In the ever-evolving landscape of personal finance, individuals are constantly seeking effective strategies to manage their money, grow their wealth, and achieve their financial goals. While various budgeting techniques and investment philosophies exist, one framework that has gained significant traction for its simplicity and effectiveness is the 70/20/10 rule. This rule, often discussed in the context of financial planning, offers a balanced approach to allocating your income, ensuring that you’re not just surviving, but thriving.

This article will delve into the nuances of the 70/20/10 rule for money, exploring how it integrates seamlessly with the core pillars of technology, brand, and money management. We’ll unpack each component of the rule, discuss its practical application, and demonstrate how leveraging modern tools and strategic thinking can amplify its impact. Whether you’re a seasoned investor or just starting your financial journey, understanding and implementing this rule can be a game-changer for your financial well-being.

Understanding the Core Components: The Pillars of Your Financial Allocation

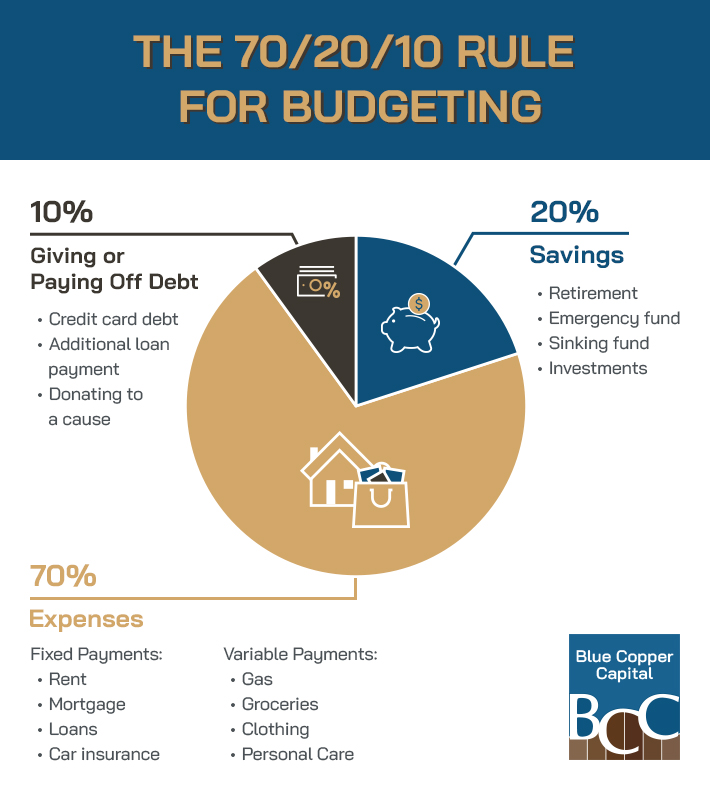

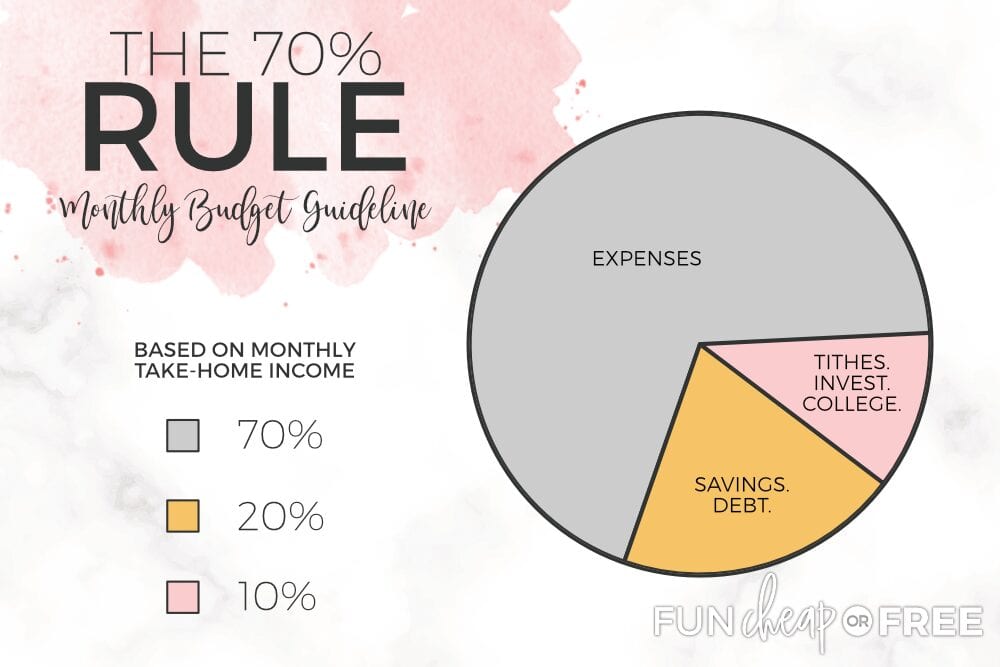

The 70/20/10 rule, in its most fundamental form, suggests that you should allocate 70% of your income towards your immediate needs and wants, 20% towards savings and debt reduction, and 10% towards long-term investments and wealth building. While the percentages are a guideline, the underlying principle is about creating a sustainable financial ecosystem that addresses both present consumption and future security.

Let’s break down each segment and explore how it interacts with the broader themes of technology, brand, and sophisticated money management.

The 70% for Living: Meeting Your Present Needs and Desires

The largest portion of your income, 70%, is dedicated to covering your everyday expenses and enjoying life. This encompasses a wide range of financial outlays, including:

- Essential Expenses: This is the bedrock of your spending. It includes housing (rent or mortgage payments), utilities (electricity, water, gas, internet), groceries, transportation (car payments, fuel, public transport), insurance premiums (health, car, home), and essential healthcare costs. These are the non-negotiable expenses that keep your life running smoothly.

- Discretionary Spending: This is where the “wants” come in. It includes dining out, entertainment (movies, concerts, streaming services), hobbies, clothing, travel, and other lifestyle choices that enhance your quality of life. The key here is balance. While it’s important to enjoy your money, uncontrolled discretionary spending is a primary reason why people struggle to save and invest.

