The question of how much to squirrel away for retirement is one that plagues many, regardless of their income level or career stage. Among the various avenues for long-term savings, the 401(k) stands out as a cornerstone of retirement planning for millions, primarily due to its tax advantages and often, the lucrative benefit of employer contributions. Determining the “right” percentage of your paycheck to allocate to your 401(k) isn’t a one-size-fits-all answer. It’s a deeply personal decision influenced by a myriad of factors, from your current financial obligations and income to your long-term aspirations and risk tolerance.

This guide aims to demystify the process, offering comprehensive insights into how to approach this critical financial decision. We’ll explore the fundamental mechanics of a 401(k), delve into common guidelines, and crucially, discuss how to tailor your contribution strategy to your unique financial landscape, ensuring you’re building a robust foundation for your future without sacrificing your present.

The Fundamentals: Why Your 401(k) Matters

Before we dive into percentages, it’s essential to grasp the fundamental importance and mechanics of a 401(k). Understanding these basics illuminates why this retirement vehicle is often hailed as a primary tool for securing your financial future.

What is a 401(k) and How Does It Work?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to invest a portion of their pre-tax or after-tax (Roth) salary into a diverse range of investment options, such as mutual funds, bond funds, and stock funds. The primary advantage of a traditional 401(k) is that contributions are made with pre-tax dollars, reducing your taxable income in the present. Your investments then grow tax-deferred until retirement, when withdrawals are taxed as ordinary income. A Roth 401(k), on the other hand, involves after-tax contributions, meaning your withdrawals in retirement are entirely tax-free, provided certain conditions are met. This choice often depends on whether you expect to be in a higher tax bracket now or in retirement.

Beyond the tax benefits, a 401(k) simplifies investing through payroll deductions, making consistent saving automatic. This “set it and forget it” approach is incredibly powerful, mitigating the temptation to spend money that might otherwise be allocated to savings.

The Power of Employer Match: Free Money You Shouldn’t Miss

Perhaps the single most compelling reason to contribute to a 401(k), especially for new investors, is the employer match. Many companies offer to match a certain percentage of your contributions, often dollar-for-dollar up to a specific limit (e.g., 100% match on the first 3% of your salary contributed, then 50% on the next 2%). This matching contribution is essentially “free money” – an immediate, guaranteed return on your investment that is hard to replicate elsewhere.

Failing to contribute at least enough to get your full employer match is akin to leaving money on the table. It’s a direct boost to your retirement savings that requires no additional effort beyond setting up your contributions. Calculating your employer’s match policy and ensuring you contribute at least that minimum should be your absolute first priority in 401(k) planning.

The Magic of Compound Interest

The long-term growth potential of a 401(k) is heavily influenced by compound interest. This phenomenon occurs when the interest you earn on your initial investment also starts to earn interest. Over decades, even modest contributions can grow into substantial sums, thanks to this exponential growth. The earlier you start contributing, the more time your money has to compound, underscoring the adage that “time in the market beats timing the market.” This principle highlights why consistency and starting early are far more impactful than waiting for the “perfect” moment to invest.

General Contribution Guidelines: Starting Points and Benchmarks

While personalized advice is key, several widely accepted guidelines offer excellent starting points for determining your 401(k) contribution percentage.

