In the modern landscape of digital finance, Venmo has evolved from a simple peer-to-peer (P2P) payment app into a robust financial tool used by millions to manage daily expenses, split bills, and even run small businesses. However, as users transition from sending small amounts for coffee to managing larger capital flows for rent or freelance services, understanding the platform’s financial boundaries becomes critical. Knowing exactly how much you can send on Venmo is not just about a single number; it is about understanding the tiers of verification, the nuances of business vs. personal profiles, and the regulatory frameworks that govern digital liquidity.

Understanding Venmo’s Transfer Limits: Unverified vs. Verified Accounts

The amount of money you can move through Venmo is primarily dictated by your account’s verification status. This is a security and compliance measure designed to prevent money laundering and fraud, ensuring that the platform remains a safe environment for financial exchange.

The Constraints of Unverified Accounts

When you first sign up for Venmo, your account is considered “unverified.” In this stage, your spending power is significantly curtailed. For most new users, the weekly rolling limit for all transactions combined is $299.99. This includes person-to-person payments and purchases made through authorized merchants. While this may suffice for casual social interactions, it is a major bottleneck for anyone looking to use the app for significant financial management.

The Benefits of Identity Verification

To unlock the full potential of the platform, users must undergo the identity verification process. This involves providing your legal name, physical address, date of birth, and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

Once verified, your total weekly spending limit jumps significantly. For most verified users, the combined weekly limit for payments is $60,000. However, this is further broken down into specific categories:

- Person-to-Person (P2P) Payments: Usually capped at $4,999.99 per week.

- Authorized Merchant Payments: Includes purchases made via the Venmo Debit Card or “Pay with Venmo” options at checkout, often capped at much higher amounts within the $60,000 total.

The “Rolling Weekly” Logic

It is vital to understand that Venmo uses a “rolling” limit rather than a calendar-week limit. This means that a transaction doesn’t clear from your limit exactly on Monday morning; instead, it counts against your limit for exactly 168 hours (seven days) from the moment the transaction was authorized. For those managing tight cash flows or frequent high-value transfers, tracking the timing of payments is essential to avoid declined transactions.

Managing Your Cash Flow: How to Increase and Optimize Your Limits

For individuals using Venmo as a primary financial tool, hitting a limit can disrupt personal budgeting and business operations. Managing these limits requires a proactive approach to your digital wallet’s settings and a clear understanding of how the platform categorizes your “spend.”

Navigating the Verification Process

The verification process is the single most effective way to increase your sending capacity. Beyond just the SSN, Venmo may occasionally ask for additional documentation, such as a photo of a government-issued ID or a utility bill, to confirm your residency. Successfully completing this not only raises your limits but also adds a layer of institutional security to your funds, making it easier to recover your account in the event of a dispute.

Strategizing Large Payments

If you need to send a payment that exceeds the $4,999.99 P2P limit—for example, a large security deposit for an apartment—you cannot simply “increase” the limit beyond the platform’s hard cap. In these instances, financial strategy comes into play. Users often split large payments over two rolling weeks or utilize the “Pay with Venmo” feature if the recipient is an authorized business merchant, as business transaction limits are often higher than P2P limits.

Monitoring Your “Available Funds” vs. Linked Methods

Your sending limit is also influenced by where the money is coming from. While your overall limit remains the same, your “Venmo Balance” may have its own internal restrictions if it has not been fully verified. Using a linked bank account via Plaid or a verified credit card ensures that your liquidity is backed by traditional banking institutions, which often allows for smoother processing of high-value transfers.

Business and Side Hustle Finances on Venmo

With the rise of the gig economy, Venmo has become a staple for freelancers, photographers, and small-scale vendors. However, using a personal profile for business transactions can lead to account freezes or tax complications. Understanding the financial limits of a “Business Profile” is a prerequisite for professional financial health.