- Debt Servicing (Short-Term): If you have short-term debts like credit card balances or personal loans with high interest rates, a portion of this 70% might be allocated to making minimum payments or slightly more to chip away at them, preventing them from snowballing. However, the 20% category is ideally where aggressive debt reduction takes place.

The Tech Integration: In today’s digital age, technology plays a crucial role in managing the 70% segment effectively.

- Budgeting Apps: Tools like Mint, YNAB (You Need A Budget), or PocketGuard can automate expense tracking, categorize your spending, and provide real-time insights into where your money is going. This transparency is vital for identifying areas where you might be overspending and making informed adjustments.

- Digital Bill Payments: Automating bill payments through your bank or service providers ensures you never miss a deadline and avoid late fees, which eat into your 70% allocation.

- Smart Shopping: Leveraging price comparison websites, browser extensions that find coupons, and subscription management tools can help you optimize your spending on essentials and discretionary items. For instance, subscription cancellation apps can identify unused services that are draining your budget.

- Digital Entertainment: While enjoyable, streaming services, online gaming subscriptions, and digital book purchases fall under discretionary spending. Technology allows for a vast array of options, but mindful consumption is key to staying within your allocated budget.

The Brand Connection: Your brand, both personal and corporate, can indirectly influence your 70% spending. If you have a strong personal brand that opens doors to higher-paying opportunities, you might find yourself with more disposable income. Conversely, maintaining a certain lifestyle associated with your brand might lead to higher discretionary spending. Understanding the perceived value of your brand can help you make conscious decisions about your spending habits.

The 20% for Security: Savings, Debt Reduction, and Financial Cushioning

The 20% allocation is a critical component for building financial resilience and moving towards long-term financial freedom. This segment is primarily focused on addressing your immediate financial obligations and building a safety net.

- Aggressive Debt Reduction: This is the ideal place to funnel extra funds towards paying down high-interest debt, such as credit cards, personal loans, or even extra payments on a mortgage or student loans. Prioritizing debt with the highest interest rates (the “debt avalanche” method) can save you a significant amount of money over time.

