The Great Crash of 1929 stands as the most devastating stock market collapse in the history of the United States. It was not merely a single day of red numbers on a ticker tape, but a systemic failure that signaled the end of an era of unprecedented optimism and the beginning of the Great Depression. For modern investors, financial analysts, and business students, understanding the 1929 crash is essential. It serves as a cautionary tale of what happens when speculative bubbles, excessive leverage, and structural economic weaknesses converge. To truly grasp the “why” behind the crash, one must look beneath the surface of the “Roaring Twenties” and examine the intricate financial mechanisms that first fueled the fire and then allowed it to consume the global economy.

The Roaring Twenties: A Decade of Dangerous Prosperity

The decade leading up to the crash was characterized by a sense of “permanent prosperity.” Following World War I, the United States entered an era of massive industrial expansion. Technological innovations like the automobile, radio, and household appliances became accessible to the masses, creating a consumer-driven boom that seemed unstoppable.

Post-War Economic Boom and Industrial Growth

During the 1920s, American manufacturing output rose significantly. The adoption of assembly-line production, pioneered by Henry Ford, lowered costs and increased efficiency. This industrial surge led to record corporate profits, which in turn attracted more investors to the stock market. Between 1920 and 1929, the Dow Jones Industrial Average (DJIA) increased nearly ten-fold. The prevailing sentiment was that the American economy had entered a “new era” where old rules of market cycles no longer applied.

The Rise of Consumer Credit and Margin Buying

Perhaps the most dangerous element of the 1920s was the democratization of debt. For the first time, ordinary citizens could buy products—and stocks—on credit. “Buying on margin” became a national obsession. Investors could purchase shares by paying as little as 10% of the stock’s value, borrowing the remaining 90% from their brokers. This extreme leverage amplified gains during the bull market, but it also meant that even a minor dip in prices could trigger “margin calls,” forcing investors to sell immediately to repay their loans. This house of cards relied entirely on the assumption that stock prices would never stop rising.

Structural Weaknesses in the Financial System

While the surface of the economy appeared polished and successful, the underlying financial infrastructure was riddled with cracks. The lack of a centralized regulatory body meant that the markets functioned more like a casino than a transparent financial exchange.

Lack of Regulatory Oversight and Banking Vulnerabilities

In 1929, the Securities and Exchange Commission (SEC) did not exist. There were few rules regarding corporate financial reporting, and “insider trading” was essentially a standard business practice. Investment pools—groups of wealthy investors—would frequently collude to “pump and dump” stocks, artificially inflating prices to lure in the public before selling off their holdings for a profit. Furthermore, the banking system was highly fragmented. Small, rural banks were particularly vulnerable, as they had tied much of their capital to the fluctuating fortunes of the agricultural sector.

Overproduction and the Agricultural Crisis

While the industrial cities were booming, rural America was already in a depression. During World War I, farmers had expanded production to meet global demand, often taking on heavy debt to buy more land and machinery. When European agriculture recovered after the war, a surplus of crops led to a collapse in prices. Farmers could no longer service their debts, leading to a wave of bank failures in the Midwest long before the Wall Street crash. Simultaneously, industrial sectors began to suffer from overproduction. By late 1929, many households had already purchased their cars and radios; demand slowed, but factories continued to churn out goods, leading to rising inventories and falling corporate valuations.

The Psychological Shift: From Euphoria to Panic

A market crash is as much a psychological event as it is a financial one. In 1929, the transition from irrational exuberance to blind panic happened with terrifying speed, exacerbated by the very tools that had built the boom.

