Auto insurance is an essential part of responsible vehicle ownership, providing a crucial safety net against unexpected financial burdens from accidents. While the concept of insurance itself might seem straightforward – a company agrees to cover your losses in exchange for a premium – the intricacies of your policy can often be a source of confusion. One of the most fundamental, yet often misunderstood, elements of any auto insurance policy is the deductible.

Understanding your deductible is paramount because it directly impacts how much you’ll pay out-of-pocket when you file a claim. It’s not just a random number; it’s a cornerstone of your insurance contract, influencing your premium, your financial planning, and your overall insurance experience. This article will delve deep into the world of auto insurance deductibles, breaking down what they are, how they work, and the critical factors you should consider when choosing one. Whether you’re a seasoned driver or new to the insurance landscape, a solid grasp of deductibles will empower you to make informed decisions and navigate your policy with confidence.

The Core Concept: What Exactly is an Auto Insurance Deductible?

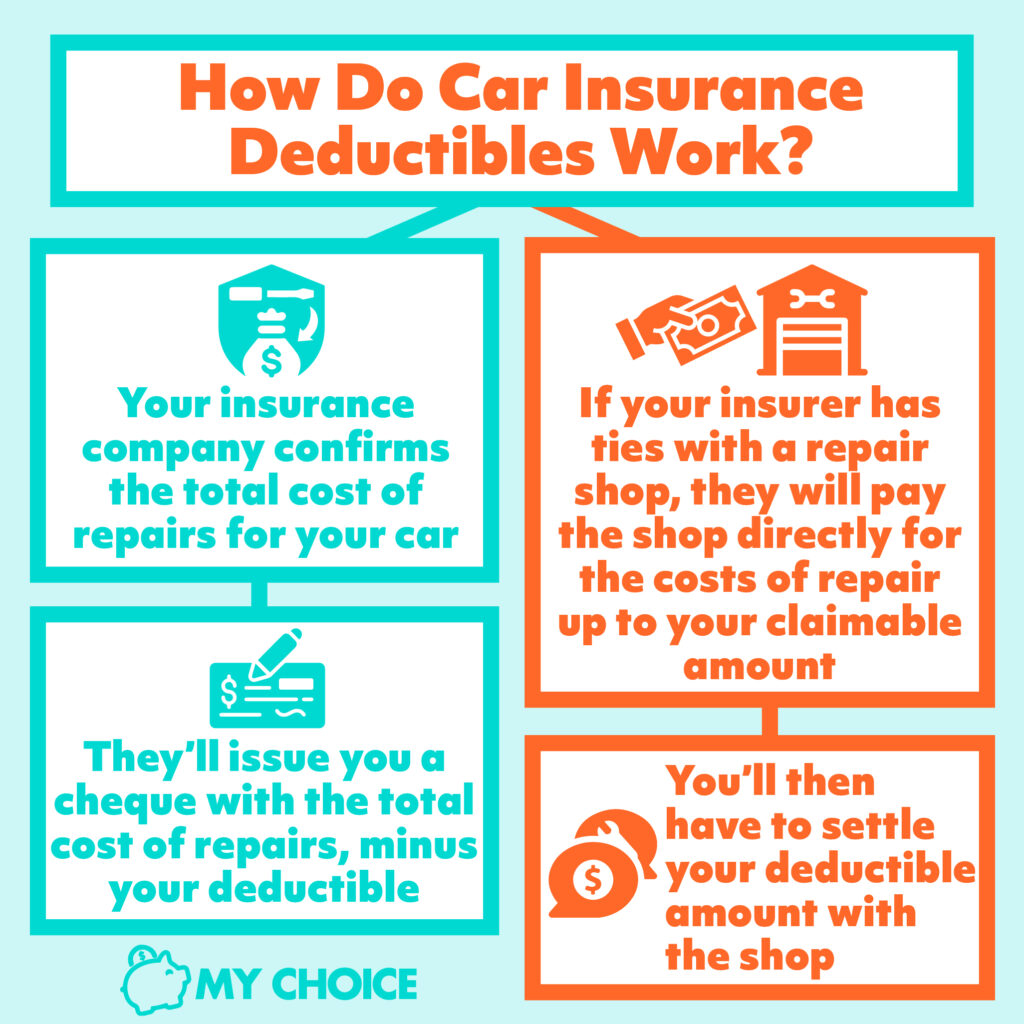

At its heart, an auto insurance deductible is the amount of money you agree to pay out of your own pocket before your insurance company starts paying for a covered claim. Think of it as your initial contribution to the repair or replacement costs after an incident. When you file a claim for damages (whether to your own vehicle or someone else’s, depending on the type of coverage), your deductible is the first portion of that bill that you are responsible for.

