Navigating the landscape of business finance requires more than just a grasp of revenue and profit margins. For any entrepreneur or small business owner, the complexities of payroll taxes represent a significant portion of operational overhead and legal responsibility. Among these obligations, the Federal Unemployment Tax Act (FUTA) stands as a foundational pillar of the American labor and financial system. While it may appear as just another acronym on a tax form, understanding FUTA is essential for maintaining compliance, optimizing cash flow, and managing the total cost of human capital.

Defining FUTA: The Mechanics of the Federal Unemployment Tax Act

At its core, the Federal Unemployment Tax Act is a piece of legislation that authorizes the federal government to collect taxes from employers to fund state unemployment insurance agencies. Unlike many other payroll taxes that are split between the employer and the employee, FUTA is a unique burden placed solely on the business.

What is the FUTA Tax?

FUTA is a federal payroll tax that provides the funds necessary to oversee unemployment insurance programs at both the state and federal levels. When a worker loses their job through no fault of their own, they are often eligible for unemployment benefits. These benefits are not paid out of thin air; they are funded by the taxes collected via FUTA and its state-level counterpart, SUTA (State Unemployment Tax Act).

The revenue generated by FUTA is primarily used to cover the administrative costs of the unemployment insurance program in all 50 states. Additionally, it funds the federal share of extended unemployment benefits during periods of high economic distress or recession.

Who is Responsible for Paying FUTA?

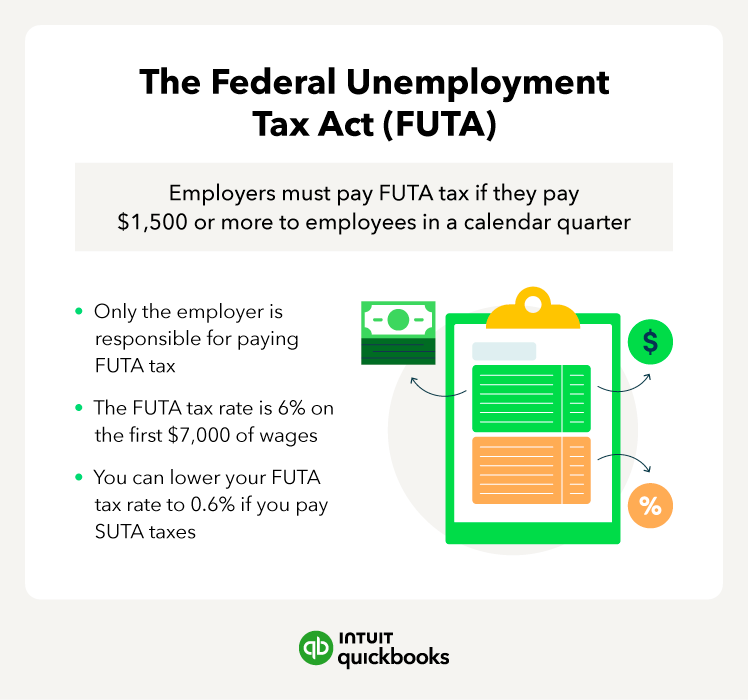

One of the most common misconceptions among new business owners is that FUTA is deducted from an employee’s paycheck. This is incorrect. FUTA is an employer-only tax. As an employer, you cannot withhold this tax from your employees’ wages or recoup the cost from them in any direct manner.

An entity is generally subject to FUTA tax if they meet one of two criteria set by the IRS:

- They paid wages of $1,500 or more to employees in any calendar quarter during the current or preceding year.

- They had at least one employee for at least part of a day in 20 or more different weeks during the current or preceding year. This includes full-time, part-time, and temporary workers.

FUTA vs. SUTA: Understanding the Distinction

To fully grasp FUTA, one must understand its relationship with SUTA. While FUTA is a federal tax, SUTA is the state-level equivalent. Every state has its own unemployment tax system with varying rates and wage bases.

The two systems work in tandem. Most of the actual benefit payments to unemployed workers come from state funds (SUTA), while the federal fund (FUTA) acts as the backbone for administration and a safety net for the states. As we will explore later, the amount you pay in SUTA can significantly impact your federal FUTA liability through a specialized tax credit.

Calculating Your Liability: Rates, Thresholds, and the FUTA Credit

The financial impact of FUTA is determined by a specific percentage and a capped wage base. For businesses with many employees, these small percentages can add up, making it vital to understand the calculation process for accurate budgeting and financial forecasting.

The Wage Base Limit and the 6.0% Rule

The FUTA tax rate is set at 6.0%. However, this rate is not applied to an employee’s total annual salary. Instead, it is applied only to the first $7,000 of wages paid to each employee during the calendar year. This $7,000 threshold is known as the “federal wage base.”

For example, if you have an employee who earns $50,000 a year, you only pay the 6.0% FUTA tax on the first $7,000 they earn. Once they have earned $7,001 in a calendar year, you no longer owe FUTA tax for that specific employee for the remainder of that year. If you have ten employees, you would owe 6.0% on the first $7,000 of each person’s earnings, totaling a maximum liability of $4,200 (10 employees x $7,000 x 0.06) before credits.

The FUTA Tax Credit: How to Lower Your Rate to 0.6%

The headline rate of 6.0% sounds high, but in practice, very few businesses actually pay that amount. The IRS offers a tax credit to employers who pay their state unemployment taxes on time. This credit can be as high as 5.4% of taxable FUTA wages.

