The landscape of personal finance has undergone a seismic shift over the last decade. The days of writing paper checks or searching for a surcharge-free ATM to pay a friend back for dinner are rapidly fading into obsolescence. In their place, a new era of digital liquidity has emerged, headlined by financial technology (fintech) giants that prioritize speed, accessibility, and user experience. At the forefront of this revolution is Cash App.

Owned by Block, Inc., Cash App has evolved from a simple peer-to-peer (P2P) payment tool into a multifaceted financial ecosystem. For the modern consumer, understanding how to navigate this platform is no longer just a matter of convenience; it is a core competency in digital money management. This guide explores the intricacies of sending money on Cash App, framed through the lens of strategic personal finance and digital security.

The Evolution of Peer-to-Peer Finance

To understand the utility of Cash App, one must first recognize the broader shift in how we perceive and move capital. Peer-to-peer payment systems have democratized banking, allowing individuals to bypass the traditional hurdles of wire transfers and clearinghouses.

Why Cash App is a Pillar of Modern Personal Finance

Cash App’s dominance in the market is not accidental. It serves a specific niche by offering a “frictionless” financial experience. For many, it functions as a secondary bank account, providing a landing spot for side hustle income, a tool for splitting household expenses, and even a gateway into equity markets. The platform’s ability to move money instantly—often referred to as “real-time payments”—has changed the velocity of money in our daily lives, making it an essential tool for those managing tight budgets or fast-moving business ventures.

