In the modern financial landscape, the days of mailing paper checks and hoping they arrive at the Internal Revenue Service (IRS) on time are rapidly fading. As digital transformation reshapes our relationship with money, the IRS has evolved to offer several robust, secure, and efficient online payment platforms. Navigating these options is a critical skill for anyone managing personal finances, running a small business, or handling a side hustle. Understanding how to pay the IRS online is not just about convenience; it is about precision, record-keeping, and strategic cash flow management.

Navigating the IRS Digital Gateway: Choosing the Right Platform

Before initiating a transfer, it is essential to understand that the IRS offers different “front doors” for digital payments. Depending on your financial status—whether you are an individual filer or a business owner—the tools you use will vary in complexity and functionality.

IRS Direct Pay: The Individual Standard

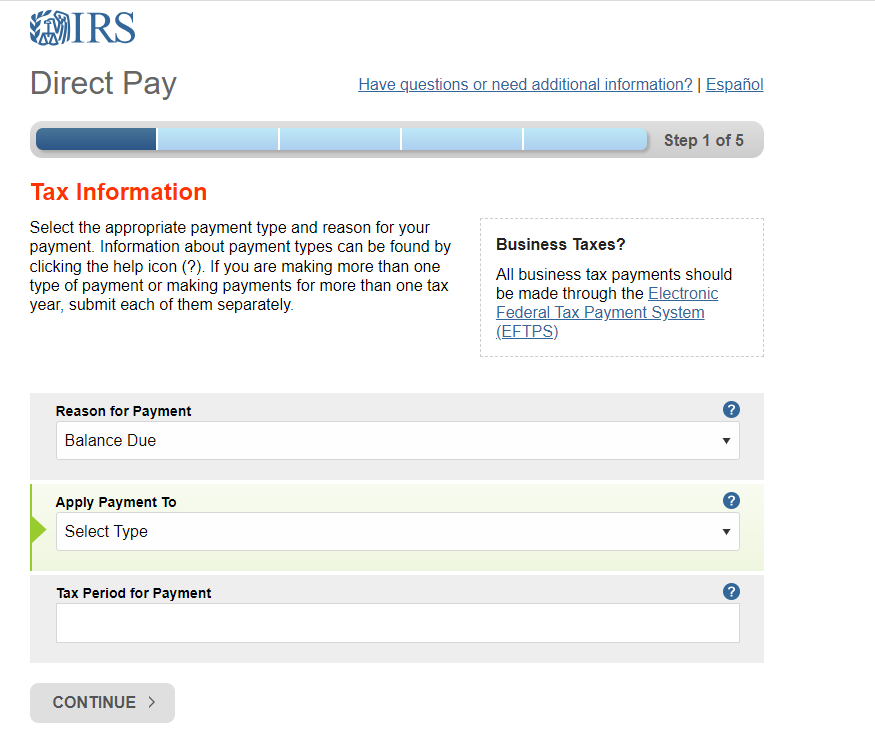

For the majority of individual taxpayers, IRS Direct Pay is the most efficient tool available. This service allows you to pay your income tax directly from your checking or savings account without any processing fees. One of the primary advantages of Direct Pay is that it does not require a registration process. You simply verify your identity using information from a previous year’s tax return, choose the reason for payment (such as “1040 Balance Due” or “Estimated Tax”), and authorize the transfer. From a personal finance perspective, this is the gold standard because it eliminates the lag time associated with physical mail.

