Tax planning is often perceived as a seasonal chore, something to be addressed in the frantic weeks leading up to April. However, for those focused on long-term wealth accumulation and financial stability, lowering taxable income is a year-round strategy. Reducing your taxable income is not about tax evasion; rather, it is about tax optimization—using the legal frameworks provided by the tax code to ensure you keep more of what you earn.

By understanding how the Internal Revenue Service (IRS) defines taxable income versus gross income, individuals can implement specific maneuvers to reduce their tax bracket, increase their eligibility for credits, and ultimately bolster their net worth. This guide explores the most effective, legal methods for lowering your taxable income through retirement planning, strategic deductions, investment management, and business optimizations.

Leveraging Retirement Accounts for Immediate Tax Relief

The most accessible and powerful tool for the average taxpayer to lower their taxable income is the use of tax-advantaged retirement accounts. These accounts are designed by the government to encourage long-term saving by offering significant upfront tax breaks.

Employer-Sponsored Plans: 401(k) and 403(b)

For many employees, the 401(k) (for-profit) or 403(b) (non-profit) is the primary vehicle for tax reduction. Contributions made to a traditional version of these plans are “pre-tax,” meaning the money is taken out of your paycheck before federal and state taxes are calculated. If you earn $80,000 a year and contribute $15,000 to your 401(k), the IRS views your taxable income as $65,000. This immediate reduction can often drop a taxpayer into a lower tax bracket, providing compounded savings.

Traditional Individual Retirement Accounts (IRAs)

If you do not have access to an employer plan, or if you want to supplement one, a Traditional IRA allows for tax-deductible contributions up to an annual limit. It is important to note that the deductibility of these contributions may be phased out based on your modified adjusted gross income (MAGI) if you or your spouse are covered by a retirement plan at work. However, when eligible, these contributions provide a “dollar-for-dollar” reduction in your taxable income.

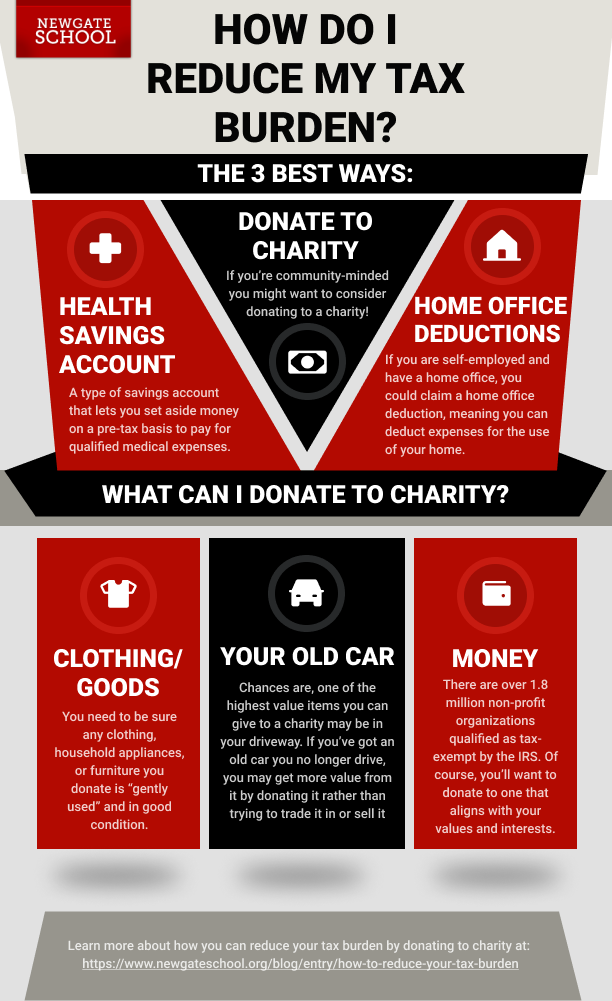

The Power of Health Savings Accounts (HSAs)

While often categorized as a healthcare tool, an HSA is one of the most potent financial instruments available for lowering taxable income. If you have a High Deductible Health Plan (HDHP), contributions to an HSA are 100% tax-deductible (or pre-tax via payroll), the growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Unlike a Flexible Spending Account (FSA), the funds in an HSA roll over year after year, effectively acting as a secondary retirement account that lowers your taxable income today.

Maximizing Itemized Deductions and Personal Credits

The standard deduction is a flat dollar amount that reduces your taxable income, but for many homeowners or high-earners, itemizing deductions can lead to a much lower tax bill. To benefit from itemizing, your total deductible expenses must exceed the standard deduction set for the current tax year.

