In the dynamic world of personal finance, the interest rate on your credit card can be one of the most significant factors determining the true cost of borrowing. For many consumers, the quest for the lowest possible interest rate is a priority, and for good reason. A lower Annual Percentage Rate (APR) translates directly into less money spent on interest charges, freeing up funds for savings, investments, or other financial goals. But what exactly constitutes the “lowest” interest rate, and how can one navigate the myriad of options to secure it? This comprehensive guide delves into the nuances of credit card interest rates, offering insights into finding, qualifying for, and utilizing the most advantageous terms available in the market.

Understanding Credit Card Interest Rates

Before embarking on the search for the lowest rates, it’s crucial to have a clear understanding of what credit card interest rates entail and how they function. This foundational knowledge empowers consumers to make informed decisions and decipher the often-complex language used by financial institutions.

The Anatomy of an APR (Annual Percentage Rate)

The APR is the most critical figure to understand when evaluating credit card interest. It represents the annual cost of borrowing money, expressed as a percentage. While it’s an annual rate, interest is typically calculated and applied daily or monthly based on your average daily balance. A common misconception is that the APR is a fixed, singular number for every cardholder. In reality, credit card issuers often present a range of APRs (e.g., 15.99% to 25.99%), with the specific rate offered depending on the applicant’s creditworthiness. Factors like credit score, debt-to-income ratio, and payment history heavily influence where an individual falls within this spectrum.

Variable vs. Fixed Rates

Credit card interest rates predominantly fall into two categories: variable or fixed.

- Variable APRs are the most common type. They are tied to a publicly available index, typically the U.S. Prime Rate. When the Prime Rate changes, your credit card’s APR will adjust accordingly, either increasing or decreasing. This means your interest rate can fluctuate over time, making it less predictable. Most major credit cards carry a variable APR.

- Fixed APRs, while less common, offer stability. With a fixed APR, your interest rate remains constant unless the card issuer provides a written notice of a change, which they must do at least 45 days in advance. Even then, certain events, such as a late payment, can trigger a penalty APR, overriding the fixed rate. For consumers who prioritize predictability, fixed rates might seem appealing, but they are increasingly rare in general-purpose credit cards.

Introductory vs. Standard APRs

Many credit cards lure new customers with attractive introductory APRs, often referred to as 0% APR offers.

- Introductory APRs are promotional rates that last for a specified period, usually between 6 and 21 months. During this time, you pay no interest on new purchases, balance transfers, or sometimes both. These offers can be incredibly valuable for financing large purchases or consolidating high-interest debt without incurring immediate interest charges.

- Once the introductory period expires, the rate reverts to the standard APR. This is the ongoing interest rate that will apply to any remaining balance or new transactions. It’s crucial to be aware of what the standard APR will be after the promotional period, as a low introductory rate can be offset by a high standard rate, especially if you anticipate carrying a balance.

Navigating the Landscape of Low-Interest Credit Cards

The term “lowest interest rate” isn’t a single, universal figure; rather, it’s a moving target influenced by market conditions, your financial profile, and the specific type of credit card you’re seeking. However, certain categories of credit cards are inherently designed to offer more favorable interest terms.

0% Introductory APR Credit Cards

For those looking for the absolute lowest interest rate for a defined period, 0% introductory APR credit cards are the undisputed champions. These cards offer a temporary reprieve from interest payments, typically for 6 to 21 months on purchases, balance transfers, or both. This allows consumers to make significant purchases or pay down existing debt without accruing interest during the promotional window.

- Best Use Cases: Ideal for financing large expenses (e.g., home appliances, medical bills), or executing a balance transfer to consolidate high-interest debt from other cards.

- Considerations: It’s imperative to have a plan to pay off the balance before the introductory period ends to avoid paying the (potentially high) standard APR. Look for cards with no balance transfer fees or low ones, as these can eat into your savings.

Low Ongoing APR Credit Cards

Beyond the introductory offers, some credit cards are specifically marketed for their consistently low standard APRs. These cards might not feature a 0% introductory period, or if they do, it might be shorter. Their primary appeal lies in providing a competitive interest rate for the long term, making them suitable for individuals who occasionally carry a balance and want to minimize ongoing interest costs.

- Who Benefits: Consumers with excellent credit who anticipate carrying a balance from month to month, or those who simply want a safety net against high interest.

- Where to Find Them: Often issued by credit unions, smaller regional banks, or specific online lenders that prioritize low rates over extensive rewards programs. Discover, PenFed, and local credit unions are often good places to start looking.

