In an age where personal data breaches are a regrettably common occurrence, safeguarding one’s financial identity has become paramount. One of the most potent tools available to consumers for achieving this protection is the security freeze, often referred to as a credit freeze. Far more than a mere inconvenience, a security freeze is a robust defense mechanism designed to prevent unauthorized access to your credit report, thereby thwarting potential identity thieves from opening new accounts in your name. Understanding this critical financial tool is not just an advantage; it’s a necessity for anyone serious about personal finance and maintaining their financial integrity in a digitally interconnected world.

A security freeze fundamentally locks down your credit file, making it inaccessible to most third parties. This action significantly complicates the efforts of fraudsters who might try to apply for new credit cards, loans, or other financial products using stolen personal information. While it might introduce a minor temporary hurdle for your own legitimate credit applications, the peace of mind and substantial protection it offers against the devastating impact of identity theft often far outweigh these considerations. This article will delve into the intricacies of a security freeze, exploring its function, benefits, implementation, and the practical implications for your financial life.

Understanding the Core Concept of a Security Freeze

At its heart, a security freeze is a proactive measure that empowers consumers to control access to their sensitive credit information. It’s a strategic move in personal finance management that can save individuals from years of financial recovery following identity theft.

What Exactly is a Credit Freeze?

A credit freeze, officially known as a security freeze, is a service offered by the three major credit reporting agencies: Equifax, Experian, and TransUnion. When you place a freeze on your credit report, these bureaus are instructed not to release your credit file to potential creditors without your explicit permission. This means that if an identity thief attempts to open a new credit card, take out a loan, or secure other lines of credit in your name, the lender will be unable to access your credit report to assess your creditworthiness. Without access to this crucial information, the lender will likely reject the application, thus preventing the fraudulent account from being opened. It’s a fundamental barrier that stops unauthorized credit applications dead in their tracks, serving as a powerful deterrent against financial fraud. Unlike a simple fraud alert, which merely flags your report for extra scrutiny, a freeze essentially closes the door to all but pre-authorized access.

How a Security Freeze Protects Your Financial Identity

The primary mechanism by which a security freeze protects your financial identity is by breaking the chain of information required for a new credit application. When you apply for credit—be it a mortgage, an auto loan, or a new credit card—the lender performs a “hard inquiry” into your credit report to evaluate your financial history and repayment reliability. If a security freeze is in place, this hard inquiry cannot be completed. The credit bureau will notify the inquiring party that the report is frozen, and thus, no credit file can be provided. This effectively renders any fraudulent application futile, as no legitimate lender will approve credit without reviewing the applicant’s credit history. This protection extends across various financial products, from retail store cards to significant loans, offering a comprehensive shield against a wide array of potential identity theft scenarios.

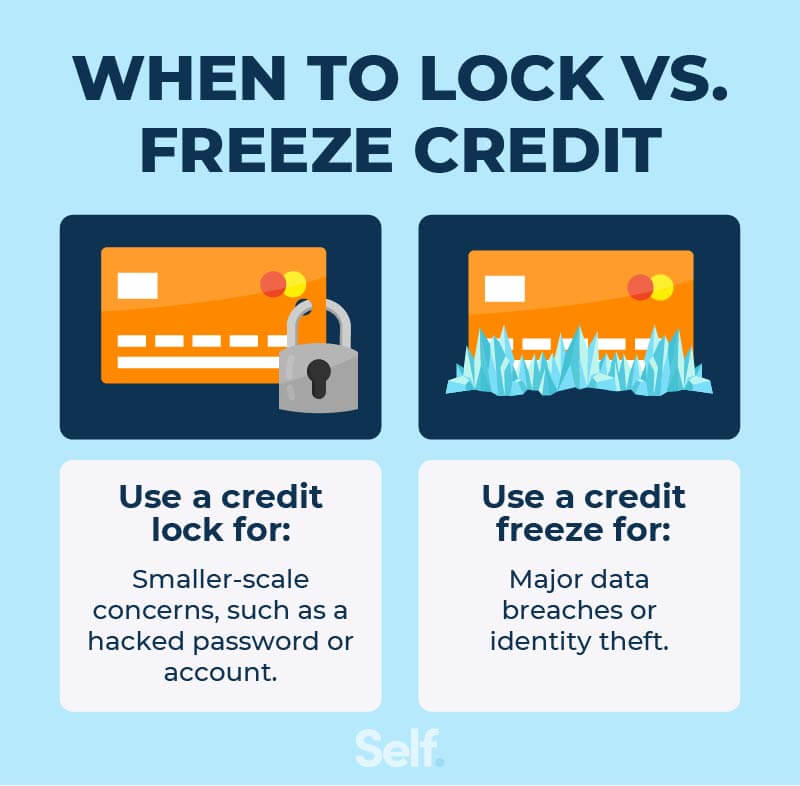

Distinguishing a Security Freeze from a Fraud Alert

It’s crucial for consumers to understand the difference between a security freeze and a fraud alert, as they serve different purposes and offer varying levels of protection. A fraud alert is a flag placed on your credit report that notifies potential creditors to take extra steps to verify your identity before extending credit. This typically involves contacting you by phone to confirm that you initiated the credit application. While a fraud alert can be helpful, especially after a suspected breach, it relies on the diligence of the creditor to follow through on the verification. It does not actively block access to your credit report.

