Budgeting is often perceived as a restrictive practice, a financial diet that forces individuals to cut out the things they love. However, in the realm of personal and business finance, a budget is not a cage; it is a roadmap. It is the tactical translation of your goals into a tangible plan. When we ask, “How do we budget?” we are essentially asking how we can take control of our future.

The process of budgeting requires a blend of psychological discipline, strategic planning, and the right set of tools. Whether you are managing a household, a side hustle, or a scaling business, the principles of resource allocation remain the same. This guide explores the foundational philosophies, proven frameworks, and practical steps necessary to master the art of the budget.

The Philosophy of Budgeting: Shifting from Scarcity to Intentionality

Before diving into spreadsheets and numbers, it is crucial to address the mindset behind budgeting. Most people fail to stick to a budget because they view it through the lens of scarcity. To succeed, one must pivot toward a mindset of intentionality.

Shifting from Scarcity to Intentionality

A budget is simply a tool that ensures your spending aligns with your values. When we look at our bank statements, we often see a series of reactive decisions—ordering takeout because we were tired, or buying a subscription we forgot to cancel. Budgeting shifts the power dynamic. Instead of wondering where your money went at the end of the month, you tell your money where to go at the beginning. This intentionality reduces financial anxiety and provides a sense of agency that “winging it” never can.

Identifying Your Financial “Why”

Without a clear objective, a budget is just a list of numbers. To maintain the discipline required for long-term financial health, you must identify your “why.” Are you budgeting to escape the cycle of debt? Are you saving for a down payment on a home? Or are you looking to build a capital fund for a new business venture? Identifying these milestones allows you to view every dollar saved not as a loss of current pleasure, but as a deposit toward a future goal.

Proven Budgeting Frameworks for Every Lifestyle

There is no “one size fits all” approach to finance. The best budget is the one you can actually stick to. Depending on your personality and financial complexity, one of the following three frameworks will likely resonate most.

