In the intricate world of personal and business finance, terms like “interest rate” and “APR” are thrown around constantly. While often used interchangeably in casual conversation, these two financial metrics represent distinct concepts, each playing a critical role in determining the true cost of borrowing money or the return on an investment. Misunderstanding their differences can lead to significant financial missteps, ranging from overpaying on a loan to miscalculating investment returns.

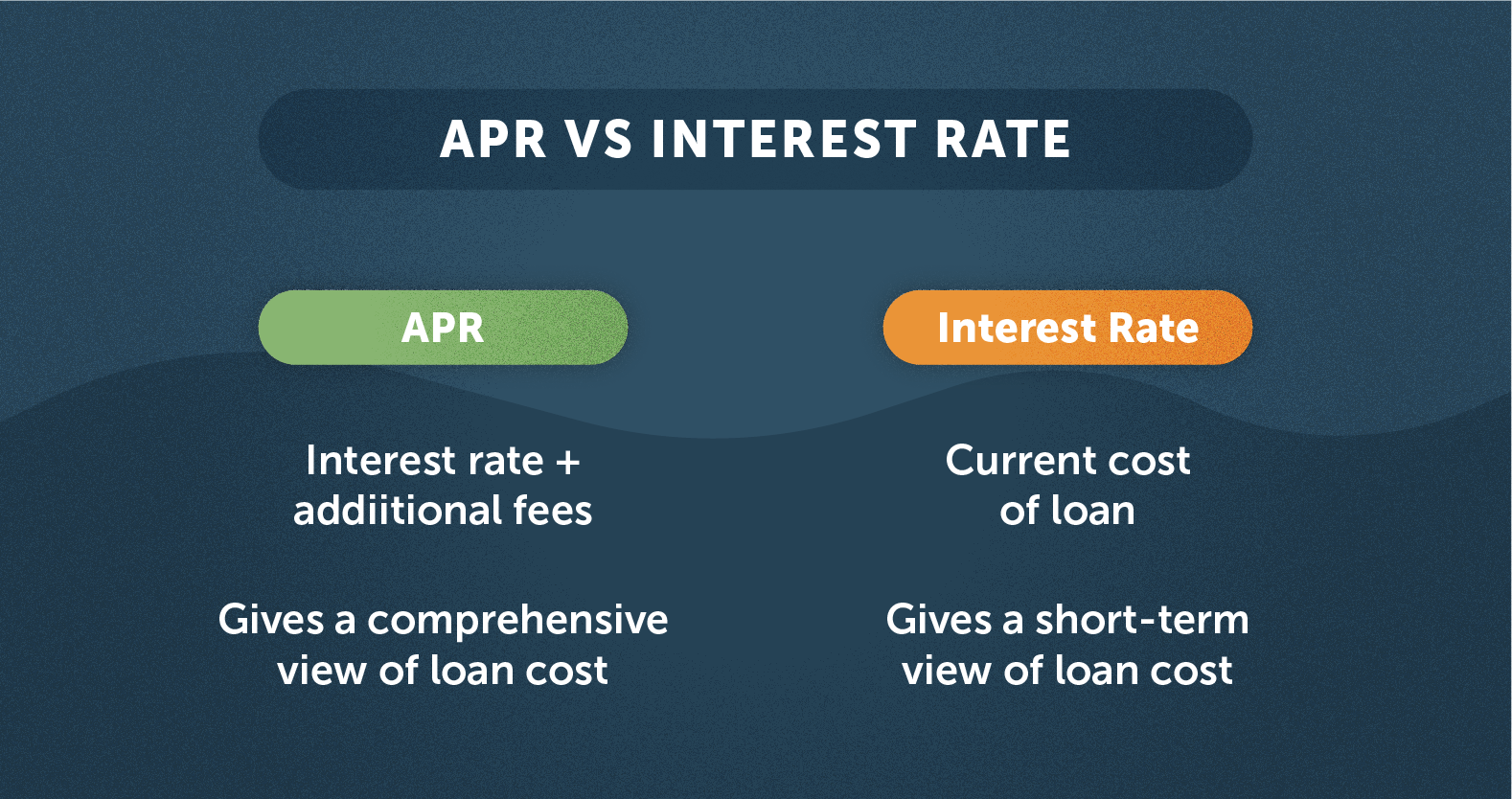

At its core, an interest rate is simply the percentage charged by a lender for the use of their money. It’s the base cost of borrowing. The Annual Percentage Rate (APR), however, offers a more comprehensive view. It encompasses not only the interest rate but also other fees and costs associated with a loan, expressed as an annualized percentage. Think of the interest rate as the price of the principal, and the APR as the overall price tag, including various hidden charges.

