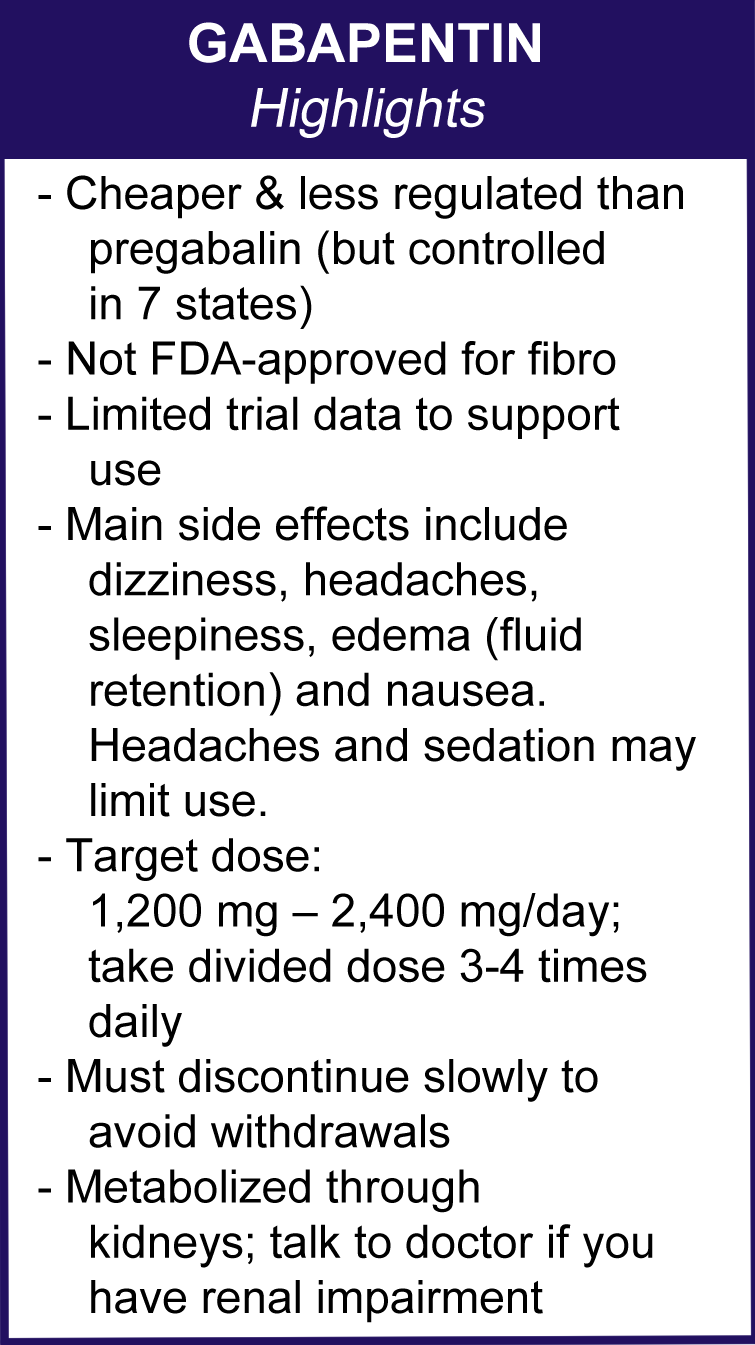

In the complex landscape of personal finance, healthcare expenses often represent one of the most unpredictable and substantial burdens. Among these, prescription drug costs play a critical role, directly impacting household budgets and access to necessary medical care. Understanding how your health insurance categorizes drugs, particularly through the “tier system,” is not just a matter of medical knowledge, but a crucial component of sound financial planning. This article delves into the specific case of gabapentin, a widely prescribed medication, to illuminate the broader financial mechanisms at play, helping you navigate pharmaceutical costs with greater insight and control.

Gabapentin, initially approved as an anti-epileptic drug, has found widespread utility in treating various conditions, including neuropathic pain, restless legs syndrome, and even certain anxiety disorders. Given its broad application, many individuals find themselves asking: “What tier drug is gabapentin?” The answer isn’t merely academic; it translates directly into the out-of-pocket costs you face at the pharmacy counter. By dissecting gabapentin’s typical tier placement and the factors influencing it, we unlock broader principles for managing your medication budget effectively.

Understanding Drug Tiers: The Foundation of Your Prescription Costs

The concept of drug tiers is central to how health insurance plans structure their prescription drug coverage. It’s a mechanism designed by Pharmacy Benefit Managers (PBMs), who negotiate prices with pharmaceutical manufacturers and manage formularies (lists of covered drugs) on behalf of insurance companies. For the consumer, understanding these tiers is paramount to predicting and managing prescription expenses.

The Tier System Explained

Most health insurance plans categorize prescription drugs into a multi-tier system, typically ranging from three to five tiers, each associated with a different level of cost-sharing for the patient.

