The world of personal finance can feel like a maze, especially when you’re navigating the often-confusing landscape of credit cards. While most credit cards operate on trust and your creditworthiness, there’s a specific type that requires an upfront financial commitment: a secured credit card, which necessitates a security deposit. Understanding what this deposit is, why it’s required, and how it functions is crucial for anyone looking to build or rebuild their credit history. This article will demystify the security deposit on a credit card, exploring its purpose, the types of cards it’s associated with, and the benefits of using them.

Understanding the Security Deposit: Your Credit Card’s Safety Net

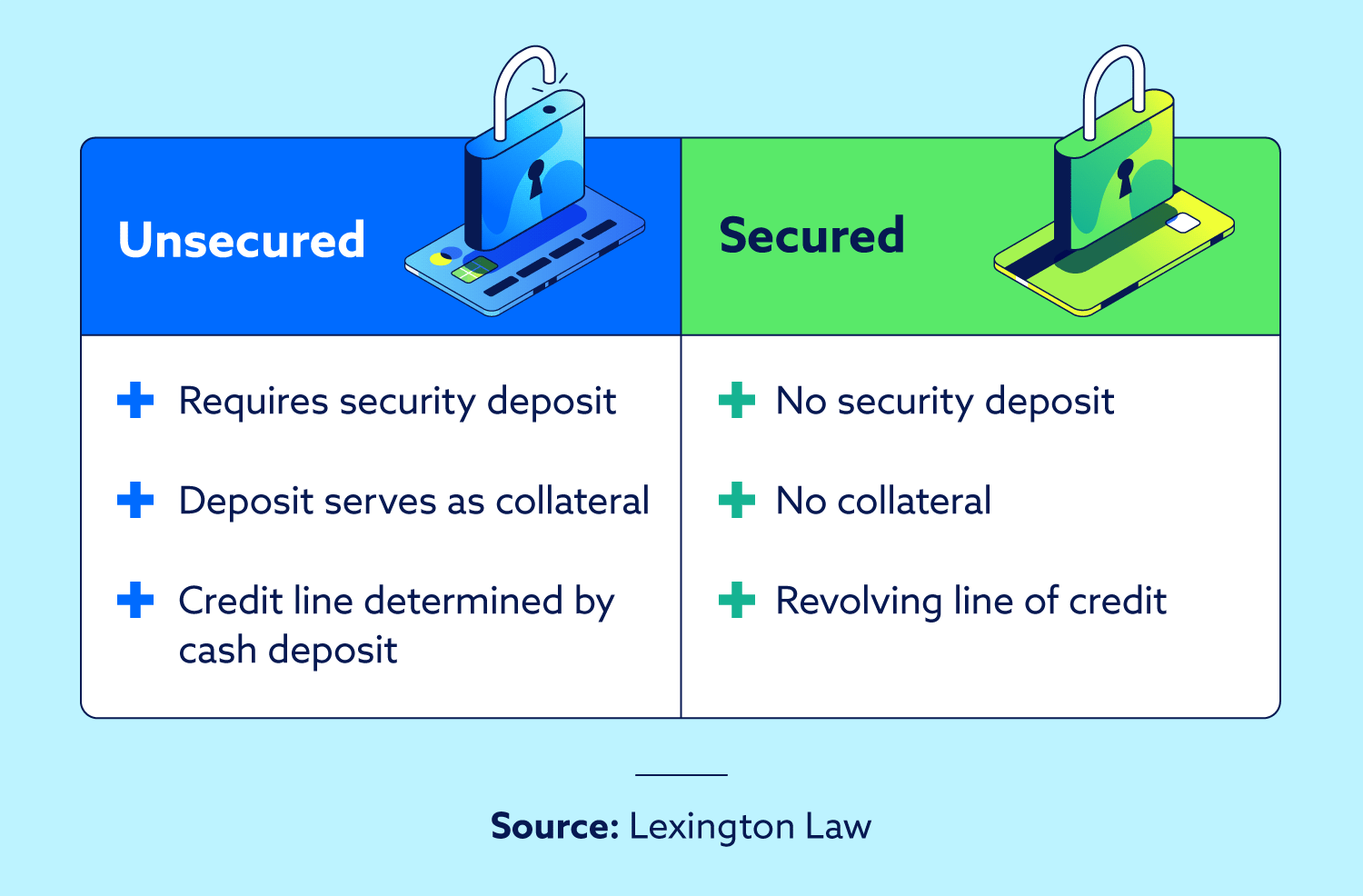

At its core, a security deposit on a credit card serves as a financial safeguard for the credit card issuer. Unlike traditional unsecured credit cards, which are issued based on a consumer’s credit history and perceived ability to repay, secured credit cards are designed for individuals with limited or poor credit. The security deposit acts as collateral, mitigating the risk for the lender.

Why Do Credit Card Companies Ask for a Security Deposit?

The primary reason a credit card company requests a security deposit is to reduce their risk of financial loss. When you apply for an unsecured credit card, the issuer assesses your credit score and financial history to determine if you’re likely to repay borrowed funds. If your credit history is weak or non-existent, this assessment is more difficult, and the risk for the lender increases significantly.

By requiring a security deposit, the issuer has a tangible asset that can be used to cover any outstanding balance if you fail to make payments. This makes the decision to extend credit much less precarious for them, opening the door for individuals who might otherwise be denied a credit card.

How Does the Security Deposit Work?

The security deposit you provide is typically held by the credit card issuer in a separate savings account. It’s not a fee you pay, nor is it an amount that gets applied to your purchases. Instead, it acts as a financial buffer.

- Credit Limit Determination: The most common practice is that your credit limit on a secured credit card will be equal to the amount of your security deposit. For example, if you put down a $300 deposit, your credit limit will likely be $300. Some issuers might offer a slightly higher limit, but it’s usually a 1:1 ratio. This means that the maximum amount you can spend on the card is directly tied to the money you’ve secured.

- No Interest Earned (Usually): In most cases, the security deposit held by the issuer will not earn any interest. This is a trade-off for the opportunity to build credit.