Bridging the Gap Between Traditional Banking and Digital Wallets

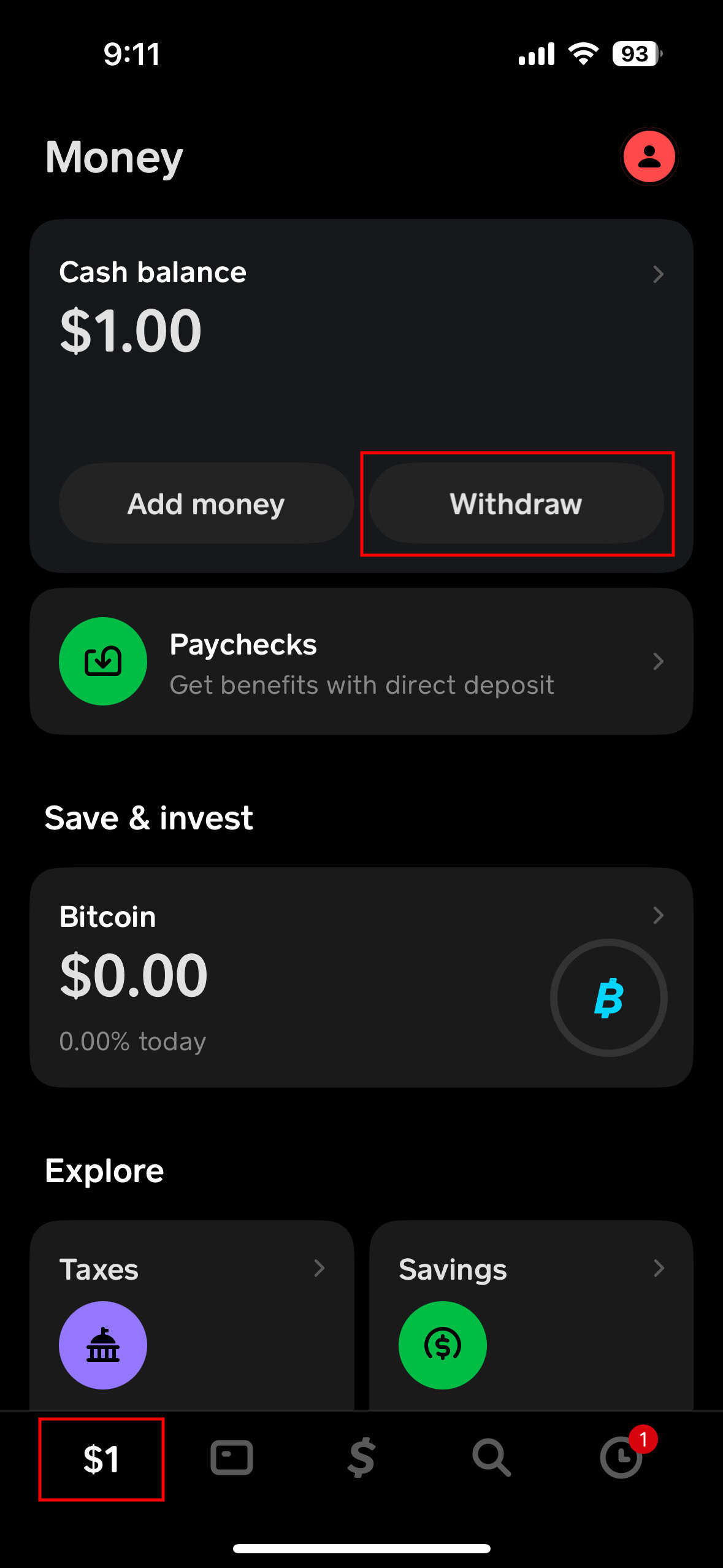

While traditional banks are catching up with services like Zelle, Cash App maintains a unique position by operating as a hybrid digital wallet. It bridges the gap by allowing users to maintain a “Cash Balance” independent of their traditional savings accounts while still providing the infrastructure to “Cash Out” to a legacy bank when necessary. This flexibility is the cornerstone of modern money management, offering a level of autonomy that traditional checking accounts often lack.

Navigating the Cash App Ecosystem

Before sending your first dollar, it is crucial to understand the infrastructure of your account. How you set up your profile and link your funding sources will determine your transaction limits, your fees, and your overall financial security.

Setting Up Your Financial Profile

Every Cash App user is identified by a unique identifier known as a $Cashtag. From a financial management perspective, your $Cashtag is your digital address for capital. When setting up your profile, professionality and clarity are key. Ensure your account is verified with your legal name and contact information; this is not just a platform requirement but a regulatory necessity under “Know Your Customer” (KYC) laws. Verification increases your sending and receiving limits, which is vital for users intending to use the platform for more than just nominal transactions.

Linking External Accounts: Debit Cards vs. Credit Cards

One of the most important financial decisions you make within the app is choosing your funding source. Cash App allows you to link debit cards, credit cards, and bank accounts.

- Debit Cards: These are the standard for P2P transfers. Sending money via a linked debit card or your Cash Balance is typically free of charge.

- Credit Cards: Cash App permits the use of credit cards for sending money, but it comes with a 3% transaction fee. From a personal finance standpoint, this is rarely advisable unless in an emergency, as it immediately erodes the value of the transfer and can lead to high-interest debt if not paid off instantly.

- Bank Accounts (ACH): While slower for “Cashing Out,” linking a bank account via the routing and account number is the most stable way to move large sums of money between your personal wealth reserves and your liquid digital wallet.

The Mechanics of Sending Money Safely

The actual process of sending money is deceptively simple. However, within that simplicity lies the need for extreme diligence. Because P2P payments are often instantaneous and irreversible, treating every “Send” button as a final financial decision is paramount.

