The Federal funds rate is perhaps the most influential tool in the global financial landscape. Often referred to simply as “the Fed rate,” it serves as the benchmark for the cost of borrowing money across the United States and, by extension, affects international markets. Whether you are a first-time homebuyer, a seasoned stock market investor, or a small business owner, the current Fed rate dictates the rhythm of your financial life. Understanding how this rate is determined, why it fluctuates, and how it impacts your wallet is essential for navigating the modern economic environment.

Understanding the Federal Funds Rate and Its Mechanics

To understand the current Fed rate, one must first understand what it actually represents. The federal funds rate is the interest rate at which commercial banks and credit unions lend their excess reserves to each other overnight. While it might sound like a niche banking technicality, it is the lever that the Federal Reserve pulls to control the supply of money in the economy.

What is the Fed Rate?

The federal funds rate is set by the Federal Open Market Committee (FOMC), a branch of the Federal Reserve System. Unlike the interest rate on your car loan, which is set by a private lender, the Fed rate is a “target range.” For instance, if the FOMC sets a target range of 5.25% to 5.50%, they are signaling to the banking system that they want the cost of short-term borrowing to stay within those bounds. When banks have to pay more to borrow from each other, they pass those costs on to consumers and businesses in the form of higher interest rates on loans.

How the FOMC Decides

The FOMC meets eight times a year to assess the health of the U.S. economy. Their decisions are guided by a “dual mandate” assigned by Congress: to promote maximum employment and maintain stable prices (which they define as a 2% annual inflation rate). If inflation is running too high, the Fed raises rates to “cool” the economy by making borrowing more expensive. If the economy is sluggish or unemployment is rising, they may lower rates to encourage spending and investment.

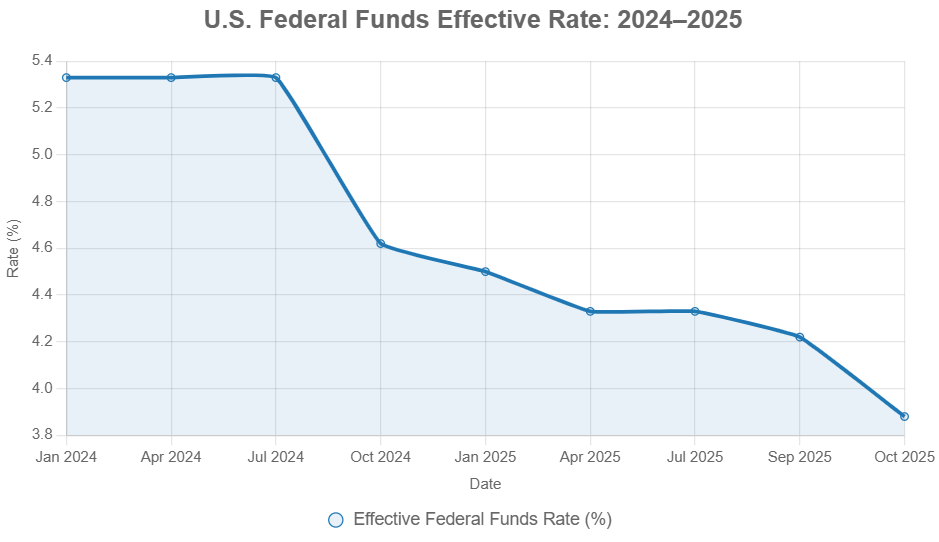

The Target Range vs. The Effective Rate

While the FOMC sets a target range, the “Effective Federal Funds Rate” (EFFR) is the actual volume-weighted median of the rates at which these overnight transactions occur. The Federal Reserve uses “open market operations”—buying or selling government securities—to ensure the market rate stays within their desired target range. This subtle dance ensures that the central bank maintains grip over the liquidity of the financial system.

Why the Current Fed Rate Matters for Your Personal Finances

The ripple effects of a change in the Fed rate are felt almost immediately in personal finance. Because the “Prime Rate”—the base rate that banks charge their most creditworthy corporate customers—is directly tied to the Fed rate, consumer lending products react in lockstep.

The Impact on Mortgages and Home Loans

For many Americans, the most significant impact of the current Fed rate is felt in the housing market. While the Fed does not directly set mortgage rates, the 30-year fixed mortgage rate tends to track the yield on the 10-year Treasury note, which is heavily influenced by Fed policy. When the Fed rate is high, mortgage rates climb, significantly increasing the monthly payment for new buyers and reducing their overall purchasing power. Conversely, a low-rate environment often triggers a refinancing boom, allowing homeowners to lower their monthly expenses.

Credit Cards and Consumer Debt

Most credit cards have variable interest rates tied to the Prime Rate. This means that every time the Fed raises the federal funds rate by 25 or 50 basis points, your credit card’s Annual Percentage Rate (APR) likely increases by the same amount within one or two billing cycles. In a high-rate environment, carrying a balance becomes exponentially more expensive, making debt repayment strategies like the “avalanche method” more critical than ever for maintaining financial health.

