Understanding how interest works is the cornerstone of financial literacy. Whether you are managing a credit card balance, planning for a mortgage, or looking to maximize the growth of your savings account, the ability to calculate interest rates on a monthly basis is an essential skill. While many financial institutions advertise an Annual Percentage Rate (APR), the actual movement of money often happens in monthly cycles.

In this comprehensive guide, we will break down the mechanics of monthly interest, explore the differences between simple and compound interest, and provide you with the formulas necessary to take full control of your personal or business finances.

Understanding the Fundamentals: APR vs. Monthly Interest

Before diving into the formulas, it is crucial to distinguish between the two primary ways interest is communicated. Most lenders and banks use the Annual Percentage Rate (APR) as their headline figure. However, the APR is a “macro” view of your cost of borrowing or rate of return. To understand your “micro” monthly obligations, you must know how to deconstruct that annual figure.

What is the Annual Percentage Rate (APR)?

The APR represents the total cost of borrowing money over the course of a full year. It includes the base interest rate plus any additional fees or costs associated with the transaction. Because it is standardized by law in many regions, it allows consumers to compare different loan products side-by-side. However, the APR doesn’t tell you how much interest will be added to your balance when your statement closes at the end of the month.

Defining the Monthly Periodic Rate

The monthly periodic rate is the APR divided by the number of periods in a year—in this case, twelve. This is the rate actually applied to your balance each month. For example, if you have a credit card with an 18% APR, your monthly periodic rate is 1.5%. Understanding this distinction is the first step in accurately predicting your monthly financial outflows or inflows.

Step-by-Step Guide to Calculating Simple Monthly Interest

Simple interest is the most straightforward way to calculate the cost of a loan or the growth of an investment. It is calculated only on the principal amount—the original sum of money borrowed or invested. While less common in modern consumer revolving credit (like credit cards), it is frequently used for short-term personal loans and certain types of certificates of deposit (CDs).

The Simple Interest Formula

To calculate simple monthly interest, you use a variation of the standard interest formula: $I = P times r times t$.

- I stands for the Interest amount.

- P stands for the Principal (the initial amount).

- r stands for the Monthly Interest Rate (Annual Rate / 12).

- t stands for the Time (number of months).

To find the interest for exactly one month, $t$ would be 1. The formula simplifies to:

Monthly Interest = Principal × (Annual Rate / 12)

A Practical Example: Personal Loans

Suppose you take out a $10,000 personal loan with a 6% annual simple interest rate. To find the interest you owe for the first month:

- Convert the annual percentage to a decimal: 0.06.

- Divide by 12 to find the monthly rate: $0.06 / 12 = 0.005$ (or 0.5%).

- Multiply the principal by the monthly rate: $$10,000 times 0.005 = $50$.

In this scenario, you are paying $50 in interest for that month. If the loan is a “non-amortizing” simple interest loan, you would pay $50 every month until the principal is repaid.

The Power of Compounding: Calculating Interest on Savings and Credit Cards

Unlike simple interest, compound interest is calculated on the principal amount plus any interest that has already been added. This is often described as “interest on interest.” For savers, compounding is a powerful engine for wealth creation. For borrowers, it can lead to a rapidly growing debt spiral if not managed correctly.