Let’s illustrate with a simple example. Suppose you have a comprehensive and collision coverage policy with a $500 deductible, and you get into an accident that causes $3,000 in damage to your car.

- You file a claim: You report the accident to your insurance company.

- Damage assessment: The insurance company assesses the damage and determines the repair cost to be $3,000.

- Deductible application: You will be responsible for paying your $500 deductible.

- Insurance payout: The insurance company will then pay the remaining $2,500 ($3,000 total damage – $500 deductible) to the repair shop.

If the damage to your car was only $400, and your deductible is $500, then you would be responsible for the entire $400 in repair costs. The insurance company wouldn’t pay anything in this scenario because the claim amount is less than your deductible.

It’s important to note that deductibles typically apply to specific types of coverage within your auto insurance policy. The most common coverages that have deductibles are:

- Collision Coverage: This covers damage to your vehicle resulting from a collision with another vehicle or object, regardless of who is at fault.

- Comprehensive Coverage: This covers damage to your vehicle from non-collision events, such as theft, vandalism, fire, natural disasters (hail, floods), and falling objects.

Other coverages, like liability insurance (which covers damage you cause to others) or medical payments coverage, usually do not have deductibles.

Differentiating Deductibles: Standard vs. Zero-Deductible Options

While the concept of a deductible is universal, the specific amounts and types can vary significantly between insurance providers and policies. Understanding these differences is crucial for tailoring your coverage to your financial situation.

Standard Deductibles:

