Determining how much home loan you can qualify for is the critical first step in the journey toward homeownership. It is a process that blends personal financial goals with the rigid risk-assessment formulas used by lending institutions. While many prospective buyers begin their search by browsing listings online, the most successful buyers start by looking at their own balance sheets. Understanding your borrowing capacity prevents the heartbreak of falling in love with a property that is financially out of reach and ensures that your future mortgage remains a manageable part of your lifestyle rather than a source of “house poor” stress.

Lenders do not just look at a single number; they evaluate a mosaic of financial indicators to determine your creditworthiness and repayment capacity. This guide will break down the complex variables—from debt ratios to credit nuances—that dictate exactly how much a bank is willing to lend you.

Understanding the Fundamentals of Mortgage Eligibility

Before a lender puts a dollar amount on your pre-approval letter, they conduct a deep dive into your financial history. Their primary goal is to mitigate risk. They need to be reasonably certain that if they lend you hundreds of thousands of dollars, you have both the means and the character to pay it back over 15 to 30 years.

The Critical Role of the Debt-to-Income (DTI) Ratio

The Debt-to-Income ratio is perhaps the most significant factor in the qualification equation. It is a percentage that represents how much of your gross monthly income goes toward paying debts. Lenders typically look at two types of DTI: “front-end” and “back-end.” The front-end ratio calculates your projected housing expenses (mortgage, taxes, insurance) against your income. The back-end ratio—which lenders weigh more heavily—includes all monthly debts, such as car loans, student loans, and credit card minimums. Most conventional lenders prefer a back-end DTI of 36% or lower, though some programs, like FHA loans, may allow for up to 43% or even 50% in specific circumstances.

Credit Score Impact on Borrowing Power

Your credit score is the lens through which lenders view your financial reliability. It doesn’t just determine if you can get a loan; it determines the interest rate you receive, which directly impacts your monthly payment and, consequently, the total loan amount you qualify for. A buyer with a 760 score might qualify for a $400,000 loan at a 6% interest rate, while a buyer with a 620 score might be offered an 8% rate. That 2% difference increases the monthly payment significantly, which might force the lower-score buyer to settle for a much smaller loan to keep their DTI within acceptable limits.

Income Stability and Employment History

Lenders prioritize consistency. Generally, you need to demonstrate at least two years of steady employment, ideally within the same field. For salaried employees, this is straightforward. However, for self-employed individuals or those with commission-based roles, lenders will often take a two-year average of net income. If your income has fluctuated significantly or if you have recently changed careers, a lender may view your application with more scrutiny, potentially lowering the maximum loan amount they are willing to offer until stability is proven.

The Core Financial Metrics Lenders Evaluate

Once the baseline eligibility is established, lenders apply specific mathematical formulas to determine the maximum loan amount. These metrics provide a standardized way to compare your financial health against the requirements of the secondary mortgage market.

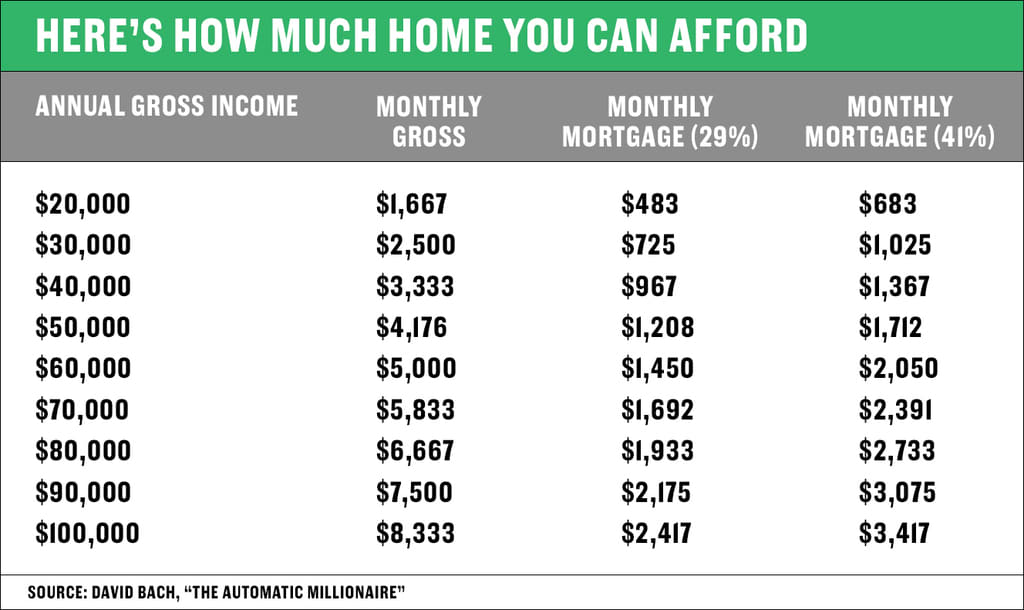

The 28/36 Rule Explained

A classic benchmark in the financial industry is the 28/36 rule. This guideline suggests that a household should spend no more than 28% of its gross monthly income on total housing expenses and no more than 36% on total debt servicing. For example, if your household earns $10,000 gross per month, the 28/36 rule suggests your mortgage payment should not exceed $2,800, and your total monthly debt payments (including the mortgage) should stay under $3,600. If you have no other debts, you might be able to push that housing expense slightly higher, but if you have a $800 monthly car payment, your available room for a mortgage payment shrinks significantly.

