In the intricate world of business finance, few concepts are as fundamental yet frequently misunderstood as debits and credits. Far from being simple indicators of “good” or “bad” financial movements, these terms represent the twin pillars of the double-entry accounting system – a methodology so robust it has underpinned global commerce for centuries. For anyone looking to gain a deeper understanding of how businesses track their financial health, from entrepreneurs managing their startups to seasoned investors deciphering financial statements, demystifying debits and credits is an essential first step. They are the directional signals that guide every financial transaction, ensuring accuracy, transparency, and a balanced view of a company’s economic position.

This article will pull back the curtain on these core accounting principles, explaining their purpose, how they interact within the accounting equation, and why mastering their application is crucial for sound financial management. By the end, you’ll not only understand what debits and credits are but also appreciate their indispensable role in portraying a true and fair view of an organization’s financial narrative.

The Foundation of Accounting: Understanding Double-Entry

At its heart, accounting seeks to provide a systematic record of an entity’s financial transactions. The double-entry system, popularized by Luca Pacioli in the late 15th century, revolutionized this process by introducing a simple yet profound rule: every financial transaction affects at least two accounts. This principle of duality is where debits and credits find their purpose, acting as the balancing mechanism that keeps the entire financial system in equilibrium.

Why Double-Entry Accounting Reigns Supreme

The longevity and universal adoption of the double-entry system are testaments to its inherent advantages. Firstly, it provides an unparalleled level of accuracy. By requiring every transaction to have an equal and opposite effect, it automatically builds in a self-checking mechanism. If the total debits do not equal the total credits, an error has occurred, which can then be traced and corrected. This inherent balance minimizes mistakes and enhances the reliability of financial records. Secondly, it offers a comprehensive view of a business’s financial health. Unlike single-entry systems that might only track cash inflows and outflows, double-entry accounting captures the full spectrum of assets, liabilities, equity, revenues, and expenses, painting a complete picture of a company’s financial position at any given time. This holistic perspective is vital for decision-making, performance analysis, and regulatory compliance.

The Concept of Duality: Every Transaction Has Two Sides

Imagine buying a new laptop for your business. This single event isn’t just an expense; it simultaneously reduces your cash (an asset) and increases your equipment (another asset). Or consider selling a product: you’ve gained revenue (an increase in equity) and received cash (an increase in assets). Every single transaction, no matter how simple or complex, creates a dual impact on a business’s financial statements. This is the essence of duality. Debits and credits are the language we use to describe these two sides of the same coin, dictating how each account is affected to maintain the fundamental accounting equation: Assets = Liabilities + Equity. Without this dual impact, the financial picture would be incomplete and misleading, making it impossible to derive meaningful insights or create accurate financial reports.

Debits and Credits: Unpacking the Core Concepts

To truly grasp debits and credits, one must shed the common misconception that “debit” means bad or subtract, and “credit” means good or add. In accounting, these terms simply denote the side of an account where an entry is made. They are directional signals, not value judgments.

Debits: The Left Side of the Equation

In any accounting ledger or T-account (a visual representation used for teaching), debits are always recorded on the left side. A debit signifies an increase in assets or expenses, and a decrease in liabilities, equity, or revenue. For instance, when a company receives cash (an asset), the cash account is debited. When a company pays rent (an expense), the rent expense account is debited. It’s crucial to remember that a debit isn’t inherently a “bad” thing; it’s simply a recording method. Increasing an asset like cash or equipment is generally a positive development for a business, yet it is recorded as a debit.

Credits: The Right Side of the Equation

Conversely, credits are always recorded on the right side of an account. A credit signifies an increase in liabilities, equity, or revenue, and a decrease in assets or expenses. So, when a company takes out a loan (a liability), the loans payable account is credited. When a company sells goods or services, the revenue account is credited. Similarly, if cash is paid out (decreasing an asset), the cash account is credited. Just as with debits, a credit is a neutral term indicating the direction of the financial impact on a specific account type. An increase in revenue (a credit) is typically a very positive event for a business.

Beyond Positive and Negative: A Matter of Direction

The critical insight into debits and credits is to view them purely as directional indicators within the double-entry system. They don’t carry intrinsic positive or negative connotations. Instead, their meaning is determined by the type of account they are affecting. This is why a debit can represent both a “good” thing (like an increase in cash) and a “bad” thing (like an increase in expenses). Likewise, a credit can be “good” (like an increase in revenue) or “bad” (like a decrease in cash). The system is designed to track the movement of value, ensuring that for every value received, an equal value is given, and vice-versa, always maintaining the balance of the accounting equation.

The Accounting Equation and Account Types: Where Debits and Credits Live

The entire framework of debits and credits is built upon the fundamental accounting equation: Assets = Liabilities + Equity. Understanding how different account types relate to this equation is key to mastering debit and credit rules.

Assets, Liabilities, and Equity: The Pillars

- Assets are economic resources owned by the business that are expected to provide future economic benefits (e.g., cash, accounts receivable, inventory, property, plant, equipment).

- Liabilities are obligations of the business to other entities that must be settled in the future (e.g., accounts payable, loans payable, deferred revenue).