- Building an Emergency Fund: Life is unpredictable. An emergency fund is a crucial safety net for unexpected events like job loss, medical emergencies, or major home/car repairs. The general recommendation is to have 3-6 months of living expenses saved. This fund should be easily accessible but kept separate from your everyday checking account.

- Short- to Medium-Term Savings Goals: This could include saving for a down payment on a house, a new car, a significant vacation, or further education. These are goals that you aim to achieve within the next 1-5 years.

The Tech Integration: Technology significantly streamlines the process of managing this 20% segment.

- High-Yield Savings Accounts (HYSAs): These online accounts offer significantly higher interest rates than traditional brick-and-mortar bank accounts, allowing your emergency fund and short-term savings to grow faster.

- Debt Payoff Calculators: Numerous online tools and apps can help you strategize your debt repayment. They can calculate how long it will take to become debt-free based on different payment amounts and demonstrate the interest savings you’ll achieve.

- Automated Transfers: Set up automatic transfers from your checking account to your savings or debt repayment accounts on payday. This “pay yourself first” approach ensures that these crucial allocations are made before you have a chance to spend them.

- Investment Platforms for Short-Term Goals: While the 10% is for long-term investments, some platforms offer low-risk, short-term investment options for goals within the next few years, such as money market funds or short-term bond funds.

The Brand Connection: A strong personal or corporate brand can indirectly influence your ability to allocate funds to this 20% category. If your brand is associated with financial responsibility and discipline, it can motivate you to prioritize debt reduction and savings. Furthermore, a positive brand image can sometimes lead to better loan terms or financial opportunities that expedite debt payoff.

The 10% for Growth: Long-Term Investing and Wealth Building

The final 10% is where the magic of compounding truly takes hold, focusing on building long-term wealth and achieving financial independence. This is not about short-term gains but about strategic allocation for future security.

- Retirement Accounts: This is the primary focus for many. Contributions to 401(k)s, IRAs (Traditional and Roth), or similar retirement plans are crucial for ensuring a comfortable future. Employer matching contributions in 401(k)s are essentially “free money” and should be a top priority.

- Taxable Investment Accounts: Once retirement accounts are adequately funded, this 10% can be invested in taxable brokerage accounts in a diversified portfolio of stocks, bonds, ETFs (Exchange Traded Funds), or mutual funds.

- Alternative Investments: Depending on your risk tolerance and financial knowledge, this segment might also include allocations to real estate (e.g., REITs or direct ownership), peer-to-peer lending, or other alternative investment vehicles.

- Entrepreneurial Ventures/Side Hustles: While “Online Income” and “Side Hustles” are listed as a “Money” topic, the initial capital for starting or scaling a business often comes from this long-term growth allocation, especially if the business is viewed as an asset for future wealth creation.

The Tech Integration: Technology is indispensable for effective long-term investing.

- Robo-Advisors: Platforms like Betterment, Wealthfront, or Acorns use algorithms to create and manage diversified investment portfolios based on your risk tolerance and goals. They often have low fees and are a great entry point for new investors.

- Online Brokerages: Major players like Fidelity, Charles Schwab, and Vanguard offer user-friendly platforms for buying and selling stocks, bonds, ETFs, and mutual funds. They provide research tools, educational resources, and often commission-free trading.

- AI-Powered Investment Tools: Emerging AI tools are being developed to analyze market trends, identify investment opportunities, and even personalize investment strategies, offering a glimpse into the future of wealth management.

- Cryptocurrency Exchanges: For those interested in digital assets, secure and reputable cryptocurrency exchanges facilitate the buying and selling of various cryptocurrencies, though this falls into a higher-risk investment category.

The Brand Connection: Your personal brand can significantly impact your ability to invest for the long term. A strong professional brand can lead to career advancement and higher income, allowing you to allocate more than 10% to investments. Conversely, a brand that is perceived as unstable or unreliable might make it harder to secure favorable investment opportunities or loans for entrepreneurial ventures that could boost long-term wealth. Additionally, understanding your personal brand’s financial narrative can inform your investment choices and risk appetite.