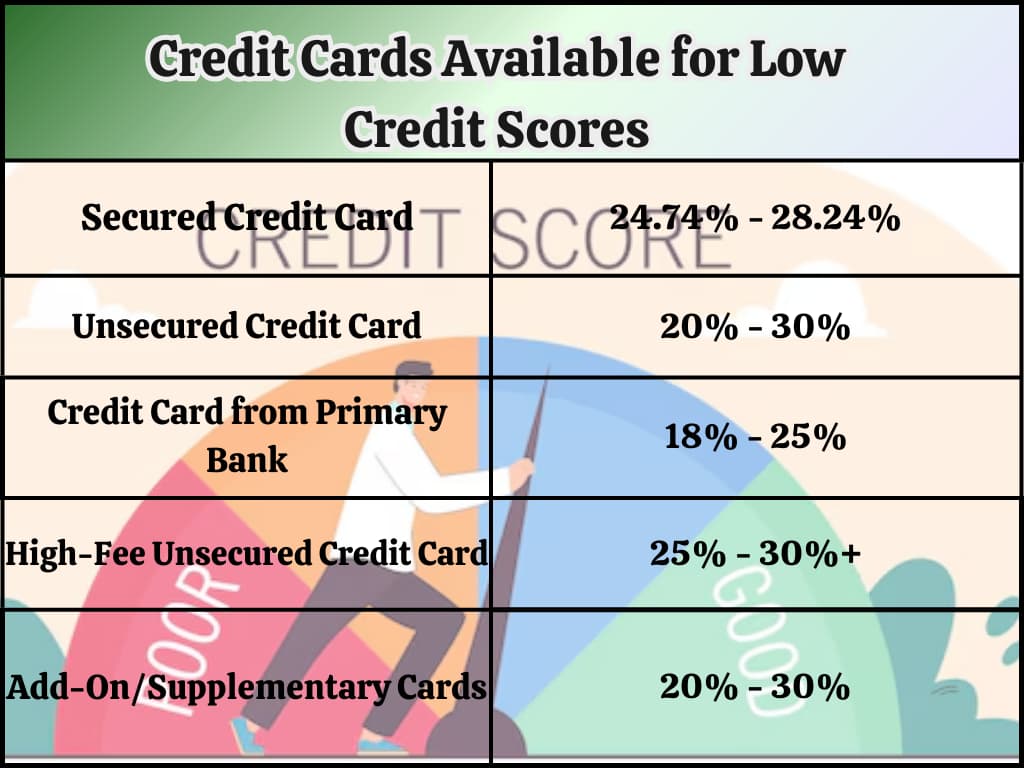

Secured Credit Cards as a Path to Lower Rates

For individuals with limited or poor credit history, qualifying for top-tier low-interest cards can be challenging. Secured credit cards offer an alternative pathway. While not always boasting the lowest rates upfront, they can be instrumental in building or rebuilding credit, which is the ultimate key to unlocking better rates in the future.

- How They Work: You provide a cash deposit, which typically becomes your credit limit. This deposit secures the card and reduces the risk for the issuer, making them more willing to approve applicants with less-than-perfect credit.

- Credit Building: Regular, on-time payments with a secured card are reported to credit bureaus, positively impacting your credit score. Over time, as your score improves, you can graduate to an unsecured card with significantly lower interest rates and more favorable terms. Some secured cards even offer competitive APRs for their category, particularly those from credit unions.

Strategies for Securing the Best Interest Rates

The “lowest interest rate” is often not simply found; it’s earned. Your financial behavior and the way you approach credit applications play a crucial role in the rates you’re offered.

The Critical Role of Your Credit Score

Your credit score is arguably the single most influential factor in determining the interest rate you’ll be offered. Lenders use this three-digit number to assess your creditworthiness and the risk associated with lending to you.

- Excellent Credit (740-850 FICO): Individuals in this range consistently qualify for the lowest available APRs, including the best 0% introductory offers and low ongoing rates.

- Good Credit (670-739 FICO): Still qualifies for very competitive rates, though perhaps not the absolute lowest.

- Fair Credit (580-669 FICO): Rates will be higher, and 0% offers might be limited or nonexistent.

- Poor Credit (300-579 FICO): Expect high interest rates. Secured cards or credit builder loans are usually the best starting points for improvement.

To improve your score, focus on paying bills on time, keeping credit utilization low (below 30%), and avoiding opening too many new accounts in a short period.

Debt-to-Income Ratio and Its Impact

While not as directly impactful on APR as your credit score, your debt-to-income (DTI) ratio is another metric lenders consider. It compares your total monthly debt payments to your gross monthly income. A high DTI can signal to lenders that you’re overextended, potentially making them less likely to offer you their most favorable rates, even if your credit score is decent. A DTI below 36% is generally considered good, with lower being better.