- Tier 1: Preferred Generics. These are generally the least expensive drugs for patients. They are chemically identical to brand-name drugs but are produced and sold after the original patent has expired. Insurance plans heavily favor generics due to their lower cost, often requiring only a minimal copayment (e.g., $5-$15).

- Tier 2: Preferred Brand-Name Drugs. This tier includes brand-name medications that the insurance plan has negotiated favorable pricing for. While more expensive than generics, they offer a moderate level of coverage, with higher copayments than Tier 1 drugs (e.g., $20-$50).

- Tier 3: Non-Preferred Brand-Name Drugs. These are also brand-name medications, but the insurance plan either hasn’t negotiated as favorable a price or prefers alternative drugs in the same therapeutic class. They come with significantly higher copayments or coinsurance (e.g., $50-$100 or a percentage of the drug’s cost).

- Tier 4/5: Specialty Drugs. This highest tier is reserved for high-cost, often complex medications used to treat serious, chronic, or rare conditions (e.g., certain cancer drugs, biologics for autoimmune diseases). These drugs typically require specialized handling, administration, or monitoring, and come with the highest coinsurance rates, often a substantial percentage of the drug’s retail price (e.g., 20%-50%), potentially costing hundreds or even thousands of dollars per month.

Factors Influencing a Drug’s Tier Assignment

A drug’s tier placement isn’t arbitrary; it’s the result of complex negotiations and evaluations. Key factors include:

- Generic Availability: The most significant factor. Once a generic version of a drug becomes available, the original brand-name drug typically moves to a higher tier, and the generic takes its place in Tier 1.

- Negotiated Discounts: PBMs leverage their purchasing power to negotiate discounts with manufacturers. Drugs offering better rebates or discounts are more likely to be placed in lower, “preferred” tiers.

- Clinical Effectiveness and Cost-Effectiveness: While efficacy is paramount, PBMs also consider the overall value proposition. If multiple drugs treat the same condition, the one that offers comparable efficacy at a lower net cost to the plan may be preferred.

- Market Competition: The presence of many manufacturers for a generic drug often drives prices down, solidifying its Tier 1 status.

- Formulary Management Strategies: Insurance plans may implement strategies like step therapy (requiring patients to try a lower-tier drug first) or prior authorization for higher-tier drugs, influencing placement.

Gabapentin’s Place in the Formulary: A Financial Deep Dive

Given the intricacies of the tier system, where does gabapentin typically fall, and what are the financial implications for patients?

Gabapentin: A Generic Success Story

Gabapentin was originally marketed under the brand name Neurontin by Pfizer. However, its patent expired years ago, paving the way for numerous generic manufacturers to produce and distribute the drug. This shift to generic availability is the primary reason gabapentin is generally an affordable medication. The competition among generic manufacturers has driven its price down significantly.

Typical Tier Placement for Gabapentin

For the vast majority of patients with health insurance, gabapentin, in its generic form, is typically categorized as a Tier 1 (Preferred Generic) drug. This means that patients usually face the lowest possible copayment for their prescription, making it highly accessible and budget-friendly.

- Financial Advantage: A Tier 1 classification translates to minimal out-of-pocket costs, often just a few dollars per refill. This predictability allows patients to budget for their medication with confidence, reducing financial stress and promoting adherence to treatment plans.

- Brand-Name Exception: It’s important to note that if a patient specifically requests or is prescribed the brand-name Neurontin, it would almost certainly fall into a higher tier (e.g., Tier 2 or 3), resulting in significantly higher costs. However, most physicians will prescribe the generic version unless there is a very specific medical reason not to, given its identical active ingredient and efficacy.

- Extended-Release Formulations: There are also extended-release formulations of gabapentin, such as Gralise (for postherpetic neuralgia) and Horizant (for restless legs syndrome and postherpetic neuralgia), which are brand-name drugs with distinct patents. These specialized versions would be placed in higher tiers (Tier 2 or 3) and carry higher copayments or coinsurance than generic immediate-release gabapentin.

Variances Across Insurance Plans

While gabapentin’s generic status makes Tier 1 placement common, it’s crucial to remember that formulary decisions are made by individual insurance plans and their PBMs. Therefore, there can be slight variations:

- Different PBMs: Two different insurance companies might use different PBMs, leading to slightly different formularies and tier assignments for certain drugs, even generics.

- Plan Type: The specific type of health insurance plan (e.g., HMO, PPO, EPO, High-Deductible Health Plan, Medicare Part D, Medicaid) can influence its formulary. Medicare Part D plans, for instance, have their own specific rules and formulary structures.

- Formulary Changes: Formularies can change annually. While gabapentin’s generic status makes a major shift unlikely, it’s always wise to review your plan’s updated formulary each year.

Beyond the Copay: Hidden Costs and Financial Planning for Medications

While understanding drug tiers is foundational, the financial burden of prescriptions extends beyond just the copay. Savvy financial planning requires considering the broader context of your health insurance benefits.