Implementing the 70/20/10 Rule: From Theory to Practice

Transitioning from understanding the 70/20/10 rule to actively implementing it requires a systematic approach. It’s not a rigid dogma, but a flexible framework that should be adapted to your unique financial circumstances and goals.

Tailoring the Rule to Your Financial Life

The “perfect” 70/20/10 split is a myth. Your ideal allocation will depend on several factors:

- Income Level: Individuals with higher incomes might find it easier to adhere to the percentages, while those with lower incomes might need to adjust. For instance, someone with very high essential expenses might find their “living” percentage creeping up, requiring them to be extra diligent in the other two categories.

- Debt Load: If you have significant high-interest debt, you might temporarily shift more towards the 20% for aggressive debt repayment, perhaps even reducing the 10% investment portion slightly until that debt is under control.

- Age and Life Stage: Younger individuals with a longer time horizon until retirement can afford to take on more investment risk in their 10% allocation. Older individuals closer to retirement might shift towards more conservative investments.

- Financial Goals: Are you saving for a down payment in two years or planning for early retirement in twenty? Your specific goals will dictate the urgency and nature of your savings and investment strategies.

Practical Steps for Implementation:

- Track Your Spending Meticulously: Use budgeting apps or spreadsheets to understand exactly where your money is going. Identify your fixed and variable expenses.

- Calculate Your Net Income: This is the money you have left after taxes and other deductions. This is the figure you’ll be working with.

- Set Clear Financial Goals: Define what you want to achieve with your 20% (e.g., debt-free by X date, $10,000 emergency fund) and 10% (e.g., retirement savings target, down payment for a rental property).

- Automate Your Allocations: Set up automatic transfers to your savings, investment, and debt repayment accounts on payday. This is arguably the most critical step for consistent progress.

- Regularly Review and Adjust: Your financial situation will change. Review your budget and allocations at least quarterly, or whenever a significant life event occurs (e.g., a pay raise, a new job, a marriage).

Leveraging Technology and Brand for Enhanced Financial Outcomes

The integration of technology and a strong understanding of your brand can transform the 70/20/10 rule from a mere guideline into a powerful engine for financial growth.

- Smart Budgeting and Financial Planning Software: Beyond basic tracking, advanced tools can offer predictive analytics, scenario planning, and personalized recommendations, helping you optimize every dollar.

- Digital Investment Platforms and AI: As mentioned earlier, robo-advisors and AI-driven investment tools democratize sophisticated portfolio management, making it accessible to a wider audience.

- Online Financial Education: Numerous reputable websites, courses, and podcasts offer free or affordable education on personal finance, investing, and wealth building, empowering you to make informed decisions.

- Personal Branding for Financial Advancement: Cultivating a strong professional brand can lead to career opportunities, higher earning potential, and better negotiation power. This directly impacts your ability to allocate more resources to your 20% and 10% categories.

- Corporate Brand and Financial Stability: For businesses, a strong corporate brand can attract investment, facilitate loans, and create a stable financial environment that trickles down to employee financial well-being.

The Long-Term Vision: Financial Freedom Through Balanced Allocation

The true power of the 70/20/10 rule lies in its ability to foster a balanced approach to your financial life. It acknowledges the importance of enjoying your present while diligently preparing for your future.

- Avoiding Lifestyle Creep: By having a defined allocation for spending, you’re less likely to fall victim to “lifestyle creep” – the tendency to increase spending as your income rises.

- Building Sustainable Wealth: The consistent application of the 10% investment rule, combined with the reduction of debt in the 20% category, creates a powerful compounding effect that leads to significant wealth accumulation over time.

- Achieving Financial Goals: Whether it’s early retirement, financial independence, or the ability to support your family comfortably, this rule provides a clear roadmap to achieving your aspirations.

- Mental Peace and Security: Knowing that you have a plan in place for your present needs, future security, and long-term growth provides immense peace of mind and reduces financial stress.

In conclusion, the 70/20/10 rule for money is more than just a numerical formula; it’s a philosophy of financial stewardship. By understanding its core components, leveraging the power of technology and strategic branding, and committing to disciplined implementation, you can unlock a path towards sustainable financial success, allowing you to live a fulfilling life today while building a secure and prosperous tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.