Navigating the complexities of the tax system is often cited as one of the most stressful aspects of personal and business finance. Whether you are a salaried employee, a freelance professional, or a small business owner, the question “how do I pay my taxes” involves more than just writing a check to the government. It requires an understanding of your specific financial obligations, the digital infrastructure available for payments, and the strategic planning necessary to avoid penalties. In an era where financial literacy is a cornerstone of wealth management, mastering the tax payment process is an essential skill. This guide explores the multifaceted world of tax compliance, providing a roadmap for fulfilling your obligations efficiently and accurately.

Understanding the Landscape: Determining What You Owe

Before you can initiate a payment, you must first accurately calculate your liability. The modern tax landscape is nuanced, with different rules applying based on how you earn your income and your overall financial structure. Understanding these distinctions is the first step toward effective financial management.

Distinguishing Between Employee and Independent Contractor Status

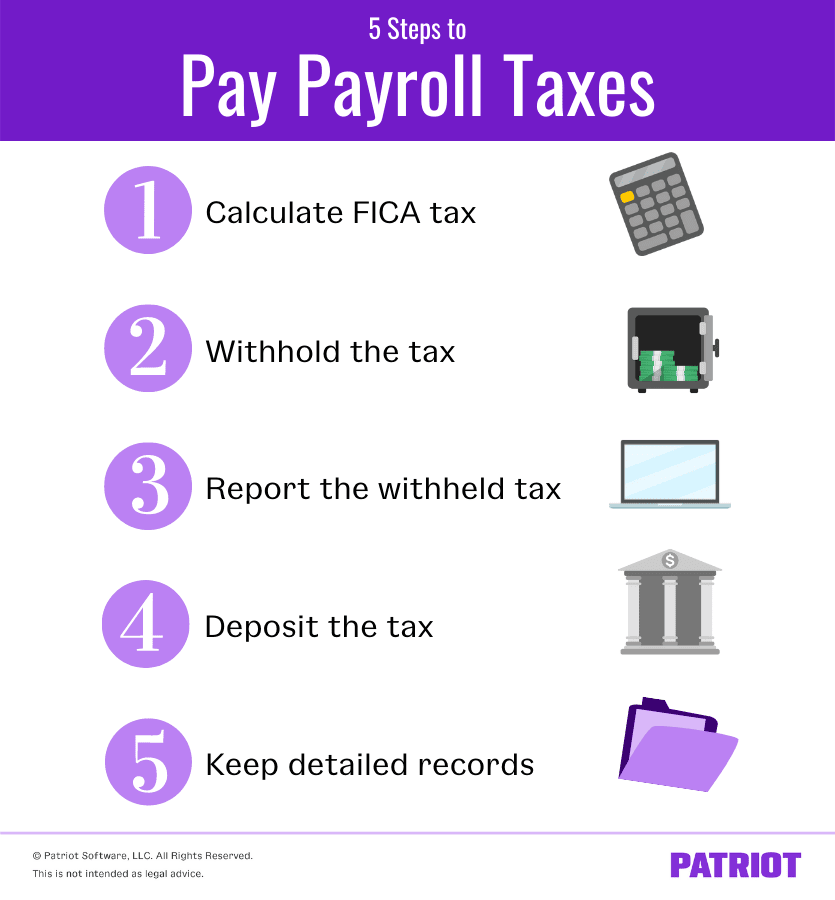

For most individuals, tax liability is determined by their employment status. W-2 employees typically have taxes withheld from their paychecks by their employers throughout the year. For these individuals, “paying taxes” often refers to the annual reconciliation process during the filing season to determine if enough was withheld. On the other hand, 1099 independent contractors and freelancers are responsible for the entirety of their tax burden, including both the employer and employee portions of Social Security and Medicare taxes. This distinction is critical because it dictates the frequency and method of your payments.

Identifying Taxable Income Streams

Taxable income extends beyond a standard salary. To pay your taxes correctly, you must account for capital gains from investments, dividends, interest earned on savings accounts, and even income from rental properties. In the “Money” niche, savvy investors recognize that every dollar earned is a potential tax liability. Failing to report secondary income streams can lead to audits and significant back-tax penalties. Comprehensive record-keeping of all inflows—whether from a side hustle or a brokerage account—is the foundation of an accurate tax filing.

The Role of Deductions and Credits

Paying your taxes also involves knowing how to legally reduce the amount you owe. Deductions, such as those for mortgage interest, student loan interest, or business expenses, reduce your taxable income. Tax credits, such as the Child Tax Credit or the Earned Income Tax Credit, provide a dollar-for-dollar reduction of your actual tax bill. Understanding the difference between the standard deduction and itemizing your deductions is a key component of financial strategy, ensuring that you pay exactly what you owe and not a penny more.

Navigating the Payment Portals: Your Digital Options

The Internal Revenue Service (IRS) and state tax agencies have moved aggressively toward digital transformation. Today, there are several secure, electronic ways to remit payment, each with its own set of advantages depending on your financial situation.

IRS Direct Pay: The No-Fee Standard

For individual taxpayers, IRS Direct Pay is often the most efficient method. This service allows you to pay your income tax directly from your checking or savings account without any additional fees. It is particularly useful for making one-time payments related to your annual return or for paying estimated taxes. The system provides immediate confirmation, which is vital for maintaining a digital paper trail of your financial compliance.