This distinction is not merely academic; it has profound practical implications for consumers taking out mortgages, auto loans, or credit cards, as well as for businesses seeking capital. By unraveling the nuances between interest rates and APRs, individuals and organizations can make more informed, cost-effective financial decisions. This article will delve into each term, highlight their key differences, and explain why understanding both is paramount for sound financial literacy and strategic planning.

Understanding the Basic Interest Rate

The interest rate is arguably the most fundamental concept in finance, serving as the cornerstone for virtually all lending and borrowing activities. It’s the “rent” you pay for using someone else’s money, or the “income” you earn for letting someone use yours.

Definition and Calculation

An interest rate is expressed as a percentage of the principal amount – the initial sum borrowed or invested. It represents the cost of borrowing or the yield on an investment, usually calculated over a specific period, typically annually.

For instance, if you borrow $10,000 at a 5% annual interest rate, you would owe $500 in interest for that year, assuming simple interest and no compounding. The calculation is straightforward: Principal × Interest Rate.

While simple interest is easy to understand, most real-world financial products involve compound interest. This means that interest is not only calculated on the initial principal but also on the accumulated interest from previous periods. This “interest on interest” effect can significantly increase the total amount paid or earned over time, making it a powerful force in finance, whether for debt growth or wealth accumulation.

Types of Interest Rates

Interest rates come in various forms, each with its own characteristics:

- Fixed Interest Rate: This rate remains constant throughout the life of the loan or investment. It provides predictability in payments, making budgeting easier. Mortgages, for example, often come with fixed interest rates for a set period or the entire loan term.

- Variable (or Adjustable) Interest Rate: This rate can change over time, typically tied to a benchmark index (like the prime rate or LIBOR/SOFR). While variable rates can offer lower initial payments, they expose borrowers to the risk of higher payments if market rates rise.

- Nominal Interest Rate: This is the stated or advertised interest rate on a loan or investment, without taking inflation into account. It’s the rate you typically see quoted.

- Real Interest Rate: This rate adjusts the nominal rate for inflation, providing a more accurate measure of the true cost of borrowing or the real return on an investment. It’s calculated as

Nominal Interest Rate - Inflation Rate. While important for economic analysis, for the purpose of comparing loan offers, the nominal rate is usually the primary focus.

Where You Encounter Interest Rates

Interest rates are ubiquitous in finance:

- Loans: Mortgages, car loans, personal loans, student loans – all have an interest rate dictating the core cost of borrowing.

- Savings Accounts & Certificates of Deposit (CDs): These accounts offer an interest rate as a return for depositing your money.

- Bonds: The coupon rate on a bond is essentially its interest rate, indicating the periodic payment the bondholder will receive.

- Credit Cards: While often advertised with APR, the underlying mechanism involves an interest rate applied to outstanding balances.

In essence, the interest rate is the foundational price tag for financial capital. However, it rarely tells the whole story of a loan’s total cost.

Demystifying the Annual Percentage Rate (APR)

While the interest rate provides a direct measure of the cost of borrowing the principal, the Annual Percentage Rate (APR) offers a more holistic and transparent picture of a loan’s total annual cost. It’s designed to give consumers a single, standardized metric to compare different loan offers, taking into account not just the interest, but also other mandatory fees.

Definition and Purpose

The Annual Percentage Rate (APR) is the true annual cost of a loan, expressed as a percentage. It represents the total cost of credit over the full term of the loan, including the nominal interest rate and any additional charges or fees imposed by the lender.