The IRS Online Account: A Holistic Financial View

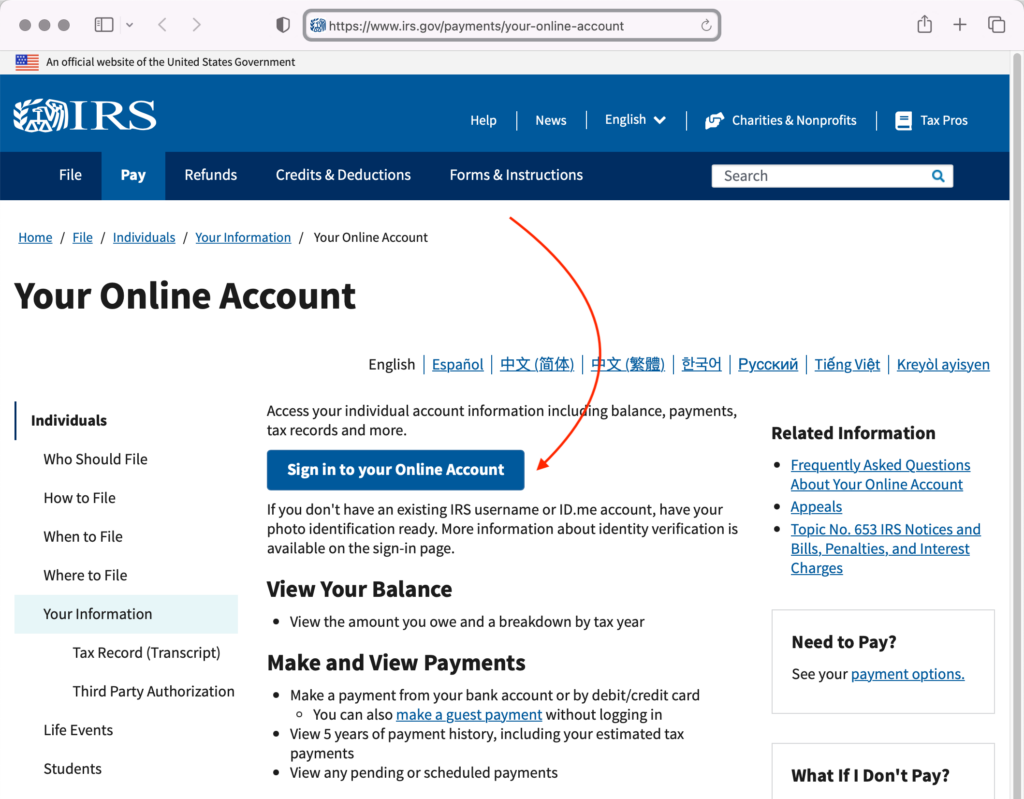

While Direct Pay is a transactional tool, the IRS Online Account is a comprehensive management dashboard. By creating an account (which now typically requires identity verification through ID.me), you gain access to your entire tax history. Here, you can view the total amount you owe, see your payment history for the last 24 months, and view key data from your most recent tax return. For those focused on long-term financial planning, the Online Account is indispensable because it provides a centralized location to ensure all credits and payments have been accurately applied to your file.

EFTPS: The High-Volume Business Solution

The Electronic Federal Tax Payment System (EFTPS) is a free service provided by the U.S. Department of the Treasury. While individuals can use it, it is primarily designed for business owners and high-net-worth individuals who need to make frequent, large payments. Unlike Direct Pay, EFTPS requires a formal enrollment process that can take five to seven days to complete, as a PIN is mailed to your physical address. However, once enrolled, it offers the highest level of scheduling flexibility, allowing users to schedule payments up to 365 days in advance.

Analyzing Payment Methods: Fees, Liquidity, and Incentives

Once you have selected a platform, the next decision involves the medium of exchange. In the world of personal finance, every transaction has a cost-benefit profile. Choosing between a bank transfer and a credit card payment can have significant implications for your bottom line.

Bank Transfers (ACH) and Financial Efficiency

The most fiscally conservative way to pay the IRS online is via an Automated Clearing House (ACH) transfer, often referred to as an “e-check.” As mentioned, platforms like Direct Pay offer this for free. For the savvy investor or budgeter, avoiding third-party processing fees is a priority. Using an ACH transfer ensures that 100% of your money goes toward your tax liability rather than being eroded by service charges.

Credit and Debit Card Payments: The Cost of Convenience

The IRS does not personally process credit or debit card payments; instead, it utilizes third-party payment processors like PayUSAtax or ACI Payments, Inc. These processors charge a convenience fee, which typically ranges from 1.82% to 1.98% for credit cards, or a flat fee for debit cards.

