Equity lending is a powerful financial tool that allows individuals and businesses to leverage the value of their assets to secure funding. While the term itself might sound complex, at its core, it’s about using what you own to borrow money. This concept is deeply intertwined with the “Money” section of our website, touching upon personal finance, business finance, and the strategic use of financial tools. However, its implications extend far beyond mere transactions, resonating with the broader principles of “Brand” building and even the innovative applications found in “Tech.”

Imagine your assets – whether they are your home, your business’s equipment, or even certain intangible business values – as dormant capital. Equity lending breathes life into this capital, transforming it into liquid funds that can be used for a multitude of purposes. This could range from funding a critical business expansion, consolidating high-interest debt, investing in new technology, or even securing personal financial stability. Understanding equity lending is therefore not just about grasping a financial mechanism; it’s about understanding a pathway to growth, innovation, and enhanced financial control.

This article will delve into the intricacies of equity lending, exploring what it is, how it works, its various forms, and the key considerations for anyone looking to utilize this financial strategy. We’ll also touch upon how technology is influencing equity lending and how a strong brand can impact your ability to access these valuable financial resources.

Understanding the Fundamentals of Equity Lending

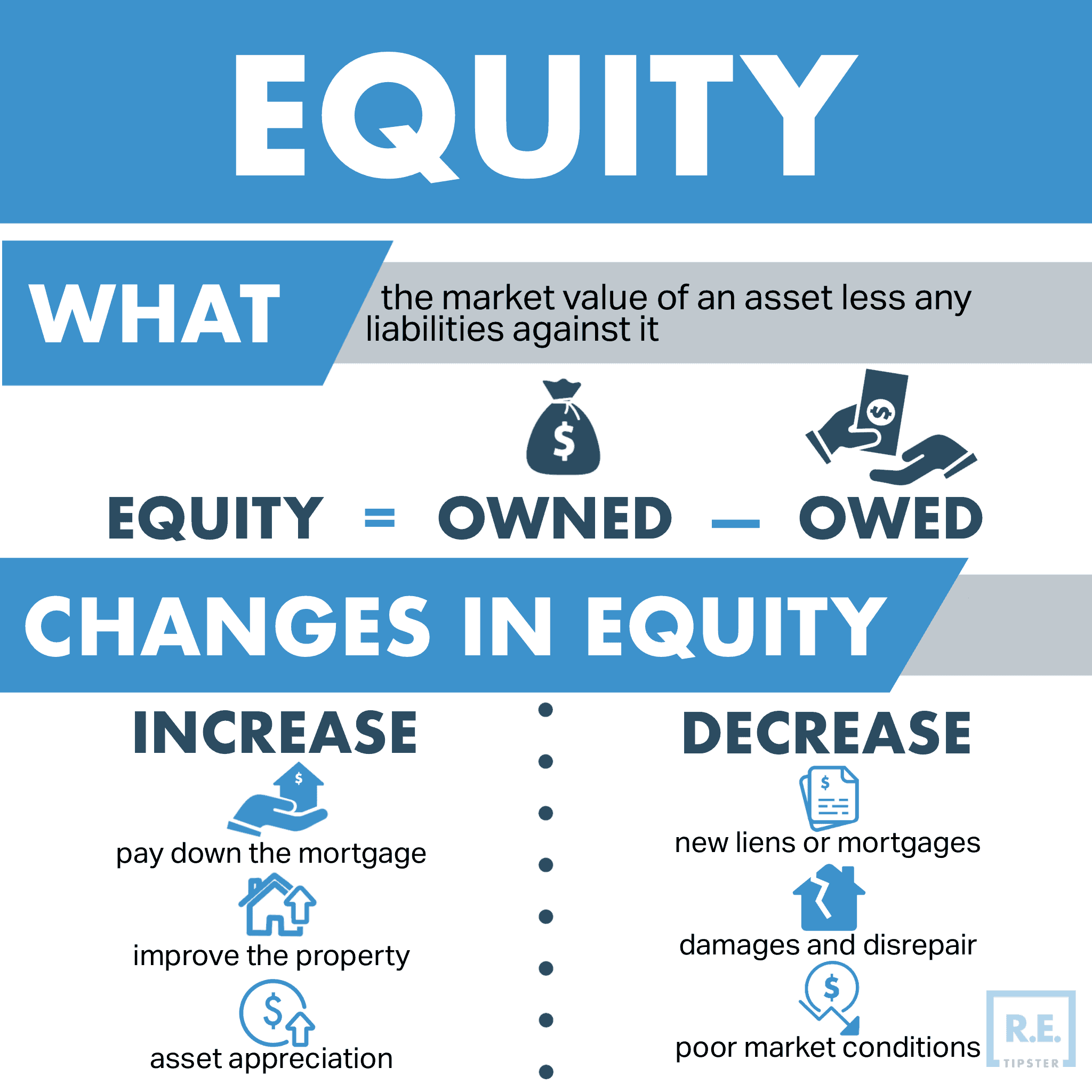

At its most basic, equity lending involves borrowing money against the equity you hold in an asset. Equity, in this context, refers to the difference between the market value of an asset and any outstanding debt secured against it. For instance, if your home is valued at $500,000 and you owe $200,000 on your mortgage, you have $300,000 in home equity. This equity can then serve as collateral for a new loan.