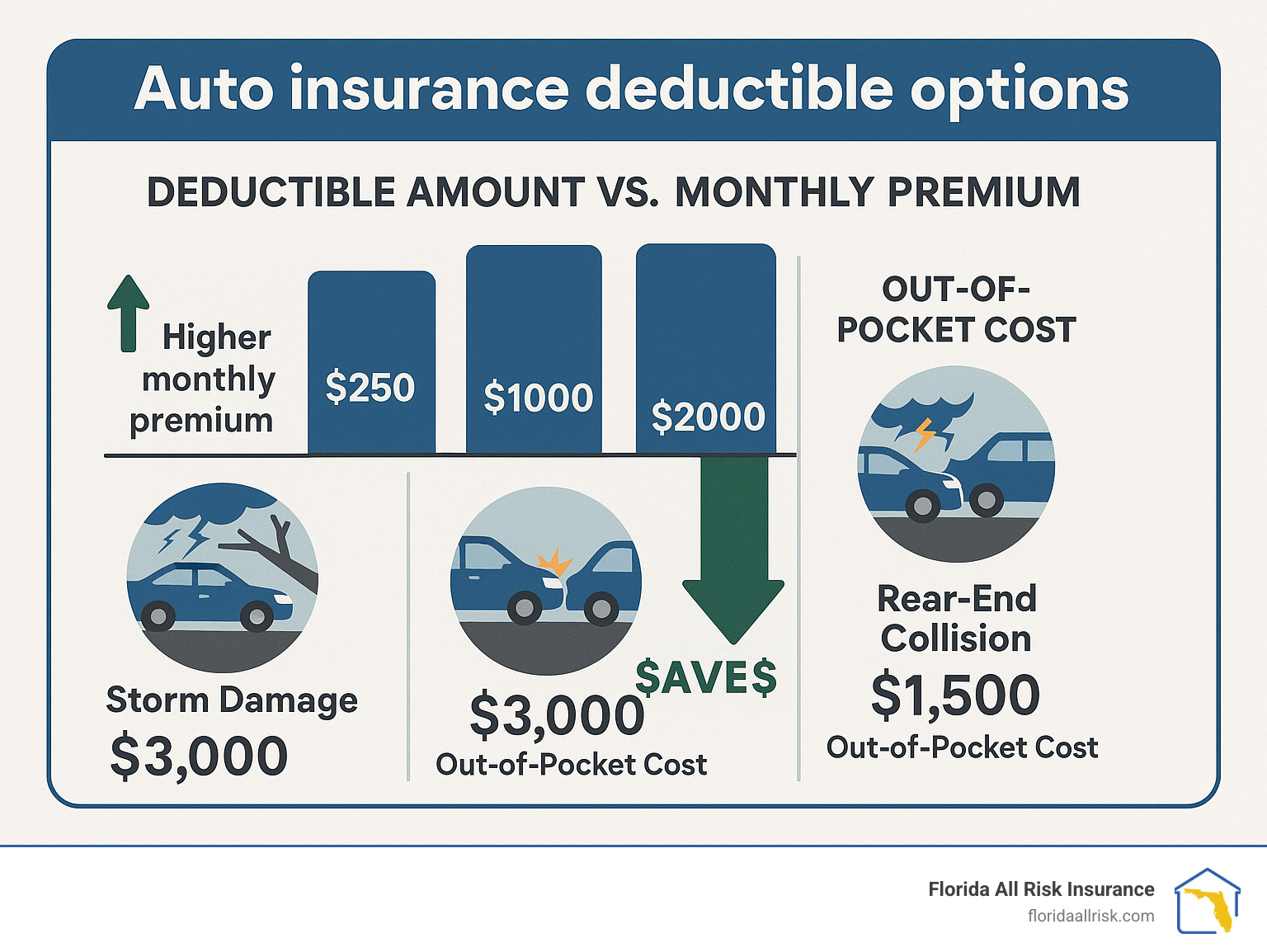

The most common scenario involves policies with standard deductibles. These are pre-set amounts that you choose when you purchase your policy. Common deductible amounts often range from:

- $250

- $500

- $1,000

- $2,500

The choice between these amounts is a fundamental decision that impacts your premium.

Zero-Deductible Options:

Some insurance companies offer policies with a “zero deductible” option, particularly for certain coverages like comprehensive or glass claims. This means that if you have a covered incident under that specific coverage, your insurance company will pay the full repair or replacement cost without you having to pay any out-of-pocket amount.

While a zero-deductible policy might sound incredibly appealing, it’s important to understand its implications:

- Higher Premiums: Insurance companies offset the increased risk of paying out the full amount for every claim by charging significantly higher premiums for zero-deductible policies.

- Limited Availability: Not all insurance providers offer zero-deductible options, and they might be restricted to specific types of coverage or vehicles.

- Strategic Consideration: A zero-deductible can be a worthwhile investment for drivers who prioritize financial predictability and can afford the higher premium, or for those who frequently drive in areas prone to specific risks (e.g., hail, windshield damage).

When reviewing your policy options, it’s essential to clarify with your insurance agent precisely which coverages have deductibles and what those amounts are.

The Impact of Your Deductible Choice: Premium vs. Out-of-Pocket Expenses

The deductible you choose for your auto insurance policy has a direct and significant impact on two key financial aspects: your monthly premiums and your potential out-of-pocket expenses in the event of a claim. This relationship is often described as an inverse correlation – a higher deductible generally leads to a lower premium, and vice versa.

The Trade-off: Lower Deductible, Higher Premium

When you opt for a lower deductible (e.g., $250), you are essentially telling your insurance company that you are willing to pay a smaller portion of any future claim. This means that in the event of an accident, your out-of-pocket expense will be less. Consequently, the insurance company assumes a greater financial risk, as they will be responsible for paying out a larger sum more frequently. To compensate for this increased risk, they will charge you a higher premium.

Advantages of a Lower Deductible:

- Reduced Financial Burden During Claims: If you need to file a claim, your out-of-pocket expenses will be minimal. This can provide significant peace of mind, especially if you have limited savings or a tight budget.

- More Affordable for Frequent Claimers: Drivers who anticipate needing to file claims more often might find a lower deductible more cost-effective in the long run, as the cumulative savings on claim payouts could outweigh the higher premiums.

Disadvantages of a Lower Deductible:

- Higher Monthly/Annual Premiums: You will be paying more consistently for your insurance coverage, which can strain your budget over time.

- Less Incentive for Careful Driving: While this is not a conscious decision for most, a lower deductible might inadvertently reduce the financial sting of minor incidents, potentially leading to less diligent risk mitigation for some individuals.

The Trade-off: Higher Deductible, Lower Premium

Conversely, choosing a higher deductible (e.g., $1,000 or $2,500) signifies that you are willing to bear a larger portion of the financial responsibility if a claim arises. This reduces the insurance company’s risk, as they will only be liable for the amount exceeding your deductible. As a result, they can afford to offer you a lower premium.

Advantages of a Higher Deductible:

- Lower Monthly/Annual Premiums: This can lead to substantial savings on your insurance costs over the policy term, freeing up funds for other financial goals or everyday expenses.

- Financial Incentive for Careful Driving: Knowing that you’ll have to pay more out-of-pocket in case of an accident can serve as a strong motivator to drive more cautiously and avoid preventable incidents.

- Suitable for Financially Stable Individuals: If you have a robust emergency fund or sufficient savings to comfortably cover the higher deductible amount if needed, a higher deductible can be a smart financial move.

Disadvantages of a Higher Deductible:

- Significant Out-of-Pocket Expenses During Claims: If you do need to file a claim, you’ll be responsible for paying a larger sum upfront. This could be a substantial financial hardship if you are not adequately prepared.

