In the world of mathematics, the fraction 1/3 is one of the most fundamental ratios we encounter. However, when we transition from abstract theory to the practical world of personal finance, corporate accounting, and global investing, this simple fraction reveals a complex reality. The decimal equivalent of 1/3 is 0.333…, a “repeating” or “recurring” decimal that never ends. While a student might simply write “0.33” on a test, a financial professional knows that the difference between 0.33 and 0.3333333 can represent thousands, or even millions, of dollars in a high-stakes environment.

Understanding how to convert 1/3 into a decimal and, more importantly, understanding how to manage that decimal in financial contexts is a critical skill for anyone looking to master their money. This article explores the nuances of the 1/3 decimal, its implications for your portfolio, and the ways in which precision—or the lack thereof—shapes the financial landscape.

The Mathematics of 1/3: Accuracy in Personal Finance

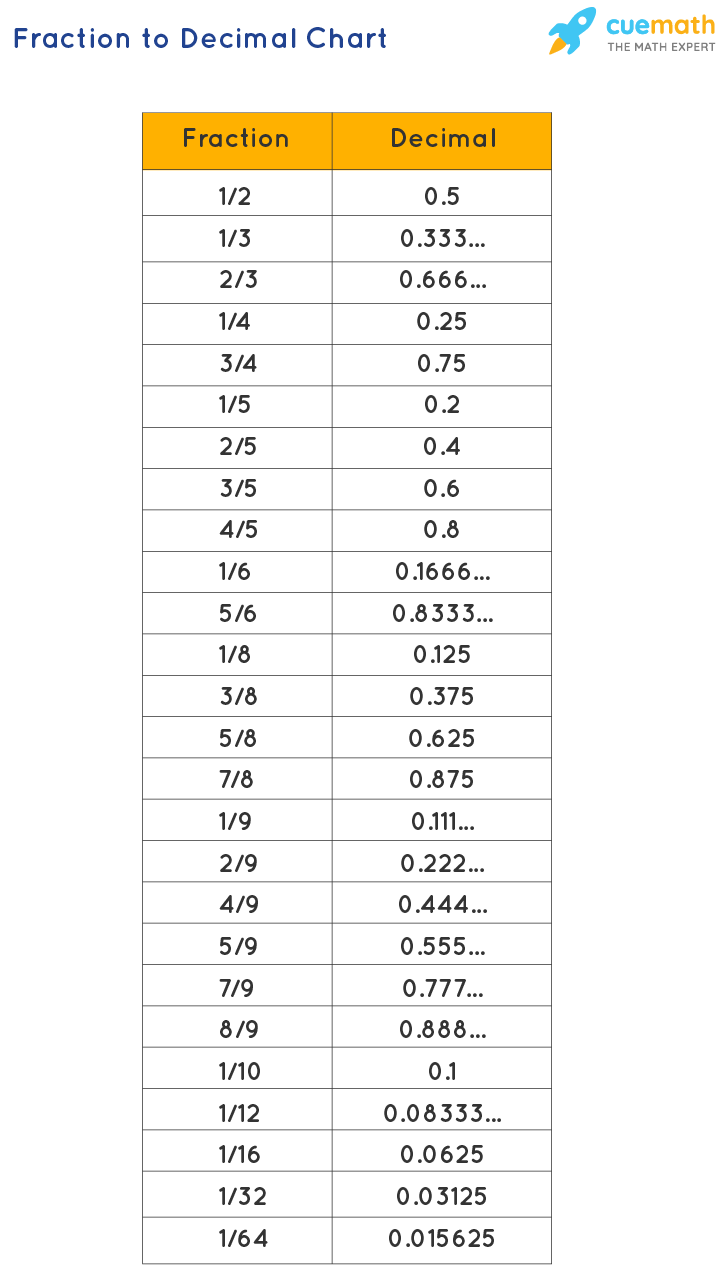

To answer the most basic question: the decimal for 1/3 is approximately 0.333333. Because 3 does not go into 10 evenly, the division results in a remainder that repeats infinitely. In financial terms, we often truncate this to 33.33% or 0.33, but this rounding is not without its consequences.

From Fractions to Decimals: The 0.3333 Infinity

When we divide 1 by 3, we are essentially looking for a way to express a third of a whole in a base-10 system. Because our currency and accounting systems are built on base-10 (cents, dollars, tens, hundreds), the number 1/3 is technically “incommensurable” with a finite decimal string.

In personal finance, this becomes relevant when splitting bills, calculating interest, or dividing assets. If you and two friends are splitting a $100 investment, a perfect split is impossible in physical currency. Someone will always be responsible for that “extra” penny, or the accounts will reflect 0.33, 0.33, and 0.34. While a penny seems trivial, the principle of precision is the bedrock of fiscal responsibility.

Rounding Errors and Their Impact on Your Savings

In long-term savings and interest-bearing accounts, rounding errors can compound. Suppose a financial institution calculates a specific fee or a dividend payout based on a 1/3 ratio. If they round down to 0.33 instead of using the infinite 0.333…, they are effectively retaining 0.0033… of the total value.

On a micro-level, this is negligible. However, in the world of high-frequency trading or massive pension fund management, these “fractions of a fraction” add up. For the individual saver, understanding that 1/3 is roughly 33.33% helps in setting realistic expectations for “Rule of Thirds” budgeting—where one might allocate 1/3 of income to housing, 1/3 to living expenses, and 1/3 to savings.

