Refinancing a mortgage is often touted as one of the smartest financial moves a homeowner can make. Whether the goal is to capitalize on lower interest rates, shorten a loan term, or tap into home equity for major expenses, the potential for long-term savings is significant. However, many homeowners are caught off guard by the upfront price tag. Refinancing is not a free transaction; it is, essentially, the process of taking out a brand-new mortgage to pay off your existing one.

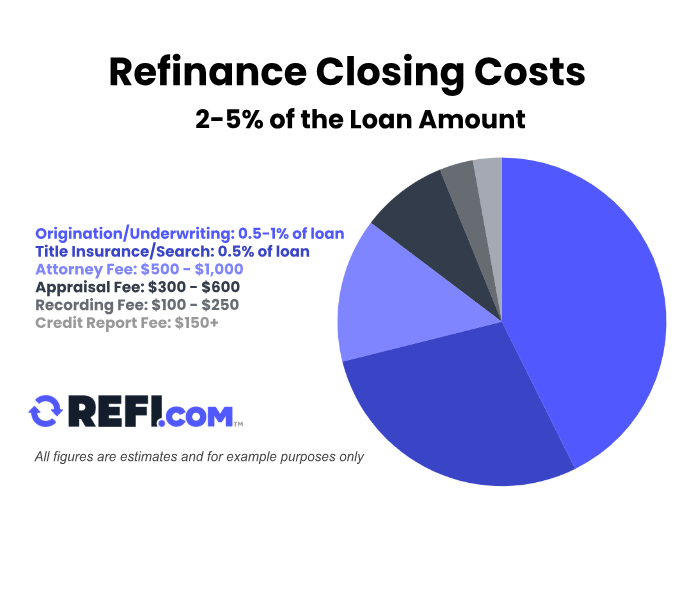

Understanding the “how much” behind refinancing requires a deep dive into closing costs, lender fees, and third-party charges. Typically, a refinance will cost between 2% and 5% of the total loan amount. On a $300,000 mortgage, that equates to an investment of $6,000 to $15,000. To determine if the move makes financial sense, you must look beyond the monthly savings and analyze the total cost of the transition.

1. Breaking Down the Primary Closing Costs

The bulk of the expense in a refinance comes from closing costs. These are the administrative and legal fees required to process the loan, evaluate the property, and ensure the lender is protected against future claims. While these fees vary by state and lender, they generally fall into three specific buckets.

Application and Appraisal Fees

The moment you decide to move forward, most lenders will charge an application fee. This covers the initial administrative work of processing your request and pulling your credit reports. While some lenders waive this to attract business, it can range from $100 to $500.

Following the application, the lender will require a professional appraisal. Even if you bought your home recently, the lender needs a current valuation to determine the Loan-to-Value (LTV) ratio. This ensures the home is worth enough to secure the new debt. A standard residential appraisal typically costs between $300 and $600, though unique properties or high-demand markets can drive this price higher.

Origination and Underwriting Charges

The origination fee is often the largest single line item on your closing disclosure. This is what the lender charges for “doing the loan.” It is frequently calculated as a percentage of the loan amount—usually around 0.5% to 1%. On a $400,000 loan, a 1% origination fee adds $4,000 to your costs.

Underwriting fees are also common. This covers the cost of the lender’s internal team verifying your income, employment, assets, and debt-to-income ratio. Think of this as the “due diligence” fee that ensures you meet the risk profile for the new interest rate.

Title Search and Insurance

Lenders must ensure that the title to your property is “clear”—meaning no one else has a legal claim to it, such as a contractor with an unpaid lien or a long-lost heir. A title company will perform a search of public records, which usually costs a few hundred dollars.

Furthermore, you will be required to purchase a new lender’s title insurance policy. Even though you bought title insurance when you first purchased the home, that policy only protects the original lender. When you refinance, the new lender requires their own protection. Depending on your location, this can cost anywhere from $500 to $2,000.

2. Navigating Variable Expenses and Hidden Fees

Beyond the standard administrative costs, there are several “variable” expenses that depend on your specific financial choices and the laws of your state. These can drastically change the total amount you need to bring to the closing table.

Mortgage Discount Points

One of the most common ways to lower an interest rate during a refinance is to buy “points.” One point is equal to 1% of the loan amount. By paying this fee upfront, you effectively “pre-pay” some of the interest in exchange for a lower permanent rate.

For a homeowner planning to stay in their house for the next 20 years, buying points can save tens of thousands of dollars. However, it adds a significant upfront cost. If you are refinancing a $500,000 loan and choose to buy two points, you are adding $10,000 to your closing costs immediately. This is a strategic money move that requires a careful calculation of your “break-even” timeline.