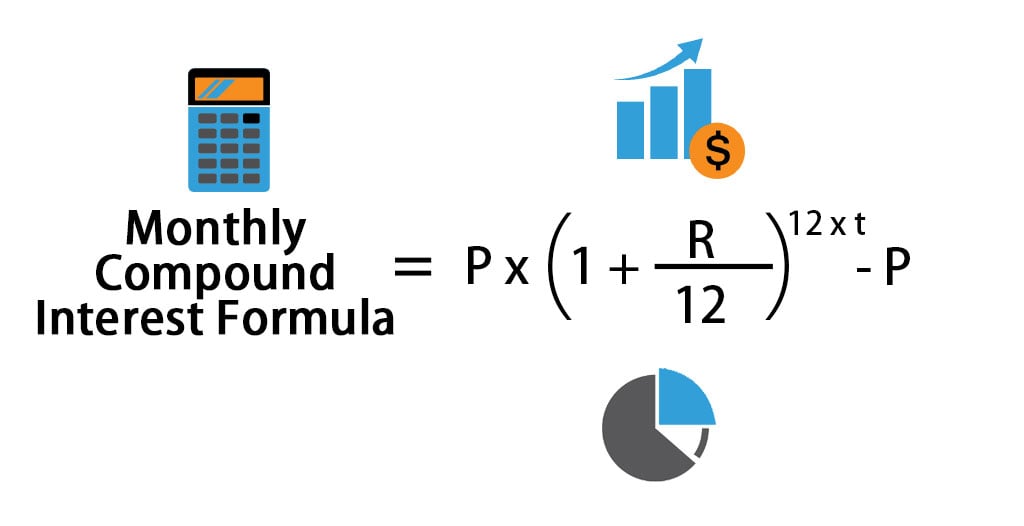

How Compound Interest Works Monthly

When interest is compounded monthly, the balance grows each month, and the following month’s interest is calculated on that new, larger balance. The formula for the total balance ($A$) after a certain time is:

$A = P(1 + r/n)^{nt}$

Where:

- P is the principal.

- r is the annual interest rate (decimal).

- n is the number of times interest compounds per year (12 for monthly).

- t is the number of years.

To find just the interest for a specific month, you would subtract the previous month’s balance from the current month’s balance.

Calculating Credit Card Interest (Average Daily Balance)

Credit cards are a unique case. Most credit card issuers use a method called the “Average Daily Balance.” To calculate this:

- Add up the balance on your card for every single day in the billing cycle.

- Divide that total by the number of days in the cycle (usually 30). This gives you the Average Daily Balance.

- Multiply the Average Daily Balance by the Daily Periodic Rate (APR / 365).

- Multiply that result by the number of days in the billing cycle.

This nuance is why your monthly interest charge might fluctuate slightly even if your month-end balance looks the same—it depends on when during the month you made your purchases.

Key Factors That Influence Your Monthly Interest Costs

Knowing the formula is only half the battle. To truly master your finances, you must understand the variables that determine the “r” (the rate) in your equations. Interest rates are not arbitrary; they are a reflection of risk, market conditions, and institutional policy.

Credit Scores and Risk Assessment

From a lender’s perspective, the interest rate is the price of risk. If you have a high credit score, you are seen as a “low-risk” borrower, and lenders will reward you with a lower APR. A difference of just 2% on a mortgage or auto loan can result in thousands of dollars saved over the life of the loan. When you calculate your monthly interest, remember that improving your credit score is the most effective way to lower that monthly “I” in your formula.

Fixed vs. Variable Interest Rates

When calculating monthly interest, you must know if your rate is fixed or variable.

- Fixed Rates: The interest rate remains the same for the duration of the loan. This makes monthly calculations predictable and budgeting easier.

- Variable (Floating) Rates: These rates are tied to an index, such as the Prime Rate. If the central bank raises interest rates, your APR—and consequently your monthly interest payment—will increase. Those using variable-rate products should recalculate their interest exposure whenever market conditions shift.

Leveraging Financial Tools for Precision

While manual calculations are excellent for understanding the logic of finance, modern financial management often requires the speed and precision of digital tools. Utilizing software can help you model different “what-if” scenarios, such as how much interest you would save by paying an extra $100 toward your principal each month.

Using Excel and Google Sheets Formulas

Spreadsheet software is a powerful ally for anyone serious about money management. You can use built-in functions to skip the manual math:

- =IPMT: This function calculates the interest payment for a given period for an investment or loan based on periodic, constant payments and a constant interest rate.

- =PMT: This calculates the total monthly payment (principal + interest).

- Custom Formula: You can build your own tracker by setting up columns for “Beginning Balance,” “Interest (Balance * Rate/12),” “Principal Payment,” and “Ending Balance.”

Online Amortization Calculators

For complex loans like mortgages, an amortization schedule is vital. These calculators show you exactly how much of your monthly payment goes toward interest versus principal. In the early years of a long-term loan, the majority of your monthly payment is often consumed by interest. Seeing this visualized can provide the necessary motivation to make extra principal payments, which drastically reduces the total interest paid over time.

By mastering these calculations, you move from a passive participant in your financial life to an active strategist. Whether you are crunching numbers to get out of debt or calculating the monthly growth of your retirement fund, understanding the monthly interest rate ensures that you always know exactly where your money is going.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.