From a strategic money management perspective, paying by credit card is usually only advisable in two scenarios:

- The Rewards Gap: If you are “churning” a new credit card and need to meet a high spending requirement to earn a massive sign-on bonus, the value of that bonus may far outweigh the 2% processing fee.

- Short-term Liquidity: If you lack the cash to pay your tax bill in full but expect to have it within 30 days, using a credit card might be cheaper than the interest and penalties the IRS would charge for late payment—provided you pay the credit card balance off before interest kicks in.

Digital Wallets and Modern Integration

In a move toward modernizing government finance, the IRS has begun accepting payments through digital wallets like PayPal and Venmo via their third-party processors. This is particularly useful for freelancers or “gig economy” workers who may keep a portion of their earnings in these digital ecosystems. It allows for a seamless transition of digital income directly to tax obligations without needing to first transfer funds to a traditional bank account.

Security, Compliance, and Record-Keeping

When moving significant sums of money online, security is the paramount concern. The IRS has strict protocols to protect taxpayer data, but the responsibility of ensuring a secure transaction also falls on the taxpayer.

Verifying the Source and Avoiding Scams

One of the most common financial pitfalls is falling victim to phishing scams. It is a strict rule of thumb that the IRS will never initiate contact with taxpayers via email, text message, or social media to request personal or financial information. When paying online, always ensure you are on a “.gov” domain. By using the official IRS.gov website as your starting point, you protect your bank account information and your identity from malicious actors.

Identity Verification and the ID.me System

To access the most advanced features of the IRS website, such as viewing your transcripts or setting up a payment plan, you must verify your identity through ID.me. This process involves uploading a government ID and performing a biometric facial scan. While some find this process cumbersome, it is a critical layer of financial security designed to prevent identity thieves from filing fraudulent returns or diverting your tax payments.

Digital Paper Trails for Audits and Accounting

A major advantage of paying the IRS online is the instant confirmation. Unlike a check that might sit in a sorting facility for weeks, an online payment provides a confirmation number immediately upon completion. For those who use accounting software like QuickBooks or Mint, these digital receipts can be easily categorized. Maintaining a digital folder of these confirmation numbers is a vital component of a healthy financial record-keeping system, ensuring that if an audit or a discrepancy ever arises, you have timestamped proof of payment.

Strategic Cash Flow: Estimated Payments and Installments

For those who are not subject to traditional W-2 withholding—such as entrepreneurs, contractors, and investors—paying the IRS is not a once-a-year event. It is a quarterly requirement that demands disciplined cash flow management.

The Importance of Quarterly Estimated Payments

The U.S. tax system is a “pay-as-you-go” system. If you expect to owe more than $1,000 when you file your return, the IRS requires you to make estimated payments throughout the year (typically in April, June, September, and January). Paying these online is the most effective way to avoid “underpayment penalties.” By setting up recurring reminders to pay via Direct Pay or EFTPS, you ensure that your business or personal finances remain in good standing with the federal government.

Leveraging Online Payment Plans

Financial setbacks happen. If you find yourself in a position where you cannot pay your full tax liability, the IRS website offers an “Online Payment Agreement” tool. Instead of ignoring the debt—which leads to compounding interest and failure-to-pay penalties—you can apply for a short-term or long-term installment agreement online.

Setting up these plans digitally is significantly cheaper than doing so over the phone or via paper application. For example, the setup fee for a Direct Debit installment agreement initiated online is much lower than other methods. This is a crucial financial tool for maintaining your creditworthiness and preventing the IRS from taking more aggressive collection actions like wage garnishments or tax liens.

Final Thoughts on Frictionless Finance

Mastering the art of paying the IRS online is a hallmark of financial literacy. By moving away from manual processes and embracing the speed and security of digital platforms, you reduce the risk of errors, avoid unnecessary penalties, and maintain a clearer picture of your financial health. Whether you are using a simple ACH transfer through Direct Pay or managing complex business obligations via EFTPS, the ability to interface with the IRS digitally ensures that you are spending less time on bureaucracy and more time growing your wealth. In the end, the most successful taxpayers are those who treat their tax obligations with the same technological rigor they apply to their investments and savings.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.