Venmo for Business Profile Limits

Business profiles are designed for those selling goods or services. These profiles have their own set of limits, which are often more generous than personal P2P limits to accommodate higher transaction volumes. For a verified business profile, the weekly limit for sending money to other users or paying for services is often consistent with personal verified limits, but the ability to receive funds is much more flexible, allowing for larger scales of operation.

Tax Implications and 1099-K Reporting

A critical aspect of sending and receiving money for business is the IRS reporting requirement. Under current tax laws, payment processors like Venmo are required to report gross payments for goods and services that exceed certain thresholds. If you use a business profile or tag a payment as “Goods and Services,” Venmo will track these amounts. If you exceed the annual threshold (which has been subject to recent legislative changes, currently trending toward a $600 floor for reporting), you will receive a Form 1099-K. This makes it imperative to keep meticulous records of your Venmo transactions to ensure your reported income matches your actual business revenue.

Professional Branding through Payments

From a financial tool perspective, the business profile allows you to separate personal “social” spending from professional “income” spending. This separation is crucial for audit trails and simplified accounting. When you send money to suppliers or receive money from clients, the professional categorization ensures that your personal limit for sending money to friends (P2P) remains untouched by your business expenses.

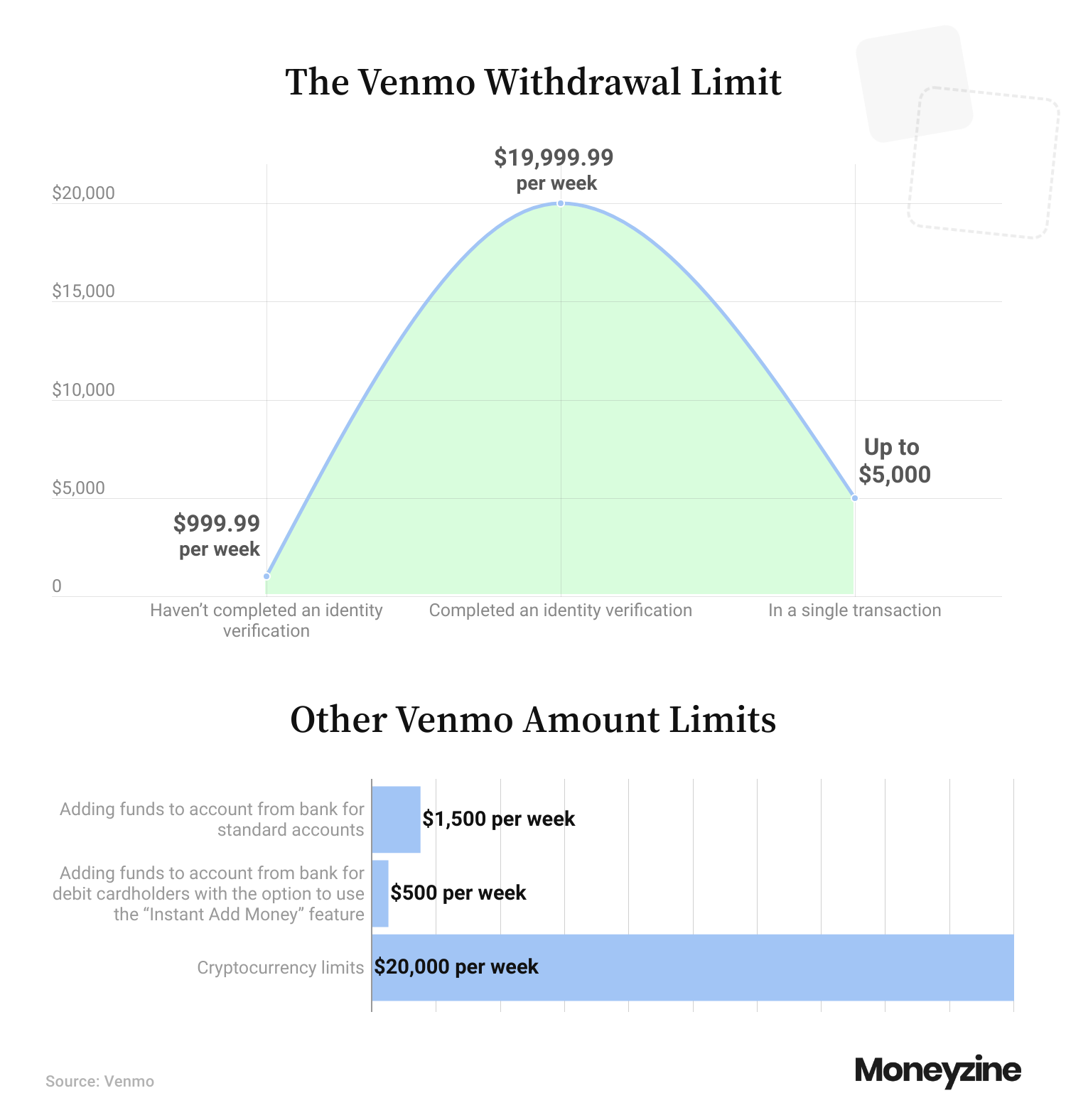

Moving Money Out: Withdrawal and Instant Transfer Limits

Knowing how much you can send is only half the battle; knowing how quickly and how much you can withdraw to your external bank account is equally important for maintaining liquidity.

Standard Bank Transfers vs. Instant Transfers

Venmo offers two primary ways to move money to your bank account:

- Standard Transfers: These take 1–3 business days and are free. They are ideal for non-urgent financial balancing.

- Instant Transfers: These occur within minutes for a small percentage fee. For those who need immediate access to capital for other investments or bills, this is a vital feature. However, instant transfers have their own limits—typically $50,000 per transaction for verified users, though this is subject to the receiving bank’s limitations as well.