Strategic Charitable Giving and “Bunching”

Charitable contributions to qualified 501(c)(3) organizations are deductible. For those who find themselves just below the threshold of the standard deduction, a strategy known as “bunching” is highly effective. This involves concentrating two or more years’ worth of planned charitable giving into a single tax year to surpass the standard deduction limit, then taking the standard deduction in the following years. Using a Donor-Advised Fund (DAF) can facilitate this by allowing you to take the tax deduction in the year you contribute to the fund, even if the money is distributed to charities over several subsequent years.

Mortgage Interest and State and Local Taxes (SALT)

For homeowners, the mortgage interest deduction remains a significant way to lower taxable income. Interest paid on up to $750,000 of mortgage debt (for homes purchased after 2017) can be deducted. Additionally, the SALT deduction allows taxpayers to deduct up to $10,000 of combined state and local income taxes (or sales taxes) and property taxes. While the $10,000 cap limits the benefit for those in high-tax states, it remains a cornerstone of itemized deductions.

Student Loan Interest and Educational Deductions

Even if you do not itemize, the IRS allows for an “above-the-line” deduction for student loan interest. You can deduct up to $2,500 of interest paid on qualified student loans. Because this is an adjustment to income, it lowers your Adjusted Gross Income (AGI) directly, which can help you qualify for other income-restricted tax credits and deductions.

Tax-Efficient Investment Strategies

Investing is essential for wealth building, but the way you manage your portfolio can significantly impact your annual tax liability. By being proactive, investors can offset gains and reduce their total taxable exposure.

Tax-Loss Harvesting

Tax-loss harvesting is the practice of selling an investment that is trading at a loss to offset the capital gains realized from selling other profitable investments. If your losses exceed your gains, you can use the excess loss to offset up to $3,000 of ordinary income. Any remaining loss can be carried forward to future tax years. This strategy is particularly effective during market downturns, allowing investors to “find a silver lining” by lowering their taxable income.

Long-Term Capital Gains vs. Short-Term Gains

Lowering your taxable income also involves managing the rate at which you are taxed. Assets held for more than one year qualify for long-term capital gains tax rates, which are significantly lower (0%, 15%, or 20% depending on income) than the ordinary income tax rates applied to short-term gains (assets held for one year or less). By strategically timing the sale of assets, you ensure that the income generated from your investments is taxed as efficiently as possible.

Investing in Municipal Bonds

For investors in high tax brackets, municipal bonds offer a unique advantage. The interest earned on bonds issued by state and local governments is generally exempt from federal income tax. In many cases, if you live in the state where the bond was issued, the interest may also be exempt from state and local taxes. While the interest rates on “munis” may be lower than corporate bonds, the “tax-equivalent yield” often makes them more profitable for high-income earners looking to lower their taxable income.

Tax Benefits for the Self-Employed and Side-Hustlers

The rise of the “gig economy” and remote work has opened up new avenues for tax reduction. If you have side-hustle income or run a full-time business, you have access to a suite of deductions that W-2 employees do not.

The Home Office Deduction

If you use a portion of your home exclusively and regularly for business, you can deduct expenses related to that space. This includes a portion of your mortgage interest, insurance, utilities, and repairs. The IRS offers two methods: the simplified method ($5 per square foot up to 300 square feet) or the actual expense method. This deduction directly reduces the business income that is subject to both income tax and self-employment tax.

Business Expense Write-Offs

Every dollar spent to earn income in a business capacity is generally deductible. This includes marketing costs, software subscriptions, professional development, and travel. For those looking to lower their taxable income at the end of the year, accelerating necessary business purchases (such as upgrading a laptop or prepaying for annual software) can reduce the net profit reported on Schedule C.

Specialized Retirement Plans: Solo 401(k) and SEP IRA

Self-employed individuals can contribute much more to retirement plans than standard employees. A Solo 401(k) allows you to contribute as both the employer and the employee, with total contribution limits significantly higher than a standard IRA. Similarly, a Simplified Employee Pension (SEP) IRA allows you to contribute up to 25% of your net self-employment earnings. These contributions are fully deductible, providing a massive lever for those with high side-income to lower their taxable threshold.

Conclusion

Lowering your taxable income is a multifaceted process that requires a blend of disciplined saving, strategic spending, and proactive investment management. By maximizing contributions to retirement accounts like 401(k)s and HSAs, being intentional with itemized deductions, and utilizing business-related write-offs, you can significantly reduce the amount of your income subject to taxation.

Ultimately, the goal of reducing taxable income is to increase your “effective” income—the money you actually have available to save, invest, and spend. While the tax code is complex, staying informed about these “Money” niche strategies allows you to build a more resilient financial future. As always, because tax laws are subject to change and individual circumstances vary, consulting with a qualified tax professional or financial advisor is recommended to ensure these strategies are implemented correctly within your specific financial ecosystem.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.