In the modern economic landscape, financial literacy is no longer a luxury—it is a survival skill. While there are countless mobile applications designed to track spending with a simple swipe, the most successful wealth-builders often return to a more foundational tool: the budget spreadsheet. A custom-built spreadsheet offers a level of granularity, privacy, and control that automated apps simply cannot match. It forces a tactile engagement with your numbers, transforming abstract income and expenses into a clear roadmap for your financial future.

Creating a budget spreadsheet is more than an exercise in data entry; it is a strategic act of self-governance. By the end of this guide, you will understand how to construct a financial engine that not only tracks where your money goes but directs it toward your most ambitious life goals.

The Foundation of Financial Literacy: Why a Spreadsheet is Your Best Asset

Before diving into rows and columns, it is essential to understand the “why” behind the tool. A budget is not a restriction on your freedom; it is a plan for your dreams. A spreadsheet serves as the central nervous system of your personal finance strategy.

Moving Beyond Mental Math

Many individuals fall into the trap of “mental budgeting,” where they keep a rough estimate of their bank balance and upcoming bills in their heads. This approach is prone to cognitive bias and often leads to “lifestyle creep,” where small, unnoticed expenses gradually erode savings. A spreadsheet provides an objective, cold-hard-look at reality. It eliminates the guesswork and replaces anxiety with data-driven confidence.

Tracking vs. Budgeting: Understanding the Difference

A common misconception is that recording past expenses is the same as budgeting. Tracking is reactive; it tells you where your money went. Budgeting is proactive; it tells your money where to go. An effective spreadsheet combines both. It allows you to set targets at the beginning of the month and then reconcile those targets with actual spending as the weeks progress. This feedback loop is the secret to moving from a paycheck-to-paycheck cycle to a state of surplus.

Step-by-Step: Designing the Architecture of Your Financial Map

To build a spreadsheet that works, you must create a structure that is both comprehensive and easy to maintain. A cluttered or overly complex sheet is a sheet you will eventually stop using. The goal is to create a “Dashboard of Truth” that you can update in less than ten minutes a week.

Categorizing Your Income Streams

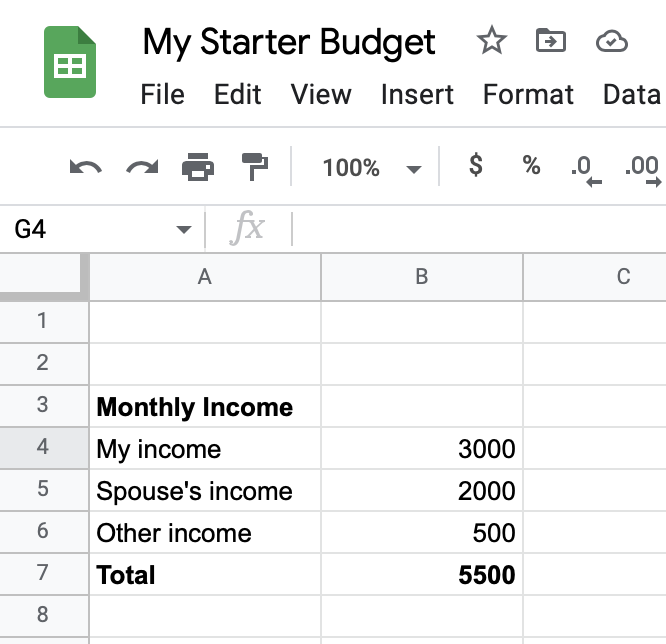

The top of your spreadsheet should always represent your “Inflow.” For many, this is a single line item: a monthly salary. However, in an era of side hustles and passive income, it is vital to list every source of revenue.

- Primary Income: Your net (after-tax) take-home pay.

- Secondary Income: Freelance work, dividends, rental income, or digital product sales.