The concept of APR was largely formalized by the U.S. Truth in Lending Act (TILA) in 1968. Before TILA, lenders could advertise attractive low interest rates while tacking on various hidden fees, making it difficult for consumers to understand the actual cost of borrowing. TILA mandated that lenders disclose the APR, aiming to provide consumers with a standardized figure that incorporates all significant costs, thus enabling easier comparison shopping.

Components of APR

The core difference between the interest rate and APR lies in what components are included in their calculation. The APR includes:

- The Interest Rate: This is the primary component and often the largest portion of the APR.

- Loan Origination Fees: Charges for processing a new loan application.

- Discount Points (or Mortgage Points): Fees paid upfront to the lender in exchange for a lower interest rate over the life of the loan. Each point typically costs 1% of the loan amount.

- Brokerage Fees: Payments made to a mortgage broker or loan officer for their services.

- Underwriting Fees: Costs associated with evaluating and approving a loan application.

- Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premiums: If required, these annual insurance premiums can be factored into the APR for certain loans.

- Some Closing Costs: While not all closing costs are included, those that are considered a cost of obtaining the credit (e.g., certain processing fees, document preparation fees) are typically part of the APR calculation. Costs like appraisal fees, title insurance, and recording fees are generally excluded because they are services related to the property itself, not directly to the cost of the credit.

By bundling these additional costs with the interest rate and spreading them over the loan’s term, the APR provides a single, comparative annual percentage that reflects the true expense of borrowing.

How APR is Calculated

The exact calculation of APR can be complex, involving actuarial methods to amortize all included fees over the life of the loan. In essence, it calculates the effective interest rate that would yield the same total cost (interest + fees) as the loan’s stated interest rate plus all included fees. The formula aims to determine a rate that, if applied solely as interest to the principal, would result in the same total payments (principal, interest, and fees) as the actual loan.

A crucial aspect of APR calculation is that it takes into account the compounding frequency of the interest. If interest is compounded more frequently (e.g., daily or monthly instead of annually), the effective cost of borrowing increases. APR aims to capture this effect, making it a more accurate representation of the annual cost than a simple nominal interest rate.

Where You Encounter APR

APR is prominently disclosed for various credit products:

- Credit Cards: Credit card statements universally display the APR for purchases, cash advances, and balance transfers. Often, different types of transactions may have different APRs.

- Mortgages: Lenders are legally required to provide the APR for mortgage loans. This is particularly important because mortgage loans often involve significant origination fees and points.

- Auto Loans: Car dealerships and lenders provide APRs for vehicle financing, helping buyers compare different financing options.

- Personal Loans: Unsecured personal loans also come with an APR disclosure, allowing consumers to gauge the total cost.

For any credit product, the APR is typically the most critical figure for making apples-to-apples comparisons between different lenders.

Key Distinctions and Why They Matter

While both interest rate and APR are percentages related to the cost of borrowing, their fundamental differences are crucial for informed financial decision-making.

Scope of Costs Included

The most significant differentiator is the scope of costs included:

- Interest Rate: Represents only the percentage charged on the principal amount borrowed. It’s the core cost of the money itself.

- APR: Represents the total annualized cost of borrowing, encompassing the interest rate plus mandatory fees and charges directly associated with obtaining the credit.

This distinction means that a loan with a lower nominal interest rate might actually have a higher APR than a loan with a slightly higher interest rate if the former has significantly more upfront fees.

The “True Cost” of Borrowing

APR provides a much more accurate representation of the “true cost” of borrowing for the consumer. When comparing loan offers, looking solely at the interest rate can be misleading. A lender might advertise a very attractive low interest rate, but if they impose substantial origination fees, processing fees, or discount points, the actual cost of that loan will be higher than implied by the interest rate alone. The APR consolidates these additional expenses into a single, digestible percentage, allowing borrowers to understand the full financial commitment.

For instance, consider two loan offers for $100,000 over 30 years:

- Loan A: 4.0% interest rate, $3,000 in fees.

- Loan B: 4.2% interest rate, $500 in fees.