How Equity Lending Works: The Collateral Connection

The fundamental principle behind equity lending is collateralization. The lender is taking on a certain level of risk when they provide you with funds. To mitigate this risk, they require an asset of value that can be seized and sold if the borrower defaults on their loan payments. This asset is the equity you hold. The lender will typically appraise the asset to determine its market value and the amount of equity available.

The loan amount you can secure will be a percentage of your available equity, often referred to as the loan-to-value (LTV) ratio. Lenders have varying LTV thresholds, but it’s common to see loans for 70-90% of the available equity. This ensures that the lender has a buffer in case the asset’s value declines or if there are costs associated with foreclosure and sale.

Repayment terms for equity loans vary significantly. They can range from short-term loans with a lump-sum repayment to longer-term loans with monthly installments, often with interest. The interest rates can be fixed or variable, depending on the loan product and market conditions.

Types of Equity Lending: Tailoring Funding to Your Needs

Equity lending isn’t a monolithic concept; it encompasses several distinct products, each designed to meet different financial needs. Understanding these variations is crucial for selecting the most appropriate option.

Home Equity Loans: Tapping into Your Residential Asset

The most common form of equity lending is the home equity loan. This is a traditional loan where you borrow a lump sum of money against the equity in your home. You receive the entire amount upfront, and then you repay it over a fixed period with regular payments, usually including both principal and interest.

- Uses: Home equity loans are often used for significant expenses like home renovations, consolidating debt, funding education, or even covering unexpected medical bills. The stability of your home equity makes it a reliable source for substantial funding.

- Considerations: It’s important to remember that your home serves as collateral. Failure to repay the loan can result in foreclosure. However, the interest on home equity loans is often tax-deductible, which can be a significant financial advantage.

Home Equity Lines of Credit (HELOCs): Flexible Access to Funds

A Home Equity Line of Credit (HELOC) is another popular option for homeowners. Unlike a home equity loan, a HELOC functions more like a credit card. You are approved for a certain credit limit based on your home equity, and you can draw funds as needed during a “draw period.” You typically only pay interest on the amount you’ve borrowed. After the draw period ends, you enter a repayment period where you pay back both principal and interest.

- Uses: HELOCs are ideal for ongoing projects or situations where you’re unsure of the exact amount you’ll need. This could include phased home renovations, managing unpredictable business expenses, or covering recurring medical treatments. The flexibility is a key advantage.

- Considerations: The variable interest rates common with HELOCs can mean your monthly payments fluctuate. It’s crucial to have a clear repayment strategy, especially as the repayment period begins. As with home equity loans, your home is at risk.

Business Equity Loans: Fueling Corporate Growth

For established businesses, leveraging business assets for equity lending can be a vital growth strategy. This can include loans secured against commercial real estate, machinery, equipment, or even accounts receivable. The availability and terms of these loans depend heavily on the business’s financial health, its assets, and the industry it operates in.

- Uses: Business equity loans are instrumental in funding expansions, purchasing new equipment, acquiring inventory, or bridging cash flow gaps. They provide a way for businesses to unlock capital that is tied up in their physical assets.

- Considerations: Lenders will conduct rigorous due diligence on the business’s financials and the value of the collateral. The loan terms are often tailored to the specific business and asset. A strong business plan and a history of profitability are usually prerequisites.

Other Forms of Equity Lending: Beyond the Traditional

While home and business equity loans are the most prevalent, the concept of equity lending can extend to other assets. For example, some lenders offer loans against the equity in investment properties or even certain types of business intellectual property, though these are often more specialized and complex.

- Uses: These niche equity lending products can be useful for investors looking to diversify their portfolios or businesses with significant intellectual assets seeking funding.

- Considerations: The appraisal and valuation of these less tangible assets can be more complex, leading to more intricate loan structures and potentially higher interest rates due to increased risk.

The Strategic Advantages of Equity Lending

The decision to pursue equity lending should be strategic, aligned with your financial goals and risk tolerance. When used wisely, equity lending offers significant advantages that can propel personal and business growth.

