When consumers ask, “how much is a Tesla car,” they are rarely looking for a single sticker price. In the modern automotive market, particularly within the electric vehicle (EV) sector, the “price” of a vehicle is a multifaceted equation involving MSRP, federal incentives, fluctuating fuel costs, and long-term depreciation rates. For the financially conscious buyer, purchasing a Tesla is less about a simple transaction and more about an investment in a shifting energy ecosystem.

This guide breaks down the financial commitment of Tesla ownership through the lens of personal finance and business economics, moving beyond the surface-level price tag to reveal the true cost of moving toward a sustainable future.

1. Decoding the Initial Investment: MSRP and Model Breakdown

The price of a Tesla is famously volatile, with the company frequently adjusting its manufacturer’s suggested retail price (MSRP) to reflect supply chain efficiencies, lithium costs, and market competition. To understand the entry point, one must look at the four primary models and the specialized Cybertruck.

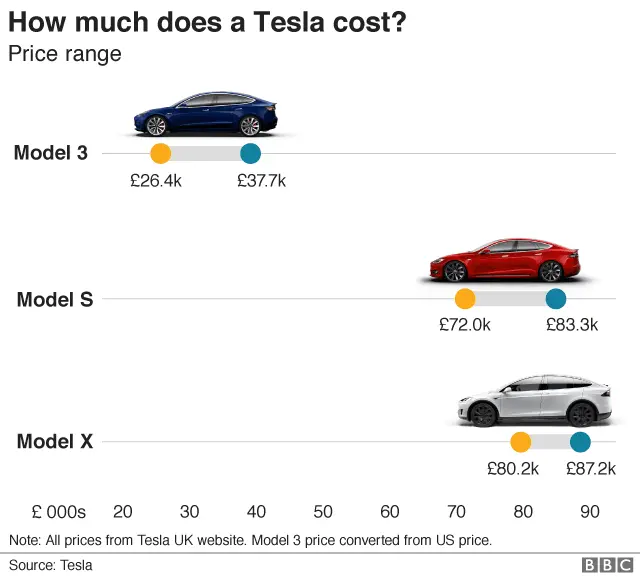

The Entry-Level: Model 3 and Model Y

The Model 3 remains the gateway into the Tesla ecosystem. Currently, the Model 3 Rear-Wheel Drive starts in the high $30,000 range, while the Long Range and Performance variants push into the $45,000 to $55,000 bracket. For those requiring more utility, the Model Y—the world’s best-selling vehicle in recent years—typically starts in the mid-$40,000s. From a financial perspective, these “mass-market” vehicles represent the highest value-to-utility ratio in the lineup, offering the lowest cost-per-mile of range.

The Luxury Tier: Model S and Model X

For the high-net-worth individual or the executive looking for a status symbol that doubles as a performance machine, the Model S and Model X represent a significant jump in capital expenditure. The Model S sedan generally starts around $75,000, with the “Plaid” variant exceeding $90,000. The Model X, with its complex Falcon Wing doors and increased towing capacity, commands a premium, often starting near $80,000. These vehicles are subject to higher luxury taxes in certain jurisdictions and face steeper initial depreciation curves than their more affordable siblings.

The Cybertruck and the Premium of Novelty

The Cybertruck has introduced a new pricing tier. With the initial “Foundation Series” models priced well over $100,000, it currently sits at the top of the pyramid. For a business owner, the Cybertruck may offer specific tax advantages under Section 179 of the IRS code due to its Gross Vehicle Weight Rating (GVWR), potentially allowing for significant first-year write-offs that lower the “real” cost of the vehicle.

2. The Role of Government Incentives and Tax Credits

In the “Money” category of automotive purchasing, the most powerful tool for the consumer is the federal and state incentive programs. These are not merely discounts; they are strategic financial instruments designed to lower the barrier to entry for EV adoption.

The Federal Clean Vehicle Credit

Under the Inflation Reduction Act, many Tesla models qualify for a federal tax credit of up to $7,500. The most significant financial shift in recent years is the ability to apply this credit at the “point of sale,” effectively treating it as a down payment rather than a credit claimed months later on a tax return. However, this is subject to strict income caps and vehicle price limits (e.g., $55,000 for sedans and $80,000 for SUVs). Navigating these thresholds is a critical step in the financial planning process for any prospective buyer.

State-Level Rebates and Local Perks

Beyond federal assistance, states like California, Colorado, and New York offer additional rebates that can shave another $2,000 to $5,000 off the effective price. Furthermore, many utility companies provide rebates for the installation of Level 2 home charging stations. When these layers of incentives are stacked, the “out-of-door” cost of a Model 3 can often rival that of a mid-tier Toyota Camry or Honda Accord, despite the higher MSRP.

The Hidden Value of HOV Access and Registration

In many metropolitan areas, Teslas are granted access to High Occupancy Vehicle (HOV) lanes regardless of the number of passengers. While difficult to quantify as a direct line item, the “time-is-money” principle applies here. Reducing a commute by 20 minutes a day can equate to hundreds of hours of reclaimed productivity over the life of the car. Additionally, some states offer reduced registration fees or exemptions from emissions testing, providing small but consistent annual savings.