The Tipping Point: Black Thursday and Black Tuesday

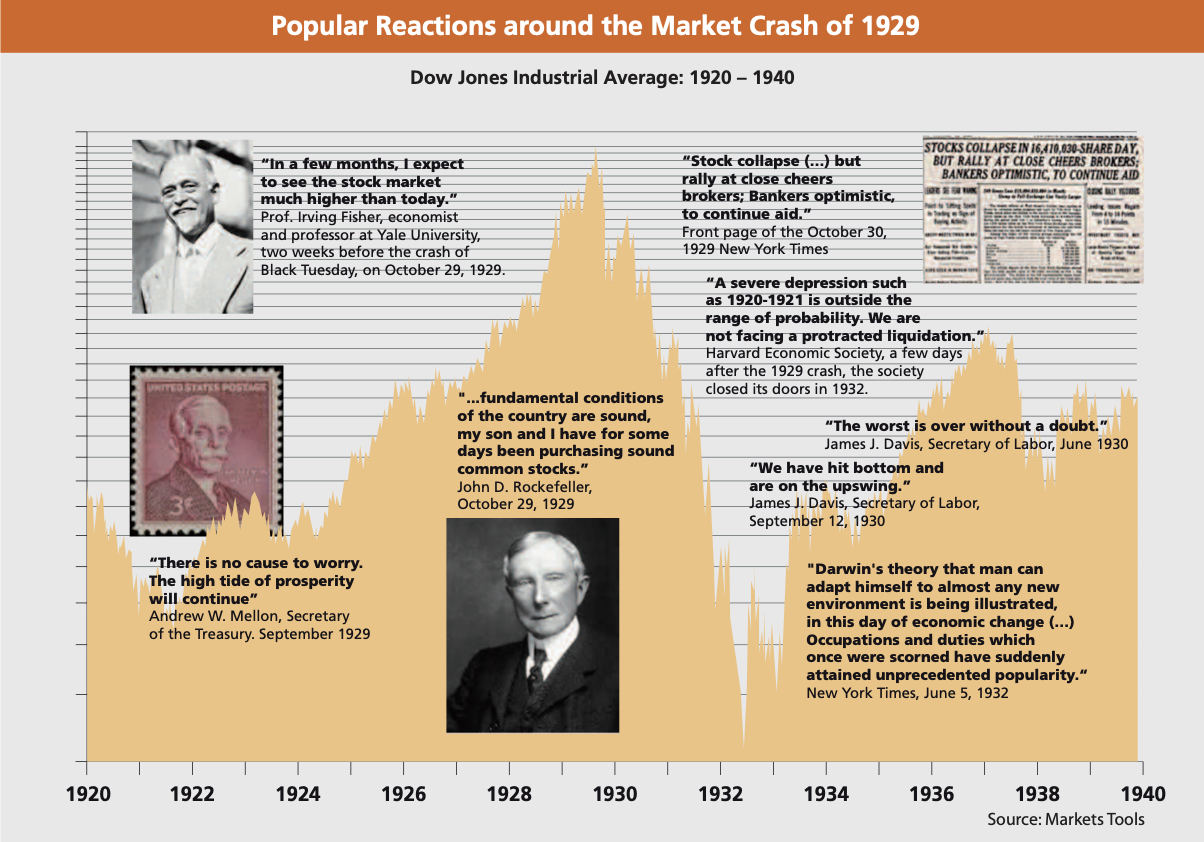

The market reached its peak in September 1929. Small tremors of instability began to appear throughout October as sophisticated investors started to quietly exit their positions. The real panic began on October 24, known as “Black Thursday,” when the market lost 11% of its value at the opening bell. While a group of powerful bankers attempted to stabilize the market by purchasing large blocks of stock, the reprieve was temporary. On October 29—”Black Tuesday”—the bottom fell out. Over 16 million shares were traded in a single day, a record that would stand for nearly 40 years. The ticker tape machines, unable to keep up with the volume of selling, ran hours behind, leaving investors in the dark about how much money they were losing in real-time.

The Role of the Federal Reserve’s Monetary Policy

Historians and economists, including Milton Friedman, have often pointed to the Federal Reserve’s mismanagement as a primary cause of the crash’s severity. In an attempt to curb the speculative fever of the late 20s, the Fed raised interest rates. While intended to cool the market, this move restricted liquidity at the exact moment the system needed it most. By tightening the money supply, the Fed made it harder for banks to survive the coming runs and for businesses to maintain operations. This contraction turned a necessary market correction into a full-scale financial collapse.

The Aftermath and Modern Parallels

The crash was the starting gun for a decade of economic misery. Its impact radiated outward from Wall Street, affecting every corner of the global economy and fundamentally changing the relationship between the government and the financial markets.

The Descent into the Great Depression

The stock market crash did not cause the Great Depression alone, but it was the primary catalyst. As stock prices plummeted, consumer wealth evaporated. Those who had bought on margin lost everything, and even those who hadn’t invested saw their savings vanish as banks failed. Consumption halted, leading to massive layoffs. By 1933, the unemployment rate in the United States hit 25%. This “vicious cycle” of reduced spending and increased unemployment defined the 1930s, proving that the health of the financial markets was inextricably linked to the welfare of the average citizen.

Lasting Regulatory Changes: The Birth of the SEC

In response to the crash, the U.S. government overhauled the financial system. The Securities Act of 1933 and the Securities Exchange Act of 1934 were passed to restore public confidence. These laws required corporations to provide full disclosure of their financial health and created the SEC to police the markets. Additionally, the Glass-Steagall Act was enacted to separate commercial banking from investment banking, preventing banks from using depositors’ money to gamble on the stock market. These regulations formed the bedrock of the modern financial system, designed to ensure that the speculative excesses of the 1920s could never happen again in the same way.

Investing Lessons for the Modern Era

Nearly a century later, the lessons of 1929 remain remarkably relevant. While the technology has changed—from paper ticker tapes to high-frequency trading algorithms—human psychology and the mechanics of financial bubbles remain the same.

Understanding Market Cycles and Sentiment

One of the key takeaways from 1929 is that “this time is different” are the four most dangerous words in investing. Every major crash is preceded by a period where investors believe that traditional metrics—like Price-to-Earnings (P/E) ratios—no longer matter. Whether it was the Dot-com bubble of 2000, the housing crisis of 2008, or the speculative fervor in crypto and tech today, the pattern of euphoria followed by a “reversion to the mean” is a constant of the financial world.

The Importance of Diversification and Liquidity

The 1929 crash highlighted the danger of over-concentration and the misuse of leverage. Investors who were “all-in” on equities with borrowed money were wiped out in days. For the modern investor, this emphasizes the need for a diversified portfolio and the maintenance of adequate liquidity. Liquidity—the ability to access cash without selling assets at a loss—is the ultimate insurance policy against market volatility. By studying the mistakes of 1929, today’s market participants can better navigate the complexities of the modern financial landscape, recognizing that while markets are a powerful tool for wealth creation, they require vigilance, discipline, and a healthy respect for risk.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.