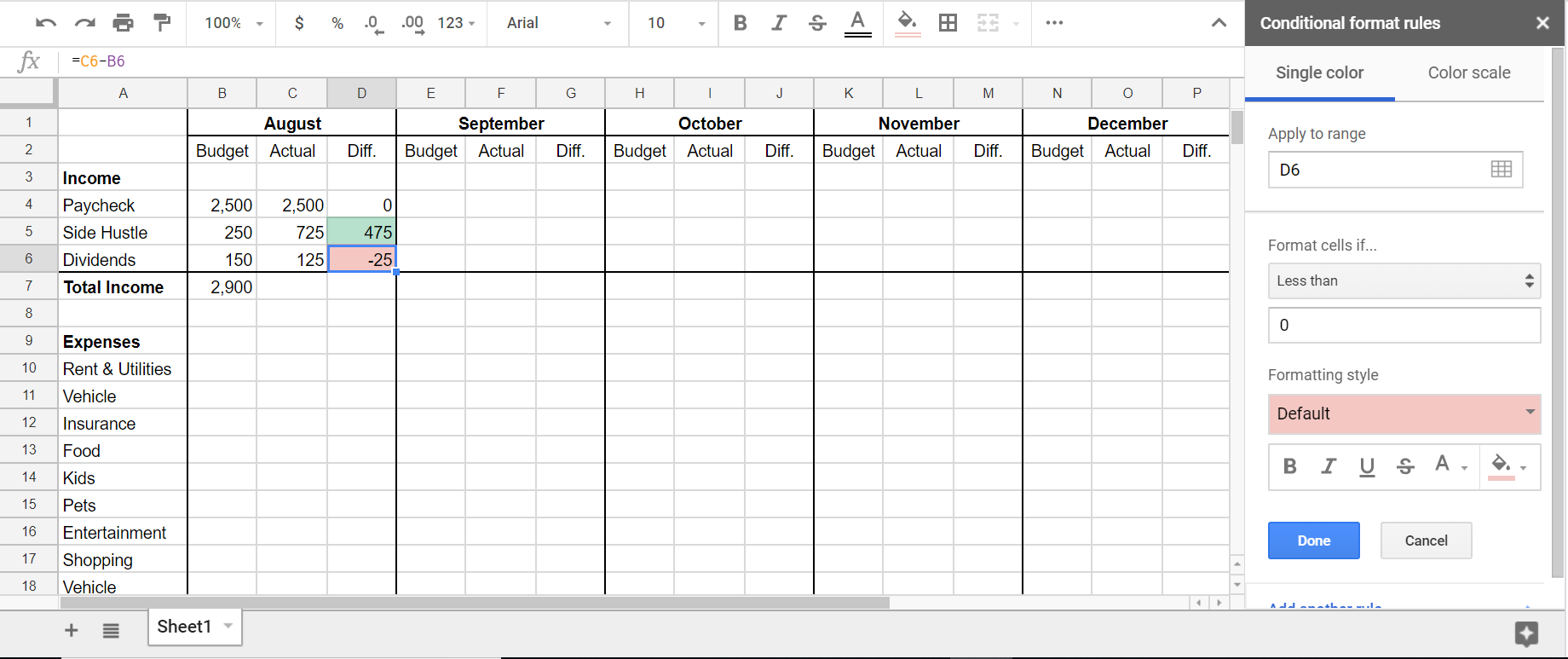

- Expected vs. Actual: Create columns for what you expect to earn and what actually hits your account. This is particularly helpful for those with variable income.

Defining Fixed vs. Variable Expenses

This is the core of your spreadsheet. To maintain clarity, divide your outflows into two distinct sections:

- Fixed Expenses: These are the non-negotiables. Rent/mortgage, insurance premiums, utilities, and subscription services. These costs rarely change month-to-month and are the easiest to plan for.

- Variable Expenses: These are the “living” costs—groceries, dining out, fuel, and entertainment. This is where most “budget leakage” occurs. By isolating these, you can identify exactly where you need to exercise more discipline.