- Potential for Not Filing Small Claims: If the cost of repairs is only slightly above your high deductible, you might choose not to file a claim to avoid the expense and potential premium increases. While this saves money in the short term, it might mean you’re not adequately protected for minor damages.

The decision of which deductible to choose is a personal one, heavily influenced by your financial stability, your risk tolerance, and your driving habits. It’s a careful balancing act between minimizing your ongoing insurance costs and ensuring you can comfortably afford potential repair bills after an incident.

Navigating Your Deductible: Practical Tips for Drivers

Understanding what a deductible is and how it impacts your premiums is the first step. The next is to actively manage this aspect of your auto insurance policy to your advantage. Here are some practical tips to help you navigate your deductible choices and optimize your insurance coverage.

1. Assess Your Financial Readiness

The most crucial factor in deciding on a deductible amount is your ability to pay it. Before committing to a policy, honestly assess your financial situation.

- Emergency Fund: Do you have an emergency fund that can comfortably cover the deductible amount? If a $1,000 deductible is required, can you access $1,000 without dipping into essential living expenses or savings designated for other critical goals?

- Risk Tolerance: How comfortable are you with the idea of paying a larger sum out-of-pocket? Some individuals are naturally more risk-averse and prefer the security of a lower deductible, even if it means higher premiums. Others are more comfortable taking on more risk for the potential savings.

- Cash Flow: Consider your monthly cash flow. Can you absorb a higher premium for a lower deductible, or would the savings from a higher deductible be more beneficial for your budget?

Actionable Advice: Before you even start shopping for insurance, calculate how much you could realistically afford to pay in an emergency. This will set a practical upper limit for your deductible.

2. Shop Around and Compare Quotes

Insurance companies have different pricing structures and appetites for risk. What might be a high premium for one insurer with a certain deductible could be more competitive with another.

- Vary Deductible Options: When getting quotes, don’t just ask for one deductible amount. Request quotes for multiple deductible levels (e.g., $500, $1,000, and $2,500) from each insurer. This will give you a clear picture of how much you can save by increasing your deductible.

- Compare Insurers: Obtain quotes from at least three to five different insurance companies. Prices can vary significantly, and you might find a much better deal by comparing.

- Understand the “Total Cost”: Don’t just look at the premium. Calculate the potential total cost of insurance over a year with different deductibles. For example, a policy with a $500 deductible might have a $1,200 annual premium, while a policy with a $1,000 deductible might have a $900 annual premium. The $300 difference in premium is what you’re paying for the reduced out-of-pocket risk.

Actionable Advice: Utilize online comparison tools and speak directly with insurance agents. Be transparent about your needs and ask for quotes with various deductible options for comprehensive and collision coverage.

3. Consider Your Vehicle and Driving Habits

The type of vehicle you drive and your typical driving patterns can also influence your deductible decision.

- Vehicle Value: If you drive an older, lower-value car, the cost of repairs might approach or exceed the value of the car. In such cases, a higher deductible might make more sense, as you might be more inclined to pay for minor repairs out-of-pocket rather than file a claim that could lead to your car being declared a total loss.

- Newer/High-Value Vehicles: For newer or more expensive vehicles, you might prefer a lower deductible to minimize your financial exposure in case of significant damage.

- Driving Location and Frequency: If you live in an area prone to specific risks (e.g., hail, car theft) or if you commute long distances daily, you might face a higher likelihood of filing claims. This could influence your decision towards a deductible that aligns with your risk assessment.

Actionable Advice: Factor in the age, value, and repair costs associated with your specific vehicle when determining an appropriate deductible. Also, reflect on your typical daily commute and the types of roads you frequent.

4. Review Your Policy Annually

Your financial situation and insurance needs can change over time. It’s crucial to review your auto insurance policy at least once a year, especially before your renewal date.

- Re-evaluate Financial Readiness: Has your income or savings changed? Are you now in a better or worse position to handle a higher deductible?

- Check for Discounts: Your insurer might offer new discounts that could impact your overall premium and make a lower deductible more affordable.

- Shop for New Quotes: Don’t assume your current insurer always offers the best deal. The market changes, and new providers may offer more competitive rates.

Actionable Advice: Schedule a review of your insurance policy in your calendar annually. This proactive approach ensures you’re always getting the best coverage for your evolving needs and financial circumstances.

By actively engaging with your auto insurance policy and considering these practical tips, you can make informed decisions about your deductible that best suit your financial security and peace of mind. The deductible is not just a number; it’s a powerful tool that, when understood and managed correctly, can lead to significant savings and a more predictable insurance experience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.