- Equity represents the owners’ residual claim on the assets of the business after deducting liabilities (e.g., owner’s capital, retained earnings, common stock).

The equation Assets = Liabilities + Equity must always remain in balance. This means that if an asset increases, there must be a corresponding increase in a liability or equity, or a decrease in another asset. Debits and credits are the tools used to record these changes while maintaining balance.

The Expanded Equation: Revenue and Expenses

To better track performance over a period, the accounting equation is often expanded to include revenue and expenses, which directly impact equity:

- Revenue represents the income generated from the ordinary activities of a business (e.g., sales revenue, service revenue). Revenue increases equity.

- Expenses are the costs incurred in the process of earning revenue (e.g., rent expense, salaries expense, utilities expense). Expenses decrease equity.

When revenue increases, equity increases. When expenses increase, equity decreases. Therefore, understanding how debits and credits affect these temporary equity accounts (which are eventually closed into permanent equity accounts) is crucial for accurate profit and loss reporting.

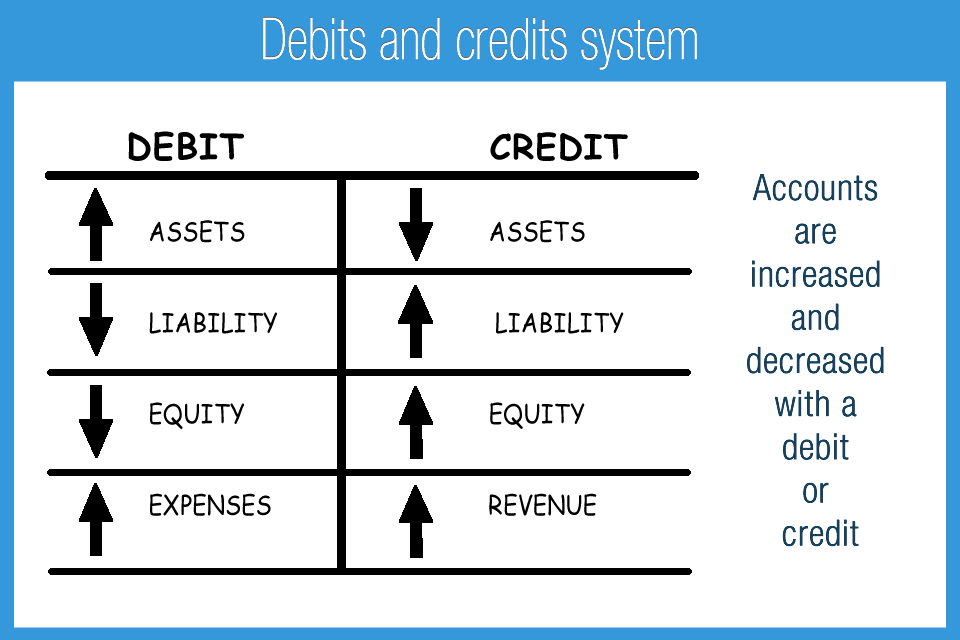

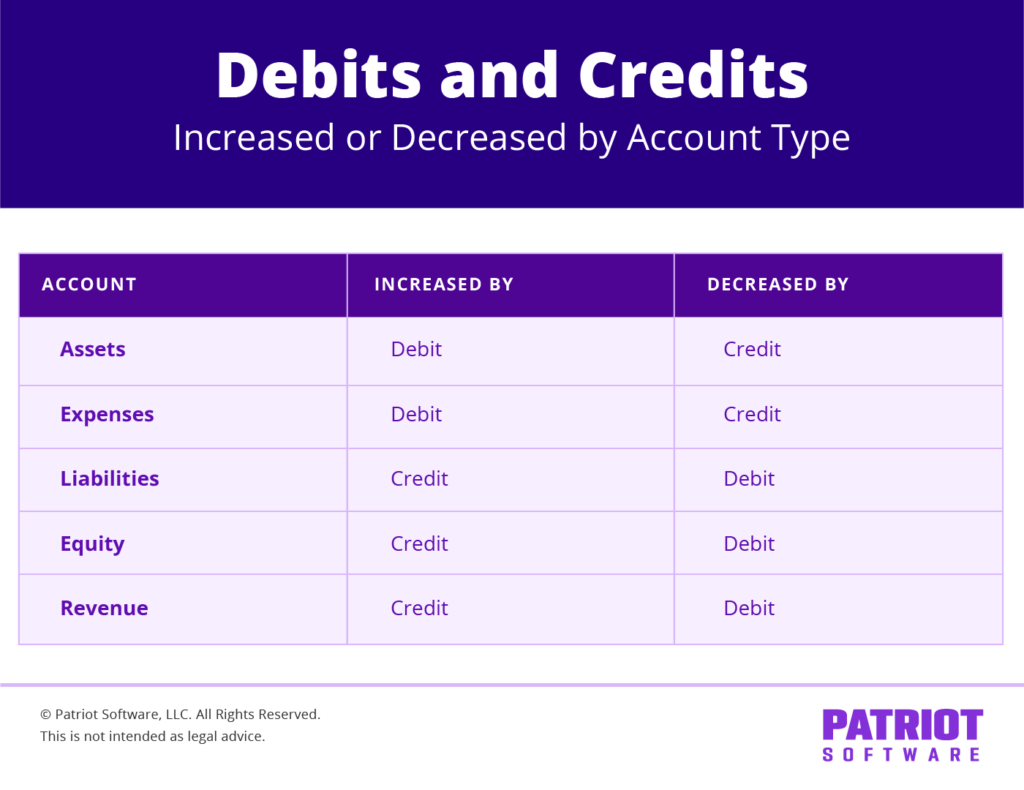

The Normal Balance: A Key Concept

Every account type has a “normal balance,” which is the side (debit or credit) on which increases to that account are recorded. Knowing an account’s normal balance makes it much easier to apply debit and credit rules:

- Assets: Normal balance is a debit. (Increases are debits, decreases are credits).

- Expenses: Normal balance is a debit. (Increases are debits, decreases are credits).

- Liabilities: Normal balance is a credit. (Increases are credits, decreases are debits).

- Equity: Normal balance is a credit. (Increases are credits, decreases are debits).

- Revenue: Normal balance is a credit. (Increases are credits, decreases are debits).

This concept of normal balance is the bedrock for recording transactions correctly. It’s the consistent rule that ensures the accounting equation remains balanced after every entry.

Practical Application: Journal Entries and the Ledger

Understanding debits and credits moves from theoretical knowledge to practical application through journal entries and the general ledger. These are the primary tools accountants use to record and organize financial transactions.

Recording Transactions: The Journal Entry

Every financial transaction is first recorded in a journal, often called the “book of original entry.” A journal entry details the date of the transaction, the accounts involved, the amounts debited and credited, and a brief explanation. For example:

- Transaction: A company pays $500 cash for office supplies.

- Analysis: Cash (an asset) decreases, so it is credited. Office Supplies (an asset) increases, so it is debited.

- Journal Entry:

Date Account Debit Credit [Date] Office Supplies $500 Cash $500 To record purchase of office supplies for cash Notice how the total debits ($500) perfectly equal the total credits ($500) in this entry, upholding the double-entry principle. Posting to the Ledger: Organizing the Data