On the surface, Loan A seems better due to its lower interest rate. However, once the fees are factored into the APR calculation, Loan A’s APR might be 4.25%, while Loan B’s APR might be 4.22%. In this scenario, Loan B, despite a slightly higher nominal interest rate, is actually the cheaper option when considering the total cost over the loan’s life.

Impact of Compounding

While a nominal interest rate might be quoted as an annual figure, the actual interest could be compounded more frequently (e.g., monthly). The APR implicitly accounts for this compounding effect, providing an effective annual rate that reflects the true cost or return over a year, considering all compounding periods. This makes the APR a more robust metric for comparing financial products that have different compounding frequencies.

Regulatory Mandates

In many jurisdictions, including the United States, the disclosure of APR is a legal requirement for various consumer loans under regulations like the Truth in Lending Act (TILA). This mandate ensures transparency and consumer protection, compelling lenders to present the full cost of credit in a standardized format. While interest rates are also disclosed, the emphasis on APR highlights its importance as the primary comparative metric.

Practical Implications for Consumers and Businesses

Understanding the difference between APR and interest rate is not merely an academic exercise; it has tangible implications for making sound financial decisions for both individuals and organizations.

Choosing the Right Loan

For consumers, the most direct benefit of understanding APR is in loan comparison. When shopping for a mortgage, auto loan, or personal loan, always prioritize comparing the APRs of different offers, not just the interest rates. A lower interest rate can be deceptive if it comes with hefty upfront fees that drive up the APR. By focusing on APR, you ensure you’re comparing the total cost of borrowing, making it easier to identify the truly cheapest option.

Furthermore, consider the term of the loan. For shorter-term loans, upfront fees might have a proportionally greater impact on the APR. For longer-term loans, the interest rate component typically outweighs the upfront fees.

Understanding Credit Card Costs

Credit cards are notorious for having multiple APRs (e.g., purchase APR, cash advance APR, penalty APR). The APR on a credit card reflects the annualized interest rate charged on your outstanding balance, taking into account the daily compounding of interest. It’s critical to understand that if you carry a balance, the APR will dictate how quickly your debt can grow. Always strive to pay off your credit card balance in full each month to avoid incurring any interest or APR charges. If you can’t, understanding the APR helps you calculate the true cost of carrying that debt.

Investment Decisions

While the term “APR” is primarily associated with the cost of borrowing, the underlying concept of an “effective annual rate” (which APR essentially is for loans) is crucial for investment decisions. When evaluating different investment opportunities, particularly those with varying compounding frequencies or fee structures, understanding the effective annual return (EAR) helps you compare them accurately. An investment with a 5% nominal annual rate compounded daily will yield a higher EAR than one with a 5% nominal rate compounded annually. Though not called APR, the principle of factoring in compounding and fees to arrive at a true annual percentage applies.

Business Lending

Businesses frequently seek loans for expansion, working capital, or asset acquisition. Just like consumers, businesses must scrutinize both the interest rate and the APR (or equivalent total cost analysis) when evaluating financing options. Large corporate loans can involve significant arrangement fees, commitment fees, and other charges. Ignoring these and focusing solely on the nominal interest rate can lead to underestimating the true cost of capital, impacting profitability and financial planning. Sophisticated financial modeling often incorporates all these costs to determine the effective cost of borrowing for strategic decision-making.

Conclusion

The distinction between an interest rate and an Annual Percentage Rate (APR) is fundamental to financial literacy and prudent financial management. While the interest rate represents the basic cost of borrowing the principal amount, the APR provides a more comprehensive and accurate picture by incorporating all mandatory fees and charges associated with a loan, annualized into a single percentage.

Understanding this difference empowers consumers to make truly informed decisions when taking out mortgages, auto loans, credit cards, and personal loans, ensuring they compare the total cost of credit rather than being swayed by superficially low interest rates. For businesses, this knowledge is critical for accurately assessing the cost of capital and making strategic financing choices.

In an increasingly complex financial landscape, always look beyond the initial interest rate. Demand the APR, scrutinize all disclosures, and ensure you fully comprehend the true cost of any financial product. This diligence will undoubtedly lead to smarter borrowing, more effective saving, and greater overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.