3. Total Cost of Ownership (TCO) vs. Internal Combustion Engines

To truly answer “how much is a Tesla,” one must perform a Total Cost of Ownership (TCO) analysis. This compares the all-in costs of a Tesla against a traditional Internal Combustion Engine (ICE) vehicle over a five-to-ten-year horizon.

Fuel Savings and Energy Efficiency

The most immediate financial relief comes at the “pump.” On average, charging a Tesla at home costs about one-third as much as fueling a comparable gasoline car. For a driver covering 15,000 miles a year, the savings can range from $1,000 to $2,500 annually, depending on local electricity rates and gas prices. Over a six-year ownership period, this provides a $6,000 to $15,000 “dividend” that effectively lowers the purchase price.

Maintenance and the Absence of Mechanical Complexity

Traditional vehicles require oil changes, spark plug replacements, timing belt swaps, and transmission fluid flushes. A Tesla has none of these. The regenerative braking system also significantly extends the life of brake pads and rotors. While Teslas still require tires and cabin air filters, the predictable maintenance schedule is significantly less expensive. Most estimates suggest that Tesla owners spend roughly 50% less on maintenance and repairs over the first 100,000 miles compared to ICE vehicle owners.

The Insurance Premium Variable

One area where the “Money” equation can lean negative is insurance. Because of their high-tech components, aluminum structures, and specialized repair requirements, Teslas can be more expensive to insure. Many owners report premiums 20% to 50% higher than a comparable luxury gas car. However, Tesla has launched its own insurance product in several states, using real-time driving data to offer lower rates to safe drivers, providing a way to mitigate this specific cost.

4. Depreciation, Resale Value, and Market Volatility

For most people, a car is a depreciating asset. However, the rate at which that asset loses value is the difference between a smart financial move and a poor one. Tesla’s secondary market has been a rollercoaster in recent years.

The “Elon Effect” and Price Volatility

Unlike traditional dealerships that use “haggling,” Tesla controls its pricing centrally. When Tesla aggressively cuts the price of new models—as they did throughout 2023—the resale value of used Teslas can plummet overnight. This “price transparency” is a double-edged sword. While it makes buying a new car easier, it introduces a level of market volatility that can lead to “negative equity” for those who financed their cars at the height of the market.

Battery Longevity and Long-Term Value

A major concern for used EV buyers is battery degradation. Tesla’s thermal management systems are industry-leading, with data showing that most batteries retain over 80% of their capacity even after 150,000 miles. This durability supports higher resale values compared to early EVs from other manufacturers. As the used market matures, the “Money” savvy buyer may find that a three-year-old Tesla represents a better value proposition than a new one, as the steepest part of the depreciation curve has already occurred.

Software as an Asset: Full Self-Driving (FSD)

Tesla is unique in that it offers a software package—Full Self-Driving—that can cost upwards of $8,000 to $12,000 or a monthly subscription. From a financial standpoint, adding FSD to a purchase rarely yields a 1-to-1 return on resale value. Most appraisers and trade-in platforms (including Tesla’s own) undervalue the software on the used market. For the best “Money” strategy, many experts recommend the subscription model to maintain liquidity and avoid over-capitalizing the vehicle.

5. Financing Strategies: Making the Numbers Work

The final component of the cost is how you pay for it. With interest rates fluctuating, the method of acquisition can change the total price by thousands of dollars.

Cash vs. Financing in a High-Interest Environment

If you can secure a low-interest rate through a credit union or a Tesla promotional rate (which occasionally drops to 0.99% or 1.99% for specific models), financing may be preferable to paying cash, allowing your capital to remain invested in the market. However, at standard rates of 6% or 7%, the interest paid over a 72-month loan can add nearly $10,000 to the total cost of a Model Y.

Leasing: The Hedge Against Technology Obsolescence

Leasing a Tesla has become increasingly popular as a way to hedge against rapid technological shifts and price volatility. Since you are only paying for the depreciation during the lease term, you are protected if Tesla releases a revolutionary new battery or significantly cuts prices. The downside is that Tesla historically has not allowed lessees to buy out their cars at the end of the term (particularly for Model 3 and Y), meaning you cannot capture any potential equity.

Business Use and Tax Deductions

For entrepreneurs and freelancers, a Tesla can be a powerful tax tool. If used for business more than 50% of the time, the vehicle may qualify for accelerated depreciation. Furthermore, the “cents-per-mile” deduction offered by the IRS often exceeds the actual cost of electricity, allowing the business to effectively profit from the vehicle’s efficiency on paper.

Conclusion: The Final Calculation

How much is a Tesla car? The answer is a moving target. While the sticker price might say $45,000, the “Money” perspective reveals a more nuanced story. After factoring in a $7,500 tax credit, $10,000 in fuel and maintenance savings over five years, and the potential for high resale value, the effective cost of a Tesla often places it in the same financial category as vehicles with a much lower MSRP.

Successful Tesla ownership requires looking past the monthly payment and viewing the vehicle as a component of a broader financial strategy—one that trades higher upfront capital for lower long-term operational expenses. For those who can navigate the incentives and manage the insurance costs, a Tesla is not just a technological marvel; it is a calculated financial decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.