After being recorded in the journal, each transaction’s debit and credit entries are then “posted” to the respective individual accounts in the general ledger. The general ledger is a collection of all the accounts a company uses, providing a complete record of each account’s balance. Each account in the ledger is typically represented as a T-account for simplicity, with debits on the left and credits on the right. Posting allows for a clear, organized view of all activity within a specific account, enabling accountants to easily determine its current balance. For instance, all cash debits and credits from various journal entries would be aggregated into the cash account in the ledger.

The Trial Balance: Ensuring Equilibrium

Periodically, usually at the end of an accounting period, a “trial balance” is prepared. This is a list of all general ledger accounts and their respective debit or credit balances. The primary purpose of a trial balance is to verify that the total of all debit balances equals the total of all credit balances. If they don’t match, it indicates that an error occurred in a journal entry or during the posting process, requiring investigation. While a trial balance doesn’t guarantee that all transactions were recorded correctly (e.g., if the wrong account was debited/credited but with the correct amount), it is a crucial internal check that confirms the arithmetical accuracy of the ledger.

Mastering the Rules: A Summary for Clarity

To simplify the application of debits and credits, a few mnemonic devices and a clear understanding of account types can be incredibly helpful. The fundamental rule remains: debits on the left, credits on the right, and for every debit, there must be an equal credit.

Debits Increase: Assets, Expenses, Dividends (DEAD)

A useful mnemonic for accounts that increase with a debit is DEAD:

- Debits

- Expenses

- Assets

- Dividends (though not explicitly discussed, dividends are withdrawals by owners, effectively decreasing equity, and thus increase with a debit).

So, if you are increasing an Asset or an Expense account, you will debit it. If you are decreasing one of these, you will credit it.

Credits Increase: Liabilities, Equity, Revenue (CLEAR)

For accounts that increase with a credit, think CLEAR:

- Credits

- Liabilities

- Equity

- And

- Revenue

If you are increasing a Liability, an Equity, or a Revenue account, you will credit it. Conversely, if you are decreasing one of these, you will debit it. These mnemonics can provide a quick reference point when analyzing transactions and preparing journal entries.

The Power of Balance: Why It Matters

The unwavering requirement for debits to equal credits is more than just an accounting formality; it is the bedrock of financial integrity. This balance ensures that the accounting equation always holds true, providing a consistent framework for financial reporting. Without it, financial statements would be unreliable, making it impossible for stakeholders – from business owners and managers to investors and lenders – to accurately assess a company’s financial performance and position. Mastering debits and credits isn’t just about recording numbers; it’s about understanding the financial flow of a business, enabling informed decisions, and building a foundation for sustainable growth.

In conclusion, debits and credits are not just technical terms but the very language of business finance. They are the essential tools that transform raw financial events into a coherent and balanced narrative, allowing businesses to track their journey, measure their success, and navigate the complex economic landscape with clarity and confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.