Step-by-Step Guide to Executing a Transaction

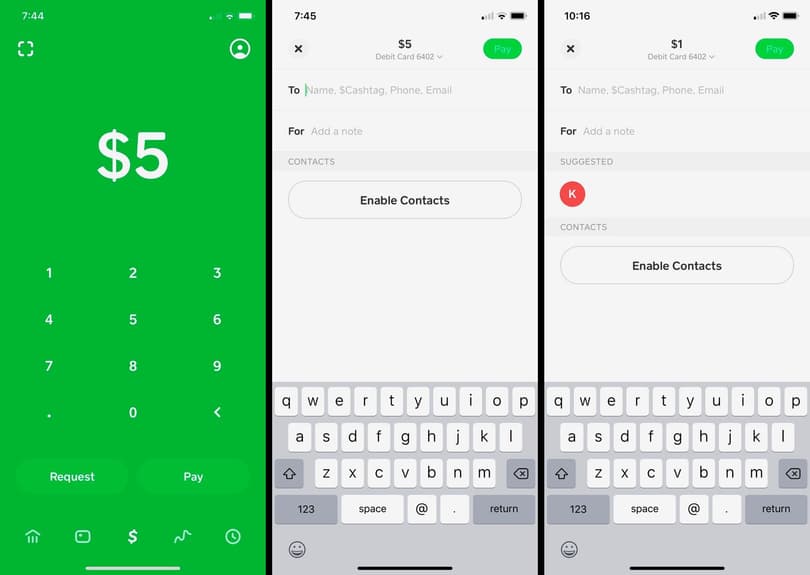

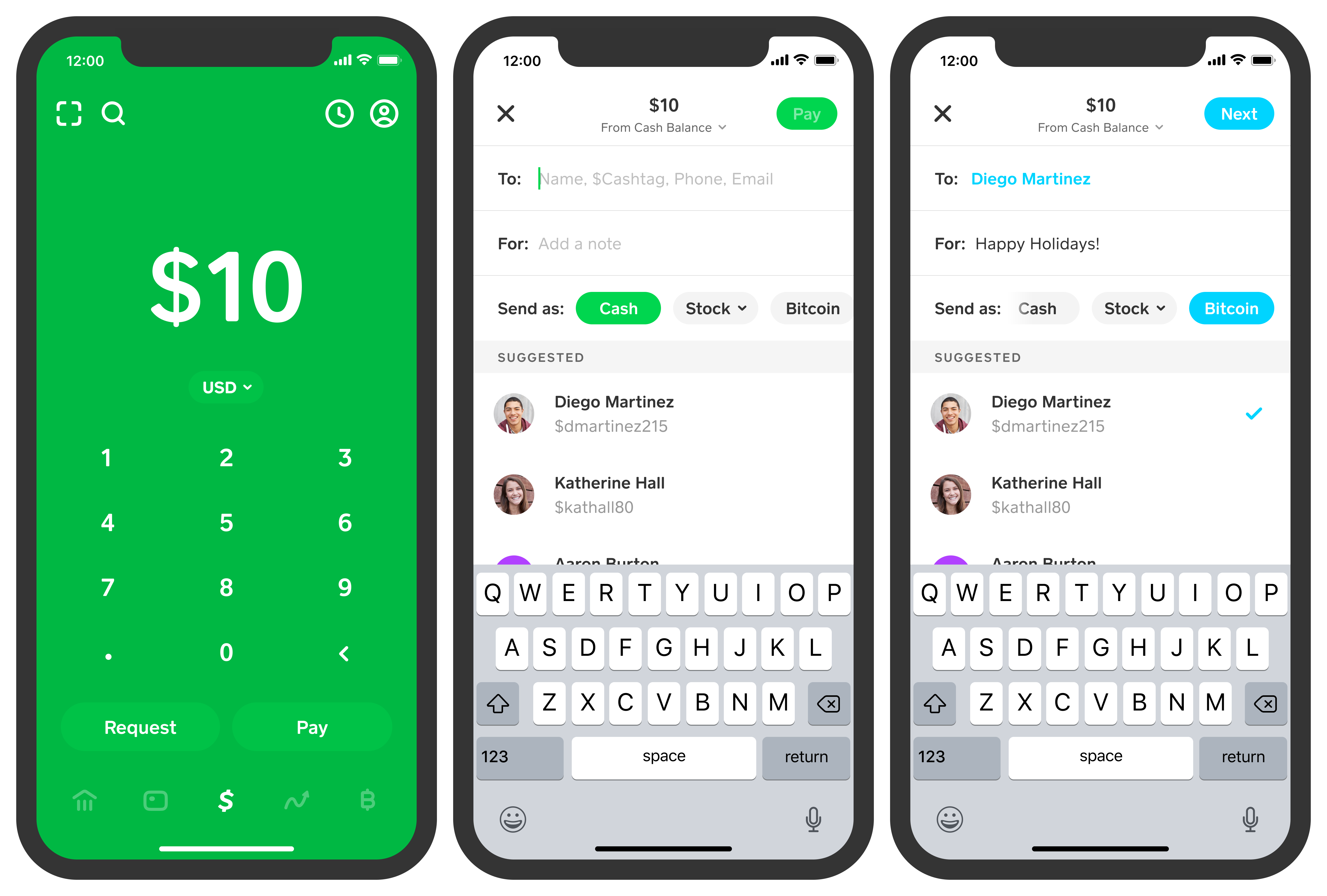

To send money, you simply open the app and enter the desired amount on the main keypad. After tapping “Pay,” you enter the recipient’s $Cashtag, email, or phone number.