The “Traditional” 10-15% Rule

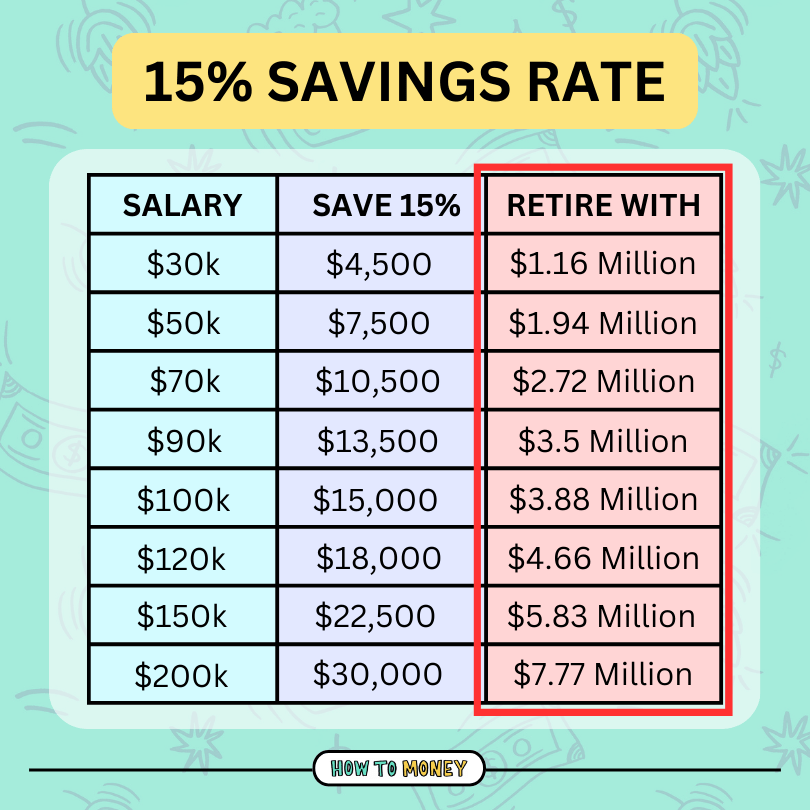

A common recommendation from financial advisors is to aim for contributing 10% to 15% of your gross income to retirement accounts, including your 401(k). This range is often considered a solid benchmark for most people to achieve a comfortable retirement, assuming they start saving in their 20s or early 30s. This percentage typically factors in both your contributions and any employer match. For example, if your employer matches 5% of your salary, you would aim to contribute an additional 5% to 10% to reach the 10-15% target.

The rationale behind this range is that it generally allows for sufficient growth over several decades to replace a significant portion of your pre-retirement income. However, this is a broad guideline and may need adjustment based on individual circumstances, such as starting late, aspiring for an early retirement, or living in an expensive area.

Prioritizing the Employer Match First

As mentioned, securing the full employer match should be your non-negotiable minimum contribution. If you’re struggling financially and can’t afford to save much, ensure you at least contribute enough to unlock every dollar of your employer’s matching contribution. This is an immediate 50% or 100% return on that portion of your investment, effectively doubling your money instantly. It’s a foundational step that no one should overlook.

The Power of Maxing Out: When and Why

For high-income earners or those with significant disposable income, the ultimate goal might be to max out your 401(k) contributions each year. The IRS sets annual limits on how much an individual can contribute (e.g., $23,000 for 2024, with additional “catch-up” contributions for those 50 and older). Maxing out your 401(k) not only significantly boosts your retirement savings but also maximizes your immediate tax benefits (for traditional 401(k)s). It demonstrates a strong commitment to financial independence and can significantly shorten the path to a robust retirement fund. While not feasible for everyone, it’s a worthwhile target to aim for as your income grows.

Tailoring Your 401(k) Strategy to Your Unique Situation

While general guidelines provide a useful starting point, your ideal 401(k) contribution percentage must be customized to your specific financial context.

Age and Career Stage

Your age plays a critical role. If you’re starting in your 20s, even a seemingly small percentage (e.g., 5-7% plus match) can grow substantially due to the power of compound interest. In your 30s and 40s, you might aim for the 10-15% benchmark, especially as your income likely increases. If you’re starting later in your 40s or 50s, you’ll likely need to contribute a much higher percentage, perhaps 15% to 20% or more, to catch up. This is where catch-up contributions (an additional amount allowed by the IRS for those 50 and over) become particularly valuable.

Current Income and Lifestyle

Your current income dictates your capacity to save. While a higher income generally allows for higher contributions, it’s crucial to balance savings with your current cost of living. Analyze your budget to identify how much disposable income you genuinely have. A frugal lifestyle can free up more funds for retirement, while an extravagant one might limit your ability to save aggressively. The goal is to find a sustainable percentage that doesn’t put undue strain on your current finances, as consistency is more important than sporadic large contributions.

Existing Debts and Financial Obligations

High-interest debt, such as credit card balances or personal loans, should often take precedence over aggressive 401(k) contributions beyond the employer match. The guaranteed return from paying off debt (e.g., avoiding 18%+ interest) typically outweighs the potential, but not guaranteed, returns from investments. Once high-interest debt is eliminated, you can then redirect those funds to accelerate your 401(k) contributions. Student loan debt and mortgages typically have lower interest rates, allowing for a more balanced approach where you can contribute to your 401(k) while also making payments.

Other Financial Goals (e.g., Down Payment, Education)

Life isn’t just about retirement. You might have other significant financial goals like saving for a down payment on a house, funding a child’s education, or starting a business. These goals can temporarily influence your 401(k) contribution percentage. It’s often a balancing act. For instance, you might contribute enough to get the employer match and then prioritize saving for a down payment in a separate, more liquid account. Once that goal is achieved, you can then ramp up your 401(k) contributions. A holistic financial plan considers all your goals simultaneously.