- Reimbursement of the Deposit: The security deposit is refundable. Once you’ve demonstrated responsible credit card usage over a period, the issuer may convert your secured card into an unsecured one and return your deposit. Alternatively, if you decide to close the account, the deposit will be refunded after any outstanding balance is settled.

Who Benefits from a Security Deposit on a Credit Card?

The concept of a security deposit might initially seem like a barrier, but it’s a critical tool for specific groups of individuals aiming to improve their financial standing:

- Individuals with No Credit History: This includes young adults who are just starting their financial journey and have never taken out a loan or credit card before. Without a credit history, lenders have no data to assess their creditworthiness.

- Individuals with Poor Credit Scores: This category encompasses those who have made past financial mistakes, such as missed payments, defaults, or bankruptcies. A secured credit card provides a pathway to demonstrate responsible financial behavior and rebuild a damaged credit score.

- Recent Immigrants: Individuals new to a country might have a limited credit history in their new location, making it difficult to obtain traditional credit. Secured cards offer an accessible entry point.

Types of Credit Cards Requiring a Security Deposit

The term “security deposit on a credit card” is almost exclusively associated with one type of credit product: secured credit cards. While other financial products might involve deposits (like a rental security deposit), the context of a credit card deposit points directly to this specific category.

Secured Credit Cards: Your Gateway to Credit Building

Secured credit cards are the primary and almost exclusive type of credit card that requires a security deposit. They are designed to serve as a stepping stone for individuals who have difficulty qualifying for unsecured credit cards.

- How They Work: You provide an upfront cash deposit to the credit card issuer. This deposit serves as collateral, essentially guaranteeing the credit line. The credit limit is typically equal to the deposit amount.

- Purpose: The main goal of a secured credit card is to help users build or rebuild their credit history. By making timely payments and keeping balances low, users can demonstrate their creditworthiness to lenders.

- Benefits:

- Accessible Credit: They are much easier to get approved for than unsecured cards, even with a low or non-existent credit score.

- Credit Building: Responsible use is reported to credit bureaus, which helps improve your credit score over time.