When you subtract the 5.4% credit from the 6.0% statutory rate, the “effective” FUTA tax rate becomes 0.6%. Following the previous example of ten employees, the total liability drops from $4,200 to just $420 ($7,000 x 0.006 x 10). To qualify for the full 5.4% credit, your state must not be a “credit reduction state,” and you must have paid all of your state unemployment obligations by the filing deadline of Form 940.

Practical Example of FUTA Calculation

Consider a boutique marketing firm with three employees:

- Employee A: Earns $60,000/year

- Employee B: Earns $45,000/year

- Employee C: Earns $5,000/year (Part-time)

The FUTA-taxable wages for Employee A and B are capped at $7,000 each. For Employee C, the taxable wages are the full $5,000 because they did not reach the $7,000 threshold.

Total taxable wages = $7,000 + $7,000 + $5,000 = $19,000.

Assuming the business qualifies for the full 5.4% credit, the FUTA tax owed would be:

$19,000 x 0.006 = $114.

Filing and Payment Requirements: Navigating Form 940

Compliance is the cornerstone of business finance. Failing to report or pay FUTA taxes correctly can lead to audits, interest, and significant penalties that can drain a company’s cash reserves.

Reporting with IRS Form 940

The primary document used to report FUTA tax is IRS Form 940, the Employer’s Annual Federal Unemployment (FUTA) Tax Return. This form is filed once a year and summarizes the total wages paid, the amount of those wages subject to FUTA, and the adjustments for state unemployment tax credits.

Even though it is an annual form, it requires diligent record-keeping throughout the year. You must track when each employee hits the $7,000 threshold and ensure that your SUTA payments are synchronized with your federal reporting.

Quarterly Deposit Rules

While Form 940 is filed annually, the actual payment of the tax may need to happen more frequently. The IRS requires quarterly deposits if your FUTA tax liability exceeds $500 in a given quarter.

If your liability is $500 or less at the end of a quarter, you don’t need to make a deposit; instead, you carry that amount over to the next quarter. Once your cumulative liability for the year exceeds $500, you must make a deposit by the last day of the month following the end of that quarter. If your total FUTA tax for the entire year is $500 or less, you can simply pay it once a year when you file Form 940.

Deadlines and Penalties for Non-Compliance

The deadline for filing Form 940 is January 31st of the following year. For example, taxes for the 2023 calendar year must be reported by January 31, 2024. If you have made all your deposits on time, you may be granted an extra ten days to file.

Failure to file or pay can result in penalties ranging from 5% to 25% of the unpaid tax amount, depending on how late the payment is. Furthermore, if your state is a “credit reduction state”—meaning the state has borrowed money from the federal government to pay unemployment benefits and hasn’t paid it back—the 5.4% credit might be reduced, effectively increasing your FUTA rate.

The Financial Impact on Small Businesses and Startups

For a large corporation, FUTA is a minor line item. For a startup or a small business operating on thin margins, every dollar counts. Understanding the nuances of FUTA is part of a broader strategy for responsible financial management.

Budgeting for Payroll Taxes

When hiring a new employee, a business owner must look beyond the base salary. Between Social Security (6.2%), Medicare (1.45%), FUTA (0.6%), and SUTA (variable), the “true cost” of an employee is typically 10% to 15% higher than their gross pay. Smart financial planning involves “grossing up” these figures during the hiring process to ensure the business can actually afford the additional headcount.

Exemptions and Special Considerations

Not all payments are subject to FUTA. For instance, payments to independent contractors (1099 workers) do not trigger FUTA liability because they are not technically employees. Additionally, certain fringe benefits, such as employer contributions to health insurance or 401(k) plans, are often excluded from the FUTA wage base. Understanding these exemptions can prevent a business from overpaying their tax obligations.

The Role of FUTA in the Broader Economic Landscape

From a macro-financial perspective, FUTA acts as an automatic stabilizer for the economy. By funding unemployment insurance, it ensures that when people lose their jobs, they still have a basic level of purchasing power. This prevents a complete collapse in consumer spending during downturns, which in turn helps businesses stay afloat. While it feels like a cost to the individual business, it serves as a collective insurance policy for the stability of the marketplace.

Strategic Financial Management: Optimizing Your Tax Obligations

To manage FUTA and other payroll taxes effectively, business owners should move away from manual calculations and embrace modern financial tools and strategies.

Leveraging Payroll Software for Accuracy

The modern entrepreneur should rarely, if ever, calculate FUTA by hand. Automated payroll systems (like Gusto, QuickBooks, or ADP) automatically track the $7,000 wage base per employee, calculate the appropriate credits, and handle the quarterly deposits and annual Form 940 filings. Using these tools reduces the risk of human error and ensures that you never miss a deadline, saving money on potential penalties.

Planning for Year-End Tax Liabilities

Since FUTA is front-loaded—meaning you pay most of it at the beginning of the year when employees have not yet hit the $7,000 cap—cash flow can be tighter in Q1 and Q2. As the year progresses and more employees cross the threshold, your FUTA liability drops to zero for those individuals. Financial officers should plan for higher payroll tax outflows in the first half of the year and allocate resources accordingly.

Why FUTA Matters for Your Bottom Line

Ultimately, the FUTA tax is a relatively small but mandatory component of business finance. By understanding the credit system, staying on top of filing deadlines, and accurately budgeting for the “real cost” of labor, business owners can ensure they remain compliant while keeping their financial house in order. In the world of business, knowledge of these “hidden” costs is what separates a struggling startup from a sustainable, profitable enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.