Financial Flexibility and Access to Capital

The primary allure of equity lending is the increased financial flexibility it provides. It allows individuals and businesses to access substantial sums of capital that might otherwise be out of reach. This immediate access can be critical for seizing time-sensitive opportunities or addressing urgent financial needs.

- For Individuals: Whether it’s consolidating high-interest credit card debt into a single, lower-interest loan, funding a child’s education, or making essential home repairs, equity lending can provide the necessary capital without requiring the sale of an asset. This preserves your ownership and potential for future appreciation.

- For Businesses: For businesses, equity lending can be a lifeline for growth. It can fund the purchase of new technology that improves efficiency, enable the expansion into new markets, or provide the working capital needed to navigate periods of seasonal demand. This access to capital can be the difference between stagnation and significant progress.

Potential for Lower Interest Rates

Compared to unsecured loans, equity loans often come with lower interest rates. This is because the collateralization reduces the lender’s risk. By offering an asset as security, you demonstrate your commitment to repayment, allowing the lender to offer more favorable terms.

- Debt Consolidation: A key benefit for individuals is the ability to consolidate multiple high-interest debts (like credit cards) into a single equity loan with a lower interest rate. This can significantly reduce your overall interest payments over time and simplify your financial management.

- Business Investment: For businesses, lower interest rates on equity loans mean that the cost of borrowing for expansion or investment is reduced. This can improve the profitability of new ventures and make significant capital expenditures more feasible.

Tax Benefits (for Home Equity)

In many jurisdictions, the interest paid on home equity loans and HELOCs used for certain purposes, such as home improvements, can be tax-deductible. This can provide a significant financial advantage, effectively reducing the overall cost of borrowing.

- Maximizing Deductions: It’s crucial to consult with a tax advisor to understand the specific rules and limitations regarding tax deductibility for home equity interest. Proper documentation of how the funds are used is essential for claiming these deductions.

Key Considerations and Potential Risks

While equity lending offers compelling benefits, it’s essential to approach it with a clear understanding of the associated risks. Responsible borrowing and careful planning are paramount.

The Risk of Losing Your Asset

The most significant risk in equity lending is the potential loss of the asset used as collateral. If you are unable to meet your loan repayment obligations, the lender has the legal right to seize and sell the asset to recover their losses.

- Financial Prudence: Before taking out an equity loan, conduct a thorough assessment of your income stability and your ability to manage the new loan payments alongside your existing financial commitments. Overextending yourself financially can have severe consequences.

- Emergency Planning: It’s wise to have an emergency fund in place to cover unexpected expenses that could jeopardize your loan payments.

Understanding Loan Terms and Fees

Equity lending products come with various terms, conditions, and fees. It’s crucial to understand these thoroughly before signing any agreement.

- Interest Rates: Be aware of whether the interest rate is fixed or variable and how changes in market rates might affect your payments, especially with HELOCs.

- Fees: Lenders may charge origination fees, appraisal fees, annual fees (for HELOCs), and closing costs. Factor these into the overall cost of the loan.

- Repayment Schedules: Understand the exact repayment schedule, including the length of the loan term and the amount of each payment.

Impact on Your Credit Score

While taking out an equity loan itself won’t necessarily harm your credit score, consistent late payments or defaults will significantly damage it. Conversely, making timely payments on your equity loan can help improve your credit history over time.

- Responsible Credit Management: Treat your equity loan as you would any other financial obligation – with responsibility and diligence.