1/3 in Investing: Asset Allocation and Diversification

Professional investors rarely deal in “clean” whole numbers. Whether you are rebalancing a portfolio or calculating dividend yields, the decimal for 1/3 appears constantly. It is most frequently seen in the “Three-Fund Portfolio” strategy, a popular investment philosophy that emphasizes simplicity and diversification.

The Rule of Thirds in Portfolio Management

Many conservative investors follow a strategy of splitting their assets into three equal categories: Domestic Stocks, International Stocks, and Total Bond Markets. This means each category should ideally occupy 33.33% of the total portfolio value.

When the market fluctuates, these percentages shift. If your domestic stocks grow while your bonds stagnate, your 1/3 allocation might become 40%. Rebalancing requires you to sell a portion of the winning asset to return to that 0.333… decimal. Investors who use automated “Robo-advisors” rely on algorithms that can calculate these decimals to eight or more places, ensuring that the rebalancing is as precise as the software allows, minimizing the “slippage” that occurs when trades are rounded to the nearest whole dollar.

Calculating Recurring Returns and Compound Growth

If an investment is expected to grow by a certain factor that involves a third—such as a project expected to return 1/3 of the initial capital annually—the decimal 0.333 becomes the variable in the compound interest formula.

When you use the formula $A = P(1 + r/n)^{nt}$, and $r$ is expressed as a decimal, using 0.33 instead of the actual repeating decimal will result in a significant underestimate of future wealth. Over a 30-year horizon, that small discrepancy in the third and fourth decimal places can lead to a gap of thousands of dollars in projected returns. Precision in the decimal representation of 1/3 is not just a mathematical curiosity; it is a requirement for accurate financial forecasting.

Corporate Finance: Managing Equity and Dividends

In the corporate world, 1/3 is a common figure in ownership structures and profit-sharing agreements. When three founders start a company with equal equity, they each hold 33.33% of the shares. However, the legal and financial recording of these shares requires a sophisticated understanding of how decimals work in ledger systems.

Splitting Shares and Ownership Ratios

A corporation might have 1,000,000 shares. If three partners own 1/3 each, they would each own 333,333.33 shares. Since you generally cannot own a fraction of a share in traditional corporate registries (though fractional shares are becoming common in retail apps), the company must decide how to handle the remaining share.

This is where “cap table” management comes into play. Financial officers must account for the 0.333… decimal by either issuing one extra share to a lead partner or by utilizing “units” of interest that can be broken down more granularly. Failure to account for the decimal for 1/3 correctly in legal documents can lead to “dilution” disputes, where a founder feels their 1/3 stake has been rounded down unfairly over successive funding rounds.

Budgeting with Non-Terminating Decimals

Corporate budgeting often involves dividing annual budgets into thirds (for terms or tranches). If a marketing department is granted a $1,000,000 budget to be spent in three equal phases, the decimal 0.3333 becomes the multiplier for each phase ($333,333.33).

In accounting, this requires “reconciliation.” Because the decimal 0.3333… never ends, the final period’s budget must be adjusted to ensure the total equals the original $1,000,000. Professionals call this “plugging the difference.” In high-level business finance, transparency about these rounding adjustments is essential for passing audits and maintaining clear financial statements.

Tools and Technology for Financial Precision

As we move toward an increasingly digital financial system, the way our software handles the decimal for 1/3 has become a topic of significant interest. Not all calculators are created equal, and the way a system “sees” 1/3 can change the outcome of a transaction.

How Financial Calculators Handle 1/3

Most standard calculators will display “0.3333333” and stop at the edge of the screen. However, dedicated financial calculators (like the HP 12C or the TI BA II Plus) often store many more digits in their internal memory than they display.

When you are calculating the Present Value (PV) of an annuity that pays out three times a year, the calculator uses the most precise version of the decimal available. For a financial analyst, the goal is to never clear the calculator between steps. If you manually type in “0.33” after a calculation, you have introduced a “truncation error” that can skew the final results of a multi-million dollar valuation.

Avoiding “Floating Point” Errors in Accounting Software

In software development for finance—such as the code behind banking apps or tax software—developers must deal with “floating-point arithmetic.” Computers represent numbers in binary, and just as 1/3 doesn’t fit perfectly into a base-10 decimal, many base-10 decimals don’t fit perfectly into binary.

To combat this, high-end financial software uses a “Decimal” data type rather than a “Float” or “Double” to ensure that 1/3 is handled with the appropriate number of significant digits. As a user of financial tools (like Excel or Google Sheets), you can observe this by increasing the decimal places in a cell. Typing =1/3 and expanding the view will show you how much precision the tool is actually using. For professional-grade financial modeling, maintaining at least four to six decimal places is the industry standard to ensure that 0.333333 is as accurate as possible.

Conclusion: The Value of Precision in a Fractional World

While the question “what is a decimal for 1/3” has a simple mathematical answer (0.333…), its application in the world of money is anything but simple. Whether you are a retail investor trying to rebalance a three-fund portfolio, a founder splitting equity with two partners, or a saver calculating the impact of fees, that repeating “3” represents a constant need for precision.

In the realm of money, the goal is not just to know the number, but to understand its implications. Rounding 1/3 to 0.3 or 0.33 might be convenient, but in a world where compound interest and high-volume transactions reign supreme, the “infinite” nature of 1/3 serves as a reminder that small details matter. By mastering the decimal representation of fractions, you equip yourself with the accuracy needed to manage wealth, minimize errors, and maximize your long-term financial health. Precision is not just about numbers; it is about the integrity of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.