Applying for Credit Strategically

Don’t apply for every low-interest card you see. Each application results in a “hard inquiry” on your credit report, which can slightly (and temporarily) lower your credit score.

- Research Thoroughly: Use online comparison tools to identify cards for which you’re likely to qualify based on your credit profile.

- Pre-qualification: Many issuers offer pre-qualification tools that allow you to see if you’re likely to be approved without a hard inquiry. This is a smart first step.

- One Application at a Time: If you’re building credit, focus on getting approved for one card and managing it responsibly before applying for another.

Beyond APR: A Holistic View of Credit Card Value

While the lowest interest rate is a prime objective, it’s essential to consider the entire package a credit card offers. A low APR can sometimes be offset by other fees or a lack of beneficial features.

Fees That Can Offset Low Interest

- Annual Fees: Some premium cards or cards with extensive rewards might carry an annual fee. If your goal is purely to minimize interest, an annual fee (especially one that isn’t waived for the first year) can negate some of the savings from a low APR.

- Balance Transfer Fees: While 0% balance transfer APRs are appealing, balance transfer fees (typically 3-5% of the transferred amount) are common. Factor this cost into your calculation when moving debt.

- Cash Advance Fees: Avoid cash advances as they often come with high fees and immediately accrue interest at a separate, often higher, cash advance APR.

- Late Payment Fees & Penalty APRs: These can quickly erode any benefits from a low standard APR. Always pay on time.

Rewards Programs vs. Interest Savings

Many credit cards come with rewards programs (cash back, points, miles). While these can offer tangible value, they are often paired with higher standard APRs.

- Prioritize: If you consistently pay your balance in full each month, a rewards card might offer more value than a slightly lower APR card. However, if you often carry a balance, the interest saved from a low APR card will almost always outweigh the value of rewards.

- The Math: Calculate how much interest you typically pay in a year versus the estimated value of your rewards. This will clearly show which card offers better overall financial benefit for your spending habits.

The Importance of Cardholder Benefits

Beyond rates and rewards, consider other benefits that might enhance the card’s value:

- Fraud Protection: Standard across most cards, but still a vital benefit.

- Purchase Protection & Extended Warranty: Can save you money on damaged or failing products.

- Travel Insurance & Concierge Services: Relevant for frequent travelers, often found on premium cards which might have higher APRs.

- Credit Score Tracking: Many cards offer free access to your FICO score, which is a valuable tool for financial management.

Minimizing Interest Payments and Smart Credit Card Use

Finding a low-interest credit card is only half the battle; the other half is using it wisely to keep interest charges to a minimum. Smart financial habits are key to leveraging the benefits of a low APR.

Always Pay More Than the Minimum

The minimum payment is designed to keep you in debt for as long as possible, maximizing interest accrual. Paying only the minimum can extend your repayment period by years and significantly increase the total cost of your purchases. Always aim to pay as much as you can afford above the minimum, or ideally, the full statement balance. Even an extra $20 or $50 a month can make a substantial difference in the long run.

Automating Payments to Avoid Missed Deadlines

One of the quickest ways to lose the benefit of a low APR is to incur a late payment. Not only can late fees be charged, but your low standard APR might be replaced by a significantly higher penalty APR. Set up automatic payments for at least the minimum amount, or for your full statement balance, to ensure you never miss a due date. Complement this with calendar reminders for larger payments if you don’t auto-pay the full amount.

Consolidating High-Interest Debt

For those struggling with multiple credit cards carrying high interest rates, a 0% introductory APR balance transfer card can be a game-changer. By moving all your high-interest balances onto a single card with a promotional 0% APR, you consolidate payments and gain a crucial interest-free period to pay down the principal. This strategy demands discipline; you must have a clear plan to pay off the transferred balance before the intro period expires to avoid the standard APR.

Regular Review of Your Credit Card Terms

Interest rates and card benefits aren’t static. Issuers can change terms, particularly for variable APRs. Make it a habit to regularly review your credit card statements and the terms and conditions. If your card’s standard APR has increased significantly, or if a better offer is available elsewhere, it might be time to consider a balance transfer or switching to a new card. Your financial health is a continuous journey, requiring ongoing vigilance and adaptation.

In conclusion, the lowest interest rate for a credit card isn’t a single, fixed number waiting to be discovered; it’s a dynamic range influenced by market rates, your individual credit profile, and the specific terms of different card products. For short-term needs, a 0% introductory APR card offers the absolute lowest rate. For long-term borrowing, an ongoing low APR card, often from a credit union, is ideal. Ultimately, securing and maintaining the best interest rate is a testament to strong financial habits, a good credit score, and a proactive approach to managing your personal finance. By understanding how interest works and strategically choosing and using your credit cards, you can significantly reduce your borrowing costs and build a healthier financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.