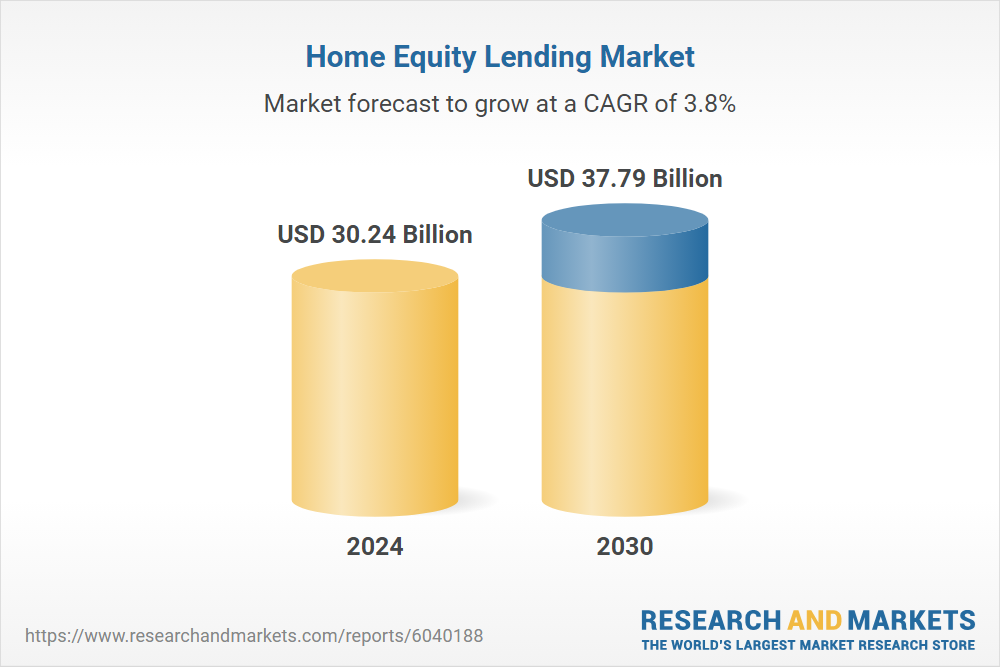

Equity Lending in the Digital Age: The Role of Technology

The digital revolution has significantly impacted the landscape of equity lending, making the process more accessible, efficient, and transparent. Technology plays a vital role in how these financial products are accessed, managed, and even originated.

Streamlined Application and Approval Processes

Online platforms and financial technology (FinTech) companies have transformed the application and approval processes for equity loans. Gone are the days of lengthy paper-based applications and weeks of waiting for a decision.

- Digital Platforms: Many lenders now offer online application portals where borrowers can submit documentation, receive real-time updates, and even get preliminary approvals within hours or days.

- Data Analytics and AI: Artificial intelligence (AI) and advanced data analytics are being used by lenders to assess risk more accurately and efficiently, speeding up the underwriting process. This can also lead to more personalized loan offers.

Enhanced Accessibility and Broader Reach

Technology has democratized access to equity lending. Individuals and businesses in more remote areas, or those who may have found traditional banking channels challenging, can now connect with lenders online.

- Comparison Tools: Numerous online tools allow borrowers to compare offers from multiple lenders side-by-side, making it easier to find the best rates and terms.

- Digital Wallets and Payment Systems: Technology also facilitates easier repayment through online portals and integration with digital payment systems.

Innovations in Asset Valuation

The valuation of assets, particularly for business equity lending, is also benefiting from technological advancements.

- Automated Valuation Models (AVMs): For real estate, AVMs can provide rapid estimates of property values, which can be a preliminary step in the equity lending process.

- Digital Due Diligence: Technologies for digital verification of business assets and financial health are making the due diligence process faster and more robust.

The Synergy Between Brand and Equity Lending

While not as direct as the connection with “Money,” your “Brand” can play a surprisingly significant role in your ability to access and secure favorable terms for equity lending, especially in the business context.

Building Trust and Credibility for Businesses

For businesses, a strong and reputable brand signals stability and reliability to lenders. A well-established corporate identity, consistent marketing efforts, and positive customer reviews can all contribute to a lender’s confidence in the business’s ability to repay a loan.

- Brand Reputation as an Asset: In some advanced business equity lending scenarios, a strong brand name and its associated goodwill can even be considered a factor in valuation, indirectly supporting the ability to secure funding.

- Case Studies and Track Record: Demonstrating successful past projects and a solid track record, often showcased through case studies and marketing materials, builds a lender’s trust in your business’s operational capacity and financial acumen.

Personal Branding for Individuals

For individuals, particularly entrepreneurs or those seeking loans for business ventures, their personal brand – their reputation, expertise, and network – can influence lender perception.

- Demonstrating Capability: A well-defined personal brand that highlights financial literacy, strong leadership skills, and a clear vision can instill confidence in lenders, especially for startup funding or expansion loans where personal guarantees are involved.

Conclusion: Strategic Leverage for Financial Growth

Equity lending is a sophisticated financial tool that, when understood and utilized effectively, can unlock significant opportunities for both individuals and businesses. By transforming dormant assets into liquid capital, it provides the means to achieve financial goals, fuel growth, and navigate economic challenges.

From the straightforward security of home equity loans and the flexible access of HELOCs to the strategic imperative of business equity lending, the options are diverse. However, the power of equity lending is intrinsically linked to responsible financial management. A thorough understanding of loan terms, a realistic assessment of repayment capabilities, and a clear appreciation of the risks involved are paramount.

Furthermore, in our increasingly digital world, technology is reshaping the equity lending landscape, making it more efficient and accessible. And while financial acumen is key, the strength of your brand – be it personal or corporate – can significantly influence your ability to secure favorable terms and build trust with lenders.

Ultimately, equity lending is not just about borrowing money; it’s about strategic leverage. It’s about intelligently utilizing the value you’ve built to create further value and achieve your financial aspirations. By approaching it with knowledge, caution, and a clear strategic vision, equity lending can be a powerful ally on your journey towards financial success and innovation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.