A security freeze, on the other hand, is a much more stringent measure. It completely restricts access to your credit report, preventing any new inquiries from being processed unless you temporarily lift or “thaw” the freeze. This makes it a more robust and proactive defense against identity theft. Consumers can place a fraud alert for an initial period (usually one year, renewable) or an extended period (seven years if you’ve been a victim of identity theft), whereas a security freeze remains in effect indefinitely until you choose to remove it. Choosing between the two often comes down to the level of risk perceived and the desired level of control over your credit file. For maximum protection, a security freeze is generally recommended.

The Strategic Advantages of Implementing a Security Freeze

Implementing a security freeze is a strategic financial decision that offers significant advantages, particularly in an era riddled with data vulnerabilities. These benefits extend beyond mere prevention, offering a profound sense of security.

Robust Protection Against Identity Theft

The most compelling advantage of a security freeze is its unmatched ability to protect against identity theft. With millions of personal records exposed through data breaches annually, the risk of your sensitive information falling into the wrong hands is higher than ever. Identity thieves thrive on exploiting this stolen data to open new credit accounts, rack up debt, and ruin victims’ financial standing. A security freeze acts as a firewall, making it incredibly difficult for fraudsters to monetize stolen information through new credit applications. By proactively freezing your credit, you remove one of the most significant pathways for identity thieves to cause financial harm, providing a robust defense that is largely unparalleled by other preventative measures.

Preventing Unauthorized Credit Applications

Beyond simply protecting against generalized identity theft, a security freeze directly targets and prevents one of its most damaging manifestations: unauthorized credit applications. Whether it’s a new credit card, a personal loan, an auto loan, or even utilities in your name, each unauthorized account can severely impact your credit score, generate fraudulent debt, and lead to a lengthy and arduous process of dispute and resolution. By blocking access to your credit report, a freeze ensures that lenders cannot process these applications, thereby eliminating the ability of a fraudster to obtain credit in your name. This proactive prevention saves individuals from the stress, financial loss, and time-consuming effort required to repair credit and resolve fraudulent debts.

Peace of Mind in a Data-Breach Era

Perhaps one of the most underrated advantages of a security freeze is the immense peace of mind it provides. Living in a world constantly exposed to news of data breaches can be a source of significant anxiety for financially responsible individuals. Knowing that your most sensitive financial information is locked down and largely inaccessible offers a substantial psychological benefit. It means you can worry less about the potential fallout from a compromised database and focus more on your financial goals. This emotional security is a valuable asset, allowing individuals to manage their money with greater confidence and reduced stress, knowing they’ve taken a critical step to safeguard their financial future.

How to Initiate and Manage a Security Freeze

Implementing a security freeze is a straightforward process, but it requires interaction with all three major credit bureaus. Managing it involves understanding how to temporarily lift or permanently remove the freeze when needed.

Contacting the Three Major Credit Bureaus

To ensure comprehensive protection, you must place a security freeze with each of the three major credit reporting agencies: Equifax, Experian, and TransUnion. Freezing your credit with only one or two bureaus leaves a significant vulnerability, as a potential creditor might pull your report from an unfrozen bureau. Each bureau operates independently, so you’ll need to contact them individually via their dedicated websites, phone numbers, or mail. Typically, the process involves verifying your identity by providing personal information such as your name, address, date of birth, and Social Security number. The Fair Credit Reporting Act (FCRA), as amended by the Economic Growth, Regulatory Relief, and Consumer Protection Act, made placing and lifting security freezes free for all consumers as of September 2018.

Necessary Information for Placing a Freeze

When contacting each credit bureau, be prepared to provide specific personal identifying information. This typically includes:

- Your full legal name (and any previous names)

- Current and previous addresses for the past two years

- Date of birth

- Social Security number

- Proof of identity (e.g., a copy of your driver’s license or state ID)

- Proof of address (e.g., a utility bill or bank statement)

The bureaus require this information to verify your identity and ensure that only you can place a freeze on your file. Once the freeze is placed, each bureau will provide you with a unique PIN or password. This PIN is crucial; you will need it to temporarily lift or permanently remove the freeze in the future, so keep it in a secure place.

Temporarily Thawing or Permanently Lifting a Freeze

There will be times when you need to grant access to your credit report, for example, when applying for a new loan, renting an apartment, or signing up for new utilities. In such cases, you have two options: temporarily thaw (lift) the freeze or permanently remove it.