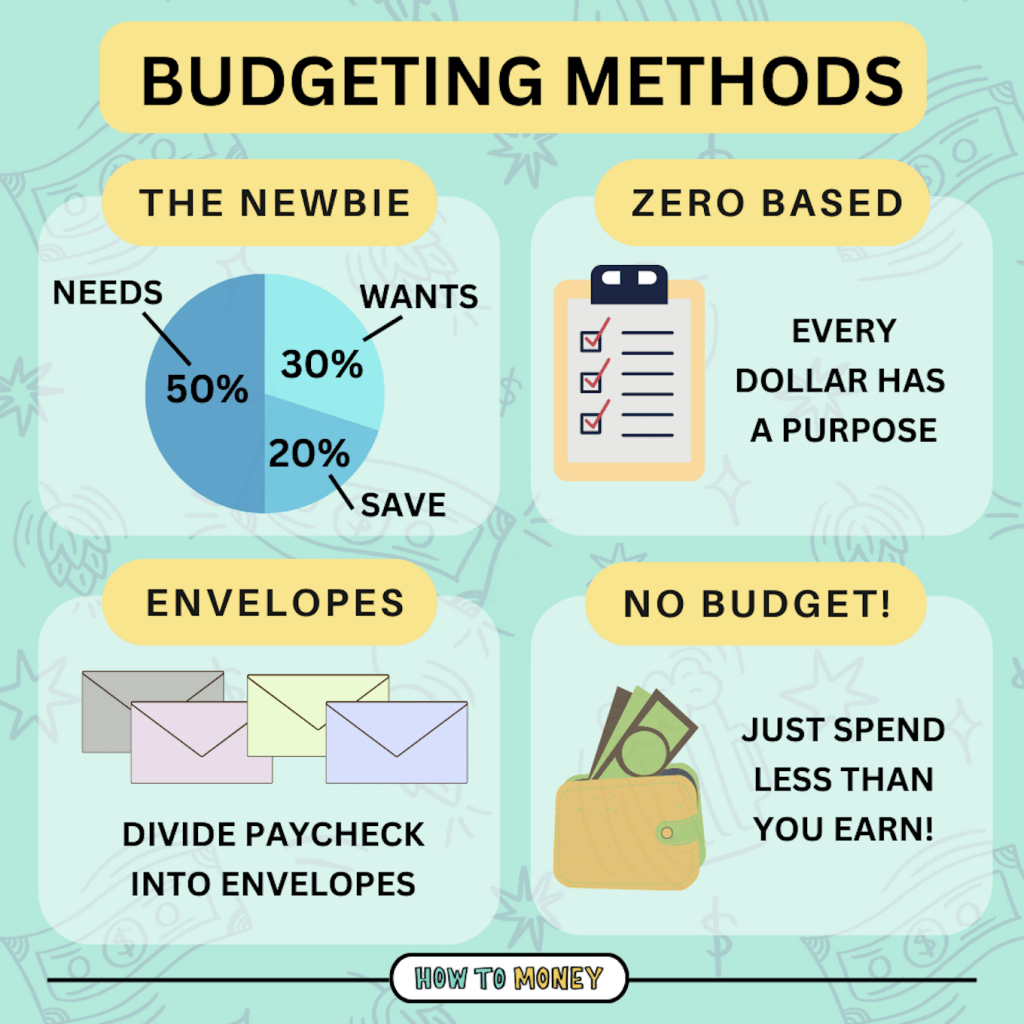

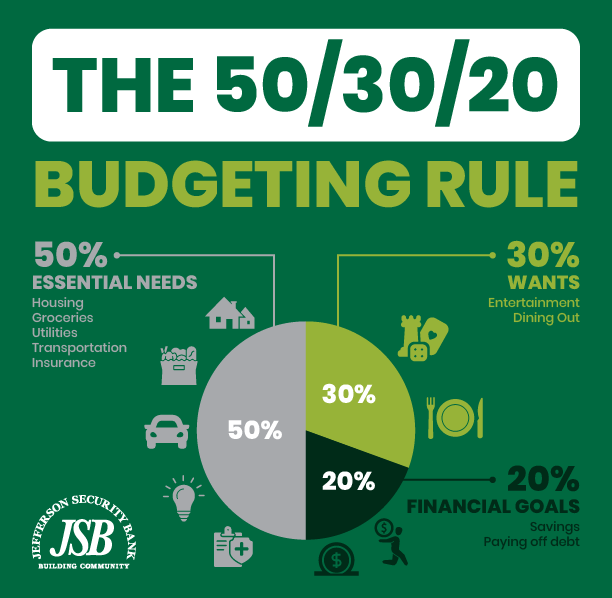

The 50/30/20 Rule: Simplicity at Its Best

Popularized by Senator Elizabeth Warren, the 50/30/20 rule is perhaps the most accessible framework for beginners. It divides your after-tax income into three distinct buckets:

- 50% for Needs: This includes non-negotiable expenses like rent or mortgage, utilities, groceries, insurance, and minimum debt payments.

- 30% for Wants: This is your “lifestyle” category. It covers dining out, hobbies, streaming services, and travel.

- 20% for Savings and Debt Repayment: This portion is dedicated to building an emergency fund, investing in retirement accounts, or making extra payments on high-interest debt.

The beauty of this method lies in its simplicity. It provides a high-level overview of financial health without requiring you to track every single penny.

Zero-Based Budgeting: Giving Every Dollar a Job

For those who prefer granular control, Zero-Based Budgeting (ZBB) is the gold standard. The core principle of ZBB is that your income minus your expenses should equal zero at the end of the month. This does not mean you have zero dollars in your bank account; rather, it means every dollar has been assigned to a specific category—including savings and investments.

If you earn $5,000 in a month, you must allocate all $5,000. If you find you have $200 left over after covering all bills and savings goals, you must decide where that $200 goes—perhaps into an “unforeseen maintenance” fund or a “vacation” fund. This method is highly effective for curbing impulsive spending.

The “Pay Yourself First” Method

Also known as reverse budgeting, this strategy prioritizes savings and debt reduction above all else. Instead of calculating what is left over at the end of the month to save, you decide on a savings goal first. Once that amount is automatically diverted to your savings or investment accounts on payday, you are free to spend the remainder of your income as you see fit. This is an excellent strategy for those who find traditional tracking too tedious but still want to ensure they are meeting their long-term financial targets.