- Potential for Upgrade: Many issuers will review your account after a period of responsible use (often 6-12 months) and may offer to graduate you to an unsecured card, refunding your deposit.

- Purchase Power: You can use the card for everyday purchases, just like any other credit card.

Other Less Common Scenarios (and why they aren’t typical)

While secured credit cards are the norm, it’s worth briefly touching upon why other credit card types generally don’t require deposits:

- Unsecured Credit Cards: These are the standard credit cards issued based on your creditworthiness alone. No deposit is required because the issuer believes you have the capacity to repay based on your credit profile.

- Prepaid Cards: These are often confused with secured cards, but they function very differently. With a prepaid card, you load money onto it before you can use it. The money you load is not a deposit to guarantee credit; it’s simply the funds you have available to spend. They don’t typically build credit history.

Therefore, when you hear “security deposit on a credit card,” it’s almost certain the discussion is revolving around secured credit cards.

The Journey from Deposit to Unsecured Credit: Building Your Financial Future

The ultimate goal for most users of secured credit cards is to transition to an unsecured credit card. This journey involves responsible financial behavior and demonstrates to the issuer that you are a reliable borrower. The security deposit, in this context, is not just a financial requirement but a catalyst for positive change in your credit profile.

Demonstrating Responsible Credit Usage

The key to moving from a secured to an unsecured credit card lies in consistently demonstrating responsible financial habits. This involves:

- Making On-Time Payments: This is the most critical factor in building credit. Late payments can significantly damage your credit score and hinder your progress. Aim to pay your statement balance in full or at least the minimum payment by the due date every month.

- Keeping Credit Utilization Low: Credit utilization refers to the amount of credit you’re using compared to your total available credit. For secured cards, your credit limit is often equal to your deposit. Ideally, you want to keep your credit utilization below 30%, and even lower (below 10%) is even better for credit score optimization. This means if your credit limit is $300, try not to carry a balance that exceeds $30-$90.

- Regularly Reviewing Your Statements: Keep an eye on your spending and ensure you understand your balance and payment due dates. This helps prevent missed payments and fraudulent activity.

- Avoiding Maxing Out Your Card: Continuously spending up to your credit limit can signal financial distress and negatively impact your credit score.

The Conversion Process: From Secured to Unsecured

Most credit card issuers offer a pathway for secured cardholders to graduate to unsecured accounts. The process typically involves:

- Account Review: After a period of responsible use (usually 6 to 12 months, but this can vary by issuer), the credit card company will review your account history. They will assess your payment behavior, credit utilization, and overall creditworthiness.

- Upgrade Offer: If your performance meets their criteria, they may offer to upgrade your secured card to an unsecured one. This often means your credit limit might increase, and crucially, your security deposit will be refunded.

- New Unsecured Card: In some cases, the issuer might simply close your secured account and issue you a new, unsecured credit card with a different credit limit and terms.

- Deposit Refund: Once the conversion to an unsecured card is complete, the issuer will refund your original security deposit. This is usually done via check or direct deposit.

The Long-Term Benefits of Using Secured Credit Cards

The security deposit, while an initial outlay, unlocks significant long-term financial benefits:

- Establishing a Credit Foundation: For those with no credit history, secured cards are often the only accessible option to begin building a positive credit record.

- Rebuilding Damaged Credit: For individuals who have faced financial setbacks, secured cards offer a practical tool to demonstrate renewed responsibility and repair their credit score. A good track record with a secured card can eventually lead to approval for better credit products.

- Improved Financial Opportunities: A strong credit score opens doors to better interest rates on loans (mortgages, car loans), easier rental approvals, and even better insurance rates. The initial security deposit is a small price to pay for these future advantages.

- Financial Education: Managing a secured credit card forces users to be more mindful of their spending and payment habits, fostering better financial discipline that can be applied across all aspects of their financial lives.

In conclusion, a security deposit on a credit card is a fundamental component of a secured credit card. It’s a financial tool that empowers individuals with limited or damaged credit to access credit, build a positive credit history, and ultimately achieve greater financial freedom. By understanding its purpose and diligently practicing responsible credit management, you can leverage this deposit to unlock a world of improved financial opportunities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.