Prepayment Penalties and Taxes

Before you refinance, you must check the terms of your current mortgage. Some older or non-conforming loans include a prepayment penalty—a fee charged if you pay off the loan balance early. While these are less common today due to post-2008 regulations, they can still exist in certain “hard money” or subprime products.

Additionally, don’t forget the government’s share. Many local and state governments charge a “recording fee” to update public records with your new mortgage information. Some states also levy a mortgage transfer tax or intangible tax based on the size of the loan. These government-mandated fees are non-negotiable and vary wildly by geography.

Escrow and Pre-Paid Items

Technically, escrow payments aren’t “fees” because the money is yours, but they do require upfront cash. When you refinance, you often have to “seed” a new escrow account for homeowners insurance and property taxes. While you will eventually get a refund of the escrow balance from your old mortgage, there is often a 30-to-60-day lag. This means you may need to provide several thousand dollars at closing to ensure your new tax and insurance accounts are fully funded.

3. Calculating the Break-Even Point: The “Is It Worth It?” Factor

In the world of personal finance, a refinance is only successful if you stay in the home long enough to recoup the costs. This is known as the “break-even point.” If you pay $6,000 to refinance but only save $100 a month, it will take you 60 months (five years) just to get back to zero.

The Break-Even Formula

The math for a refinance is relatively straightforward:

Total Closing Costs ÷ Monthly Savings = Months to Break Even.

For example, if your closing costs are $5,000 and your new monthly payment is $200 less than your old one, your break-even point is 25 months. If you plan to sell the house or move in two years, you would actually lose $200 by refinancing. If you plan to stay for ten years, you would net a profit of $19,000 ($24,000 in total savings minus the $5,000 initial cost).

Factors That Shorten the Timeline

Several factors can make the break-even point arrive faster. The most obvious is a significant drop in interest rates. A rule of thumb used to be that you should wait for a 1% to 2% drop in rates, but in today’s high-balance mortgage environment, even a 0.5% to 0.75% drop can result in massive monthly savings.

Another factor is the elimination of Private Mortgage Insurance (PMI). If your home value has increased significantly since you bought it, a refinance could help you reach 20% equity, allowing you to drop PMI. Removing a $150 monthly PMI payment on top of a lower interest rate can slash your break-even time in half.

4. Strategies to Minimize Refinancing Costs

Just because refinancing is expensive doesn’t mean you have to accept the first quote you receive. Like any major financial transaction, there is room for negotiation and strategic planning.

Shopping Around and Negotiating Fees

Many homeowners make the mistake of only talking to their current lender. However, different institutions—credit unions, national banks, and online lenders—have different “appetites” for risk and different fee structures. By obtaining three to five Loan Estimates, you can compare the “Section A” fees (origination charges).

If Lender A offers a great rate but high fees, and Lender B has lower fees, you can often use Lender B’s estimate to negotiate a fee reduction with Lender A. Remember, many fees, such as the application and processing fees, are set by the lender and can be waived if they want your business badly enough.

The Reality of “No-Closing-Cost” Refinancing

You will often see advertisements for “no-closing-cost” refinances. It is vital to understand that this is a marketing term, not a charitable donation. In a no-closing-cost loan, the lender either:

- Wraps the costs into the total loan balance (meaning you pay interest on your closing costs for 30 years).

- Charges a slightly higher interest rate to cover the costs (often called a “premium-priced” loan).

While this is a great option for homeowners who don’t have $10,000 in cash sitting in a savings account, it usually results in a higher total cost over the life of the loan. From a pure wealth-building perspective, paying the costs upfront is almost always the more profitable choice.

Improving Your Financial Profile Before Applying

The “cost” of your refinance is also tied to your credit score. Lenders use “Loan Level Price Adjustments” (LLPAs). If your credit score is 680, you might pay a higher interest rate or more in discount points than someone with a 760 score.

Spending six months improving your credit score—by paying down credit card balances and ensuring zero late payments—can save you thousands in the refinancing process. Similarly, if you can pay down your mortgage enough to hit a lower LTV bracket (such as 75% instead of 80%), you may qualify for even lower fees and rates.

Conclusion: Making the Final Decision

Refinancing is a powerful tool for optimizing your personal balance sheet, but it requires a disciplined look at the numbers. The cost of refinancing is not just the check you write at closing; it is the opportunity cost of that capital and the time it takes to see a return on your investment.

By meticulously auditing your Loan Estimate, calculating your break-even point, and shopping around for the best combination of rates and fees, you can ensure that your refinance serves its true purpose: building your long-term financial security. In the realm of money management, the goal is never just to lower a monthly payment—it is to increase your net worth over time. Understanding the true cost to refinance is the first step toward achieving that goal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.