- Double-Check the $Cashtag: Unlike a bank transfer where names are verified by the institution, a typo in a $Cashtag can result in money being sent to a complete stranger.

- Add a Note: For tax and budgeting purposes, always include a memo (e.g., “August Rent” or “Dinner Reimbursement”). This creates a digital paper trail that is invaluable during tax season or if a dispute arises.

- Confirm the Source: Ensure the app is pulling from your “Cash Balance” or “Debit Card” to avoid the aforementioned 3% credit card fee.

Understanding Limits and Verification for Larger Transfers

New, unverified accounts often face strict limits—typically $250 per week for sending and $1,000 per month for receiving. To integrate Cash App into a more robust financial strategy, you must complete the verification process by providing your date of birth, the last four digits of your Social Security Number, and potentially a photo ID. Once verified, these limits are significantly increased, allowing for the payment of high-value items like rent, contractor fees, or large-scale reimbursements.

Security Protocols and Financial Best Practices

In the digital age, security is the most critical component of money management. Cash App’s ease of use makes it an attractive target for bad actors, but with the right financial hygiene, these risks can be mitigated.

Protecting Your Capital from Scams

The most important rule of P2P finance is: Only send money to people you know and trust.

Cash App payments are not protected by the same “buyer protection” policies found in traditional credit card transactions or platforms like PayPal (Goods and Services). Common scams include “accidental” deposits where a stranger asks you to send money back, or “payment claims” where scammers pose as Cash App support. To protect your capital, enable the “Security Lock” feature in the app settings, which requires your PIN or biometric data (Touch ID/Face ID) for every transaction. This ensures that even if your phone is compromised, your funds remain secure.

Managing Your Transaction History for Better Budgeting

For those committed to financial literacy, Cash App provides a “Statement” feature. You can download your transaction history as a CSV file, which can be imported into budgeting software like YNAB (You Need A Budget) or Mint. By categorizing your Cash App expenditures, you gain a clearer picture of your “invisible” spending—those small $10 to $20 transfers that often go unaccounted for in traditional bank statements but can significantly impact your monthly net worth.

Integrating Cash App into Your Wealth Management Strategy

Beyond simple transfers, Cash App offers features that allow users to grow their wealth and manage daily expenses more effectively. Viewing the app as a comprehensive financial tool rather than just a payment app can unlock significant value.

Leveraging the Cash Card for Daily Expenses

The Cash Card is a customizable Visa debit card linked directly to your Cash App balance. For many, this card serves as a “disposable income” account. By transferring a set “fun money” budget to your Cash App balance each month and only using the Cash Card for those expenses, you create a natural barrier against overspending. Furthermore, the “Boosts” feature offers instant discounts at specific retailers, which is essentially a form of immediate cash-back that can be reinvested into your savings.

Exploring Micro-Investing: Bitcoin and Stocks

Cash App has democratized the world of investing by allowing for fractional shares and Bitcoin purchases with as little as $1.

- Equities: Users can buy portions of high-priced stocks (like Amazon or Berkshire Hathaway) without needing thousands of dollars. This is an excellent way for beginners to practice “Dollar Cost Averaging” (DCA), a strategy where you invest a fixed amount regularly regardless of market fluctuations.

- Bitcoin: As digital assets become a more common part of a diversified portfolio, Cash App provides one of the most user-friendly on-ramps for purchasing and even withdrawing Bitcoin to personal cold storage.

By integrating these features, Cash App moves from being a simple utility to a central hub for capital movement, expenditure tracking, and wealth accumulation. When used with discipline and a focus on security, it represents the pinnacle of modern, mobile-first financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.