- Temporarily Thawing: This involves contacting each credit bureau where you placed a freeze and requesting a temporary lift for a specified period (e.g., a few days or weeks) or for a specific lender. You’ll typically need your PIN to do this. Once the specified period expires, the freeze automatically reactivates. This is the recommended approach for specific applications, as it maintains your protection for most of the time.

- Permanently Lifting: If you decide you no longer need the protection of a security freeze, you can request a permanent removal from each bureau, again using your unique PIN. Be cautious when considering a permanent lift, as it re-exposes your credit file to potential unauthorized access. Many financial experts advise keeping a freeze in place indefinitely and only thawing it when absolutely necessary.

Practical Considerations and Potential Drawbacks

While the benefits of a security freeze are substantial, it’s essential to understand its practical implications and potential drawbacks to make an informed financial decision.

Impact on Your Own Credit Applications

The most common practical consideration is how a security freeze affects your own legitimate credit applications. Since a freeze prevents lenders from accessing your credit report, you must proactively “thaw” it whenever you apply for new credit or any service that requires a credit check. Failing to do so will result in your application being delayed or outright rejected. This requires a small amount of foresight and planning, as thawing a freeze isn’t always instantaneous, though credit bureaus are typically quite efficient. For urgent needs, it’s wise to request a thaw a few business days in advance. This minor inconvenience is often viewed as a small price to pay for robust identity theft protection.

Understanding the Costs (or Lack Thereof)

Historically, credit bureaus were permitted to charge a fee for placing or lifting a security freeze, with costs varying by state and bureau. However, as part of the Economic Growth, Regulatory Relief, and Consumer Protection Act, which became effective on September 21, 2018, placing and lifting a security freeze is now free for all consumers nationwide. This elimination of fees significantly reduces any financial barrier to implementing this crucial protection, making it an accessible tool for everyone, regardless of income level. This policy change underscores the federal government’s recognition of the importance of identity theft protection.

Managing Multiple Freezes Across Bureaus

One aspect that can be perceived as a drawback, though manageable, is the need to individually manage a freeze with each of the three major credit bureaus. There isn’t a single centralized system to place or lift a freeze across all three simultaneously. This means you will have three separate accounts, three different sets of instructions, and three unique PINs or passwords to manage. Keeping track of these details is paramount. Many individuals choose to store their PINs in a secure, encrypted digital vault or a locked physical safe. While it adds a layer of administrative effort, this decentralized system is a necessary evil to ensure comprehensive protection, as each bureau holds a distinct version of your credit file.

Who Should Consider a Security Freeze and When?

Deciding whether a security freeze is right for you involves assessing your risk profile and understanding specific life events or circumstances that make it particularly advisable.

Post-Data Breach Scenarios

If you’ve received notification that your personal data has been compromised in a data breach – whether from a retailer, a healthcare provider, or an online service – placing a security freeze should be one of your immediate priorities. Data breaches are direct conduits for identity theft, as they expose your sensitive information to malicious actors. By freezing your credit immediately after a breach, you effectively close the window of opportunity for fraudsters to exploit your stolen data for financial gain. This proactive response can significantly mitigate the risk of becoming a victim of subsequent identity theft.

Individuals with a History of Identity Theft

For those who have previously been victims of identity theft, a security freeze is not just recommended; it’s often a critical ongoing defense. Once your identity has been compromised, you are statistically more likely to be targeted again. Past victims often have had their personal information extensively exposed, making them recurring targets. A permanent security freeze provides a continuous layer of protection, greatly reducing the chances of repeat victimization and allowing individuals to rebuild their financial lives with greater confidence. It serves as a long-term safeguard against the pervasive threat of identity thieves who often reuse or resell stolen data.

Proactive Steps for Financial Security

Beyond specific threats or past incidents, a security freeze is an excellent proactive step for anyone committed to robust financial security. If you are not actively seeking new credit (e.g., not planning to buy a home, car, or open new credit cards in the near future), there is little downside to having a freeze in place. It’s a preventive measure, much like locking your doors or installing an alarm system, but for your financial identity. Many financial experts now recommend that all consumers place a security freeze as a default measure, only lifting it temporarily when necessary. This strategy empowers individuals to take control of their financial data, reducing vulnerability to the ever-present threat of financial fraud and contributing to overall peace of mind regarding their personal finances.

In conclusion, a security freeze is an indispensable tool in the modern financial landscape. It offers unparalleled protection against identity theft by preventing unauthorized access to your credit report. While it requires a bit of administrative effort to implement and manage, the peace of mind and robust security it provides against financial fraud make it a wise and often essential component of personal financial management. By understanding and utilizing a security freeze, consumers can take a powerful step towards safeguarding their financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.