Loan-to-Value (LTV) Ratio and the Down Payment

The Loan-to-Value ratio is the relationship between the amount of the loan and the appraised value of the property. If you buy a $500,000 home and provide a $100,000 down payment, your loan is $400,000, resulting in an 80% LTV. Lenders prefer lower LTVs because the borrower has more “skin in the game.” If your down payment is less than 20%, you will typically be required to pay Private Mortgage Insurance (PMI), which adds to your monthly cost and reduces the total loan amount for which you can qualify.

Liquid Assets and Cash Reserves

Beyond the down payment and closing costs, lenders want to see “reserves.” Reserves are liquid assets (savings, stocks, or money market accounts) that remain after the home purchase is finalized. Most lenders like to see at least two to six months’ worth of mortgage payments in reserve. Having substantial cash reserves can sometimes compensate for other weaknesses in an application, such as a slightly higher DTI or a lower credit score, thereby helping you qualify for a higher loan amount.

Factors That Can Increase or Decrease Your Qualification Limit

Qualification is not a static number; it is a moving target influenced by external economic factors and internal financial decisions. Understanding these variables allows you to time your application for maximum benefit.

Interest Rate Fluctuations and Their “Buying Power” Effect

Interest rates are the most volatile variable in the qualification process. When interest rates rise, your “buying power” falls. Even a 0.5% increase in the market interest rate can result in a buyer qualifying for tens of thousands of dollars less. This is because the higher interest rate increases the monthly payment for every dollar borrowed. To keep the total payment within the DTI limits, the lender must reduce the principal loan amount. Monitoring the Federal Reserve’s signals and locking in a rate at the right time is a crucial strategy for maximizing your loan.

The Impact of Co-borrowers and Joint Applications

Applying for a home loan with a spouse or partner can significantly boost your qualification limit because the lender considers the combined gross income of both parties. However, there is a catch: lenders also consider the combined debt. Furthermore, in most joint applications, lenders will use the lower of the two applicants’ credit scores to determine the interest rate. If one partner has a high income but a very poor credit score, their presence on the application might actually hinder the loan terms or the total amount qualified for.

Existing Monthly Obligations and “Hidden” Debts

It is not just student loans and car notes that count toward your debt. Lenders also look at alimony, child support payments, and even co-signed loans for family members. If you have co-signed a car loan for a sibling, that entire monthly payment is usually counted as your debt unless you can prove the sibling has made the payments on time for the last 12 months. Clearing these “hidden” obligations or small balances before applying can free up significant DTI space.

Proactive Steps to Maximize Your Home Loan Potential

If the initial estimates of your borrowing power are lower than you hoped, there are several strategic moves you can make to improve your standing in the eyes of a mortgage underwriter.

Improving Your Credit Profile and Mix

Increasing your credit score by even 20 or 30 points can move you into a higher “tier,” lowering your interest rate and increasing your loan capacity. Start by ensuring your credit utilization—the amount of credit you use compared to your limits—is below 30%. Avoid opening new credit lines or making large purchases (like a new furniture set on credit) in the six months leading up to a home loan application. A clean, disciplined credit history is the best tool for securing a larger loan.

Reducing Revolving Debt to Lower DTI

Since DTI is a ratio of debt to income, you can improve it in two ways: making more money or owing less. While a salary raise isn’t always within immediate reach, paying off a credit card or a small personal loan is often achievable. Eliminating a $300 monthly payment can sometimes increase your home loan qualification by $40,000 to $50,000, depending on current interest rates.

Saving for a Larger Down Payment

While it may take longer to enter the market, a larger down payment does two things: it reduces the amount you need to borrow and eliminates or reduces the cost of PMI. By lowering your monthly obligation to the bank, you make the remaining loan safer for the lender, which may lead to more flexible underwriting and a more favorable overall financial package.

Moving From Pre-Qualification to Pre-Approval

As you move closer to making an offer, it is essential to distinguish between a casual estimate and a formal commitment from a lender.

The Difference Between Pre-Qualified and Pre-Approved

“Pre-qualification” is usually based on unverified information you provide to a lender. It gives you a ballpark figure but holds little weight in a competitive real estate market. “Pre-approval,” however, involves a hard credit check and the submission of financial documents (W2s, tax returns, bank statements). A pre-approval letter is a statement from the lender that they have vetted your finances and are prepared to lend you a specific amount.

Documentation Requirements for a Formal Qualification

To finalize how much you can qualify for, be prepared to provide a “paper trail” for everything. This includes the last two years of federal tax returns, the last two months of bank statements, pay stubs covering the last 30 days, and documentation of any other assets or liabilities. Organized documentation speeds up the process and gives the lender confidence in your financial transparency.

Finding the Right Lender and Loan Product

Finally, the “how much” can vary between lenders. Different institutions have different “appetites” for risk. A local credit union might have more flexible manual underwriting than a large national bank. Additionally, different loan products—such as VA loans for veterans, USDA loans for rural properties, or FHA loans for first-time buyers—have different DTI and credit requirements. Shopping around with at least three different lenders is the best way to ensure you are seeing the absolute maximum loan you can qualify for under the best possible terms.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.