Deductibles and Out-of-Pocket Maximums

For many insurance plans, particularly high-deductible health plans (HDHPs), you must meet an annual deductible before your insurance begins to pay for prescription drugs (or any other healthcare services) beyond negotiated rates. Even a Tier 1 drug like gabapentin might be paid for out-of-pocket at a discounted cash price until your deductible is met.

- Impact on Gabapentin: If your deductible is $2,000, and your gabapentin prescription costs $15 cash, you’ll pay that $15 for many months until your other healthcare expenses contribute enough to meet the deductible. While $15 is low, imagine if you were on multiple Tier 1 drugs and also had a specialty drug – these costs add up rapidly towards your deductible.

- Out-of-Pocket Maximum (OOPM): This is the most you’ll pay for covered healthcare services in a year. Once you reach your OOPM, your insurance plan pays 100% of covered costs. For those with chronic conditions requiring many medications, reaching the OOPM offers significant financial relief.

The Donut Hole and Other Medicare Considerations

For seniors enrolled in Medicare Part D (prescription drug coverage), the financial landscape can be particularly complex due to the “donut hole,” or coverage gap. While gabapentin’s low cost might keep many seniors from reaching the initial coverage limit that triggers the donut hole, it’s a critical financial consideration for those on multiple medications or higher-tier drugs.

- Coverage Gap Dynamics: After your total drug costs (what you and your plan have paid) reach a certain limit, you enter the coverage gap. Here, you typically pay a higher percentage of the cost for both generic and brand-name drugs until you reach the catastrophic coverage phase.

- Financial Planning for Seniors: Understanding Medicare Part D phases and considering supplemental insurance (Medigap) or Medicare Advantage plans (which may offer different drug coverage) is crucial for managing medication costs in retirement.

Specialty Formulations and Compounded Prescriptions

As mentioned, brand-name extended-release versions of gabapentin (Gralise, Horizant) exist and will always be in higher tiers. Additionally, in some rare cases, gabapentin might be prescribed in a compounded form (a custom-made medication prepared by a pharmacist). Compounded medications are often not covered by insurance or are covered at a significantly higher cost, as they fall outside standard formulary structures. While unlikely for standard gabapentin use, it’s a potential financial wildcard to be aware of.

Strategic Financial Navigation: Optimizing Your Prescription Budget

Understanding gabapentin’s tier status is a starting point, but proactive strategies are essential for overall financial wellness related to medications.

Proactive Formulary Review

Before selecting an insurance plan or during annual enrollment, always review the plan’s formulary for the coming year.

- Key Action: Check the tier placement and any restrictions (like prior authorization or step therapy) for all your current and anticipated medications. This prevents surprises and allows you to choose a plan that best covers your specific drug needs.

Leveraging Generic Options and Step Therapy

Always ask your doctor if a generic alternative is available for your prescribed medications.

- Gabapentin Example: Since generic gabapentin is widely available and affordable, ensure your doctor prescribes it unless a medical necessity dictates otherwise.

- Step Therapy: If your plan requires “step therapy” for a higher-tier drug, meaning you must try a lower-cost alternative first, discuss this with your doctor. Sometimes, a medical appeal can bypass this if the generic is ineffective or contraindicated.

Exploring Patient Assistance Programs and Discount Cards

For those struggling with medication costs, numerous resources can help:

- Manufacturer Coupons: For brand-name drugs (like Gralise or Horizant), manufacturers often offer coupons or patient assistance programs to reduce out-of-pocket costs.

- Discount Cards: Services like GoodRx, SingleCare, and Optum Perks can offer significant discounts, sometimes even beating your insurance copay, especially if you haven’t met your deductible.

- Non-Profit Assistance: Organizations like the Partnership for Prescription Assistance or specific disease foundations offer financial aid for medications.

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

These tax-advantaged accounts are powerful tools for managing healthcare expenses, including prescription drugs.

- HSAs (Health Savings Accounts): Available with HDHPs, HSAs allow you to contribute pre-tax money, which grows tax-free and can be withdrawn tax-free for qualified medical expenses. This is an excellent way to save for deductibles, copays, and even future medical costs in retirement.

- FSAs (Flexible Spending Accounts): Offered by employers, FSAs also allow pre-tax contributions for medical expenses. While they typically have a “use-it-or-lose-it” rule (though some plans allow rollovers), they’re effective for covering predictable annual medical costs.

Conclusion

Understanding “what tier drug is gabapentin” opens a window into the broader financial ecosystem of prescription medications. Its typical placement as a Tier 1 generic drug makes it an accessible and affordable option for many, underscoring the significant financial relief that generic availability brings to the healthcare system and individual budgets.

However, gabapentin’s case also serves as a critical reminder that while one drug might be affordable, the overall landscape of medication costs is intricate. From navigating deductibles and out-of-pocket maximums to understanding the nuances of Medicare Part D and leveraging financial planning tools like HSAs, proactive engagement with your health insurance and healthcare providers is paramount. By taking an informed, strategic approach to your prescription drug coverage, you can mitigate financial surprises, ensure adherence to vital treatments, and maintain better control over your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.