High-Yield Savings Accounts and Certificates of Deposit (CDs)

It isn’t all bad news when the Fed rate rises. For savers, a higher Fed rate is a boon. Banks begin to compete for consumer deposits by offering higher yields on savings accounts, money market funds, and Certificates of Deposit (CDs). After years of near-zero interest, a federal funds rate above 5% allows conservative investors to earn a meaningful return on their cash without taking on the volatility of the stock market.

The Influence of Monetary Policy on the Investment Landscape

The Federal Reserve’s stance on interest rates is the primary driver of market sentiment. Wall Street hangs on every word of the Fed Chair’s press conferences, looking for “dovish” signals (indicating lower rates) or “hawkish” signals (indicating higher rates).

Stock Market Volatility and Sector Performance

Generally speaking, rising interest rates are a headwind for the stock market. When rates go up, the “discount rate” used by analysts to value future earnings also goes up, which typically leads to lower stock valuations—especially for high-growth tech companies that rely on future profits. Furthermore, higher rates increase interest expenses for companies with significant debt, eating into their bottom line. However, certain sectors, like Financials (banks), often benefit from higher rates as they can widen their net interest margins.

Fixed Income and the Bond Market

The relationship between interest rates and bond prices is inverse: when the Fed rate goes up, bond prices go down. This is because new bonds are issued with higher yields, making existing bonds with lower rates less attractive to investors. However, for those looking to enter the market, a high-rate environment offers the best yields seen in decades, allowing investors to lock in steady income through Treasury bonds or high-quality corporate debt.

Real Estate Investment Trusts (REITs)

REITs are particularly sensitive to the Fed rate. Since REITs often use debt to acquire property portfolios, higher interest rates increase their cost of capital. Additionally, because REITs are often viewed as income-producing assets similar to bonds, they must offer higher yields to remain competitive when “risk-free” Treasury rates rise. This often leads to price volatility in the real estate sector during periods of aggressive Fed tightening.

Economic Indicators Driving the Fed’s Decisions

The Fed does not operate in a vacuum. Their decisions regarding the current rate are “data-dependent,” meaning they react to specific economic signals to determine if they should hike, hold, or cut.

Taming Inflation: The 2% Target

Inflation is the Fed’s Public Enemy Number One. The Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index are the primary metrics the FOMC watches. If these metrics show that prices for goods and services are rising faster than 2% annually, the Fed is likely to keep rates high or raise them further to dampen demand. The goal is a “soft landing”—bringing inflation down without triggering a severe recession.

Employment Data and Labor Market Strength

The other half of the dual mandate is employment. The Fed monitors monthly jobs reports, including the unemployment rate and wage growth. A labor market that is “too hot”—characterized by massive job openings and rapidly rising wages—can actually worry the Fed, as it can lead to a “wage-price spiral” that fuels further inflation. If the labor market begins to crack and unemployment rises significantly, the Fed may be forced to cut rates to stimulate job creation.

GDP Growth and Recessionary Fears

Gross Domestic Product (GDP) represents the total value of all goods and services produced. The Fed aims for steady, sustainable growth. If GDP growth is too robust, the economy risks overheating. If GDP contracts for two consecutive quarters, it is often viewed as a technical recession. The current Fed rate is always a balancing act: high enough to stop inflation, but low enough to avoid a total economic shutdown.

Strategic Financial Planning in a High-Rate Environment

When the Fed rate is elevated, the “free money” era ends, and financial strategy must shift from growth-at-all-costs to capital preservation and efficiency.

Debt Management Strategies

In a high-rate environment, the priority should be eliminating high-interest variable debt. If you have a Home Equity Line of Credit (HELOC) or a variable-rate personal loan, consider whether you can consolidate that debt into a fixed-rate loan before rates climb further. For businesses, this is a time to deleverage and focus on cash flow rather than taking on new, expensive debt for expansion.

Optimizing Your Investment Portfolio

Investors should look at their “asset allocation” through the lens of the current rate. With cash and short-term Treasuries offering competitive yields, the “TINA” (There Is No Alternative to stocks) era is over. Diversification now includes a more robust role for fixed income. Additionally, investors may look for “value” stocks—companies with strong balance sheets and consistent cash flows—which tend to be more resilient during periods of high interest rates than speculative “growth” stocks.

Preparing for Potential Rate Cuts

Financial markets are forward-looking. Even when the current Fed rate is high, investors are already betting on when the first rate cut will occur. For consumers, this means being ready to act. If you are waiting to buy a home, keeping your credit score high is vital so you can pounce on a lower rate the moment the Fed pivots. For investors, a shift toward “duration”—locking in long-term bond yields now—can provide significant capital gains if market rates drop in the future.

The current Fed rate is more than just a number; it is the heartbeat of the economy. By understanding the mechanisms behind it and the signals the Federal Reserve is watching, individuals and businesses can make informed decisions that protect their wealth and capitalize on the shifting financial tides. Whether rates are rising, falling, or holding steady, a proactive approach to your personal and business finances is the best way to ensure long-term stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.