Utilizing the Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is excellent for individuals, the Electronic Federal Tax Payment System (EFTPS) is the gold standard for businesses and high-net-worth individuals with complex requirements. EFTPS is a free service provided by the U.S. Department of the Treasury that allows for the scheduling of payments up to 365 days in advance. This tool is essential for managing cash flow, as it allows you to automate your tax obligations well ahead of the deadline, ensuring you never miss a payment due to administrative oversight.

Credit and Debit Card Payments: Convenience vs. Cost

Technically, you can pay your taxes using a credit or debit card through authorized third-party processors. While this offers the convenience of “paying over time” (if using a credit card) or earning reward points, it comes with a catch. Processors charge a percentage-based convenience fee that can range from 1.8% to 2.5%. From a personal finance perspective, this is rarely the most cost-effective option unless the value of the rewards earned significantly outweighs the processing fee.

Managing Taxes for the Modern Entrepreneur and Side-Hustler

In the gig economy, the responsibility of tax payment shifts from the employer to the individual. This requires a more proactive approach to business finance and a disciplined savings strategy to ensure funds are available when the government comes calling.

The Necessity of Quarterly Estimated Tax Payments

If you expect to owe more than $1,000 in taxes for the year, the IRS generally requires you to make quarterly estimated tax payments. These payments are due in April, June, September, and January. Failing to make these payments can result in an “underpayment penalty,” even if you pay the full amount by the April filing deadline. Treating your tax obligation as a recurring monthly or quarterly business expense is a hallmark of professional financial management.

Calculating Self-Employment Tax

For those working for themselves, the self-employment tax rate is currently 15.3%. This covers Social Security (12.4%) and Medicare (2.9%). When you are an employee, you only pay half of this, and your employer pays the other half. When you are the boss, you pay both. Understanding this math is vital when setting your rates for clients; if you do not factor in the “tax bite,” you may find that your net take-home pay is significantly lower than anticipated.

Organizing Financial Records Throughout the Year

The most difficult way to pay your taxes is to start organizing your receipts on April 14th. Successful entrepreneurs utilize digital bookkeeping tools to track income and expenses in real-time. By categorizing expenses as they happen—such as home office costs, travel, and equipment—you can view your real-time tax liability throughout the year. This prevents the “tax season shock” that often plagues those who do not maintain a rigorous financial structure.

Leveraging Technology: Financial Tools to Streamline Your Filings

The intersection of finance and technology (FinTech) has birthed a variety of tools designed to take the guesswork out of tax payment. Leveraging these tools can save time and reduce the likelihood of human error.

Leading Tax Preparation Software Options

Software platforms like TurboTax, H&R Block, and FreeTaxUSA have revolutionized the way individuals interact with the tax code. These programs use “interview-style” formats to guide users through the filing process, identifying deductions that might otherwise be missed. For many, the cost of the software is an investment that pays for itself through optimized refunds and the peace of mind that the calculations are mathematically sound.

Cloud-Based Accounting for Business Owners

For those with more complex financial lives, cloud-based accounting software like QuickBooks, Xero, or FreshBooks is indispensable. These platforms can sync directly with your bank accounts, automatically flagging tax-deductible transactions. Many of these tools also offer a “Tax Planner” feature that estimates your quarterly payments based on your current profit-and-loss statements, allowing for precise financial forecasting.

When to Transition to a Certified Public Accountant (CPA)

While software is powerful, it has limitations. As your income grows or your business structure becomes more complex (e.g., forming an S-Corp or managing multi-state income), hiring a CPA becomes a strategic financial move. A CPA does more than just “file” your taxes; they provide year-round tax planning advice that can save you thousands of dollars in the long run. In the realm of business finance, professional expertise is often the most valuable tool in your arsenal.

Long-Term Financial Planning: Preparing for the Next Tax Season

Paying your taxes should not be viewed as an isolated annual event, but rather as a continuous component of your overall financial health. By integrating tax planning into your long-term wealth strategy, you can maximize your liquidity and minimize your stress.

Establishing an Emergency Tax Fund

One of the most effective personal finance habits is the creation of a dedicated tax savings account. High-yield savings accounts are excellent for this purpose. By automatically diverting a percentage of every check—typically 25% to 30% for freelancers—into a separate account, you ensure that the money is “gone” before you have a chance to spend it. This creates a buffer that protects your primary operating capital when tax deadlines arrive.

Adjusting Withholding for Optimized Cash Flow

For W-2 employees, receiving a massive tax refund is not necessarily a “win.” It essentially means you gave the government an interest-free loan for a year. From an investment perspective, that money could have been working for you in a brokerage account or a high-yield savings account. By adjusting your W-4 withholding with your employer, you can aim for a “break-even” point where you owe nothing and receive nothing, thereby maximizing your monthly cash flow.

Deadlines, Extensions, and Payment Plans

Finally, it is crucial to understand what to do if you cannot pay the full amount by the deadline. The most important rule in finance is: always file on time, even if you cannot pay. The penalty for failing to file is much higher than the penalty for failing to pay. If you find yourself in a financial bind, the IRS offers installment agreements and payment plans. While these accrue interest, they prevent the more aggressive collection actions that follow ignored tax debt. Facing the problem head-on with a structured payment plan is the only way to maintain your financial integrity and long-term creditworthiness.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.