Venmo Debit Card and ATM Limits

For those who treat Venmo like a checking account, the Venmo Debit Card provides a physical way to spend your balance. This card has a separate set of limits:

- Daily Purchase Limit: Usually $3,000.

- Daily ATM Withdrawal Limit: Usually $400.

- Daily Cash Back Limit: Usually $400.

These limits are designed to protect you from significant loss in the event your card is stolen. From a financial planning perspective, you should not rely on the Venmo card for high-value daily purchases if they exceed the $3,000 threshold.

Best Practices for High-Value Financial Transactions

When dealing with the upper echelons of Venmo’s limits—sending thousands of dollars at a time—the margin for error shrinks. Financial responsibility dictates a more rigorous approach to these transactions than one would use for a $20 dinner split.

Security Measures for Large Transfers

Before sending a high-value payment, always verify the recipient’s identity. Venmo now offers a “last four digits of the phone number” verification feature for new contacts. Use this. Additionally, ensure that your account is secured with multi-factor authentication (MFA) and biometric locks. Because Venmo transactions are generally irreversible, a mistake in the recipient’s username or a compromised account can lead to permanent financial loss.

Comparing Venmo to Traditional Banking and Other FinTech Tools

While Venmo is convenient, it is not always the most efficient tool for every financial task. For extremely large transfers (e.g., $100,000+), traditional wire transfers or cashier’s checks remain the standard due to their legal protections and lack of “rolling” limits. Similarly, for business-to-business (B2B) payments involving complex invoicing and net-30 terms, platforms like Quickbooks or Bill.com might offer better fiscal tracking than Venmo.

Conclusion: Integrating Venmo into Your Financial Ecosystem

Understanding how much you can send on Venmo is the first step in mastering this modern financial tool. By verifying your identity, distinguishing between personal and business use, and respecting the rolling weekly limits, you can turn a simple app into a powerful engine for wealth management and commerce. Whether you are a freelancer managing client payments or a consumer handling household expenses, staying within the platform’s legal and technical boundaries ensures that your money remains mobile, secure, and ready for use whenever you need it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.