Risk Tolerance and Investment Horizon

Your comfort level with investment risk and the length of time you have until retirement (your investment horizon) also influence your strategy. If you’re decades away from retirement, you can generally afford to take on more risk, potentially leading to higher returns. As you get closer to retirement, you might shift to a more conservative investment mix to protect your accumulated wealth. While your contribution percentage is separate from your investment choices within the 401(k), a higher risk tolerance might encourage you to save more aggressively, anticipating greater long-term growth.

Advanced Strategies for Maximizing Your Retirement Savings

Once you’ve established your baseline, consider these strategies to further optimize your 401(k) and broader retirement plan.

Gradually Increasing Your Contribution Rate

One of the most effective strategies is to commit to increasing your contribution rate by 1% or 2% each year, especially when you receive a raise. If your company offers automatic enrollment with an annual increase, opt into it. You’ll barely notice the difference in your take-home pay, but these small, consistent increases can significantly impact your retirement nest egg over time, aligning with the principle of “paying yourself first.”

Understanding Catch-Up Contributions

For those aged 50 and over, the IRS allows additional “catch-up” contributions to 401(k)s. This provision is designed to help individuals who may have started saving late or want to accelerate their savings in the years leading up to retirement. This extra contribution amount (e.g., $7,500 for 2024) is above the standard annual limit and can be a powerful tool for boosting your retirement fund in a relatively short period.

Diversifying Beyond the 401(k): IRAs and Other Investment Vehicles

While your 401(k) is a powerful tool, it shouldn’t necessarily be your only retirement or investment vehicle. Consider diversifying your savings across different account types like a Roth IRA (for tax-free growth in retirement) or a traditional IRA (for tax-deductible contributions). These accounts offer broader investment choices and sometimes more flexibility. For higher earners, taxable brokerage accounts can also complement your retirement savings, offering liquidity for non-retirement goals or additional investment opportunities once tax-advantaged accounts are maxed out.

Rebalancing Your Portfolio

Periodically review the allocation of your investments within your 401(k). Over time, market fluctuations can cause your portfolio to drift from your intended asset allocation. Rebalancing means adjusting your holdings back to your desired percentages, which typically involves selling some assets that have performed well and buying more of those that have underperformed, helping you manage risk and stay aligned with your long-term strategy.

Integrating Your 401(k) into Your Holistic Financial Plan

Your 401(k) is a vital piece of your financial puzzle, but it’s crucial to view it within the context of your entire financial landscape.

The Importance of an Emergency Fund

Before aggressively investing beyond an employer match, establish a robust emergency fund. This fund, typically 3 to 6 months’ worth of essential living expenses, should be held in an easily accessible, liquid account (like a high-yield savings account). It acts as a financial buffer against unexpected events like job loss, medical emergencies, or significant home repairs, preventing you from needing to tap into your retirement savings prematurely.

Debt Management: A Prerequisite for Financial Freedom

As mentioned earlier, systematically addressing high-interest debt is a cornerstone of sound financial planning. The high interest rates on credit card debt can quickly erode any investment gains. Develop a debt repayment strategy, prioritize high-interest debts, and once they’re paid off, redirect those freed-up funds toward increasing your 401(k) contributions and other investments.

Regular Review and Adjustment

Your financial situation is not static. Life changes—your income grows, you incur new expenses, your goals evolve. Therefore, it’s crucial to review your 401(k) contribution percentage and overall financial plan at least once a year, or whenever significant life events occur (e.g., marriage, birth of a child, new job). This ensures your strategy remains aligned with your current reality and future aspirations.

Seeking Professional Financial Advice

If you feel overwhelmed by the complexities of retirement planning or have unique financial circumstances, consider consulting a qualified financial advisor. A professional can help you craft a personalized plan, optimize your investment strategy, and provide tailored advice to help you achieve your specific retirement goals. They can offer an objective perspective and expertise to navigate complex financial decisions.

In conclusion, the “right” percentage for your 401(k) contribution is a dynamic figure that evolves with your life. Start by securing the employer match, then aim for the 10-15% benchmark, and consistently review and adjust your contributions as your income and life circumstances change. Prioritize an emergency fund and debt repayment, and remember that consistency and starting early are your greatest allies in building a secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.