estimating your taxes, accounting for the standard deduction or itemized deductions, and incorporating any credits you expect to claim, such as the Child Tax Credit. While many modern accounting software tools automate this process, understanding the manual worksheet ensures you have a conceptual grasp of where your money is going.

Practical Methods for Making Payments

Once you have determined how much you owe, the next step is the actual transfer of funds to the Department of the Treasury. The IRS has modernized its systems significantly, offering several digital and traditional paths to compliance.

IRS Direct Pay and Online Accounts

For most individuals, IRS Direct Pay is the most efficient method. It allows you to pay directly from your checking or savings account without any processing fees. By creating an IRS Online Account, you can also view your past payment history, see digital copies of select notices, and track your total balance owed. This level of transparency is vital for maintaining accurate financial records.

The Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is excellent for individuals, the EFTPS is often the preferred choice for business entities or those who prefer to schedule payments far in advance. EFTPS is a free service provided by the U.S. Department of the Treasury. It requires a separate registration process and the mailing of a PIN, so it is best to set this up well before a payment deadline. EFTPS is highly secure and offers a detailed paper trail that is invaluable during a tax audit.

Traditional Mail and Vouchers

For those who prefer a non-digital approach, the IRS still accepts checks or money orders mailed with a payment voucher. These vouchers are found at the end of the Form 1040-ES packet. If you choose this method, it is highly recommended to use certified mail with a return receipt requested. This provides proof of mailing, which is your only defense if a payment is lost in the mail or delayed past the deadline.

Deadlines, Documentation, and Financial Strategy

Estimated tax payments are not due on a standard “every three months” quarterly schedule. The deadlines follow a specific logic that every business owner must memorize.

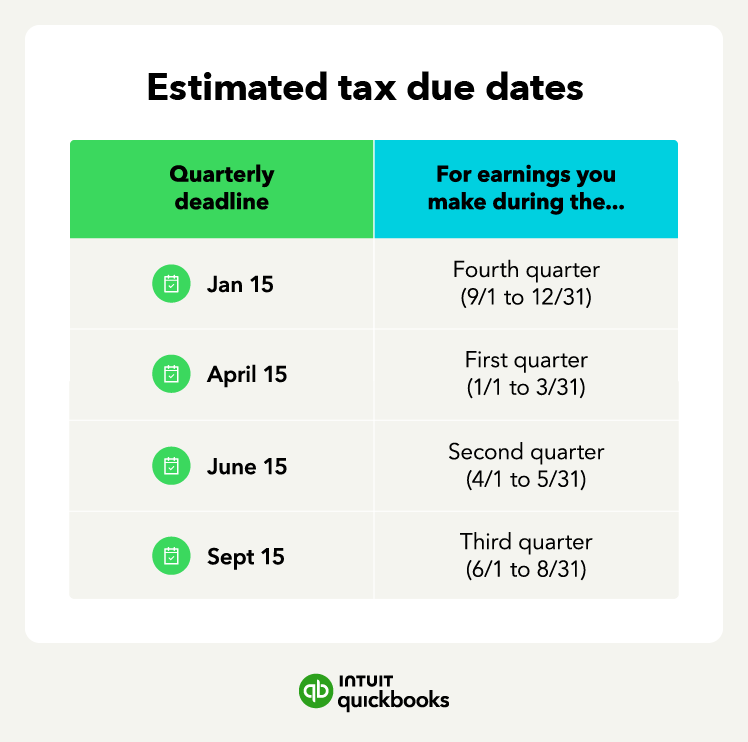

The Four Critical Deadlines

The IRS divides the year into four payment periods. For a standard calendar year, the deadlines are:

- April 15: For income earned Jan 1 – March 31.

- June 15: For income earned April 1 – May 31.

- September 15: For income earned June 1 – August 31.

- January 15 (of the following year): For income earned Sept 1 – Dec 31.

It is important to note that if these dates fall on a weekend or legal holiday, the deadline moves to the next business day. Mark these on your financial calendar to avoid the last-minute scramble.

The 30% Rule of Thumb

To avoid cash flow issues, many financial advisors recommend the “30% Rule.” Every time you receive a payment from a client or a distribution from your business, immediately move 30% of that gross amount into a high-yield savings account dedicated solely to taxes. This ensures that when the quarterly deadline arrives, the money is already set aside and has even earned a small amount of interest. This habit eliminates the “tax cliff” that many entrepreneurs face in April.

Leveraging Financial Tools for Record-Keeping

In the modern financial landscape, manual spreadsheets are increasingly being replaced by integrated accounting software. Tools that sync with your bank accounts can categorize expenses in real-time, providing a rolling estimate of your tax liability. Maintaining digital receipts and a clean general ledger is not just about convenience; it is a professional necessity. Accurate records allow you to maximize your deductions, effectively lowering your net income and, by extension, your quarterly tax burden.

Conclusion: A Proactive Approach to Financial Health

Making estimated tax payments is more than a legal obligation; it is a cornerstone of professional financial management. By moving from a reactive mindset to a proactive one, you eliminate the anxiety associated with “tax season.” Understanding who must pay, accurately calculating your liability, and utilizing the right payment channels allows you to focus on what matters most: growing your business and securing your financial future. When you treat the IRS as a regular “vendor” that requires quarterly settlement, you ensure that your path to wealth is not derailed by avoidable penalties or sudden liquidity crises.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.