Factoring in “Sinking Funds” and Irregular Costs

One of the primary reasons budgets fail is the “surprise” expense—the annual car registration, the holiday season, or a semi-annual insurance payment. A professional-grade budget spreadsheet includes a section for “Sinking Funds.” These are categories where you save a small amount each month to cover a large future expense. By treating a $1,200 annual expense as a $100 monthly “bill” paid to yourself, you eliminate financial shocks and maintain a steady trajectory.

Choosing Your Budgeting Methodology

Your spreadsheet is a tool, but your methodology is the engine. There is no one-size-fits-all approach to money management. Your spreadsheet should be tailored to the specific philosophy that resonates with your personality and goals.

The 50/30/20 Rule: Simplicity for Beginners

For those just starting their financial journey, the 50/30/20 rule is an excellent framework to build into a spreadsheet.

- 50% to Needs: Housing, groceries, and essential utilities.

- 30% to Wants: Dining, hobbies, and travel.

- 20% to Savings and Debt Repayment: Building an emergency fund or investing for retirement.

In your spreadsheet, you can use simple formulas to calculate these percentages automatically, giving you an immediate “pass/fail” grade on your spending habits each month.

Zero-Based Budgeting: Giving Every Dollar a Job

Favored by strict wealth managers, Zero-Based Budgeting requires that your Income minus your Expenses (including savings and investments) equals exactly zero. If you have $50 left over at the end of your calculations, you haven’t finished budgeting; you must assign that $50 to a specific category, such as an extra payment on a loan or a contribution to a brokerage account. This method ensures that no money is “lost” to mindless spending.

The Pay-Yourself-First Strategy

This methodology prioritizes long-term wealth over immediate consumption. In this spreadsheet layout, the “Savings and Investments” section is placed immediately below “Income.” Before you list your rent or groceries, you decide how much you are investing. This flips the traditional script of “saving what is left after spending” to “spending what is left after saving.”

Advanced Financial Insights: Leveraging Data for Long-Term Growth

Once you have mastered the basics of tracking and planning, your budget spreadsheet can evolve into a powerful analytical tool. This is where personal finance transitions into personal wealth management.

Visualizing Trends with Charts and Graphs

Numerical data is essential, but visual data is influential. Most spreadsheet software allows you to transform your monthly totals into pie charts or line graphs. Seeing a visual representation of your “Housing” cost taking up 45% of your income is often the wake-up call needed to consider downsizing or refinancing. Tracking your “Net Worth” (Assets minus Liabilities) over a 12-month line graph provides the motivation to keep going when the daily grind feels repetitive.

Integrating Debt Repayment and Investment Tracking

An elite budget spreadsheet doesn’t just stop at cash flow; it looks at the big picture.

- The Debt Snowball/Avalanche: Create a dedicated tab to list your debts, interest rates, and balances. Use your budget’s “surplus” to project how quickly you can become debt-free.

- Investment Allocation: Track your contributions to 401(k)s, IRAs, or brokerage accounts. Watching your “Money Working for You” is the ultimate psychological reward for sticking to a budget.

Monthly Audits: How to Iterate for Success

The final piece of the puzzle is the “Monthly Review.” At the end of each month, sit down with your spreadsheet and ask: Where did I overspend? Why? Were my goals realistic? A budget is a living document. It should change as your life changes. If you consistently overspend on groceries but underspend on entertainment, adjust the numbers for the following month. This iterative process turns the spreadsheet from a static record into a dynamic instrument of growth.

Conclusion: Empowerment Through Organization

Building a budget spreadsheet is an act of taking ownership of your life. It removes the veil of mystery from your finances and replaces it with a clear, actionable strategy. Whether you are aiming to climb out of debt, save for a first home, or achieve early retirement, the path begins with a single cell in a spreadsheet.

By categorizing your income, defining your expenses, choosing a methodology that fits your lifestyle, and utilizing data to look ahead, you transform from a passive observer of your bank account into the CEO of your own household. Financial freedom is rarely the result of luck; it is the result of a well-executed plan. Start building your spreadsheet today, and give yourself the gift of a disciplined, prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.