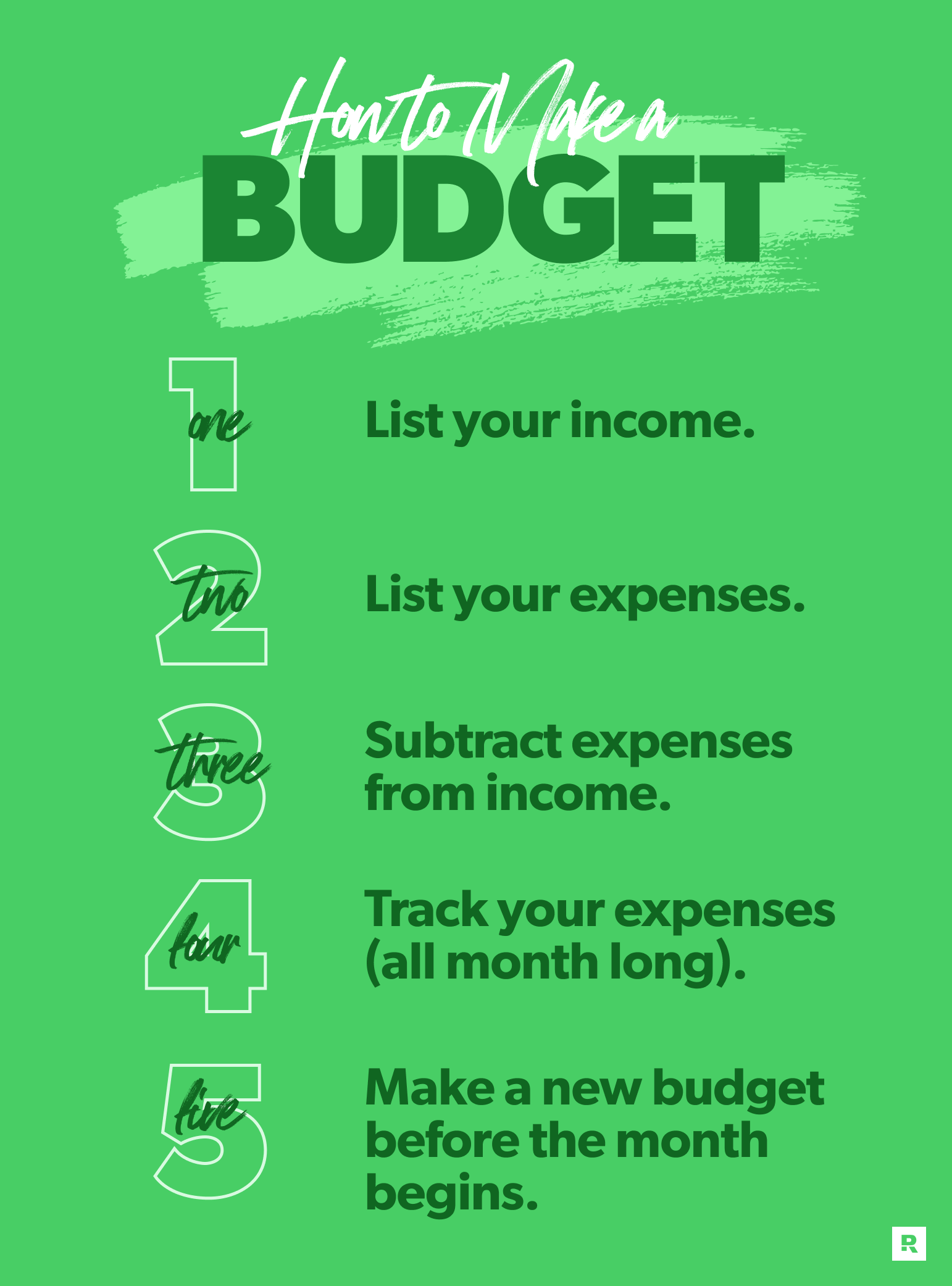

The Practical Process: Steps to Building Your First Budget

Once you have chosen a framework, it is time to get into the mechanics. The transition from theory to practice involves a clear, three-step process.

Tracking Income and Mandatory Expenses

The first step is to establish your baseline. Calculate your total net income—the amount that actually hits your bank account after taxes and deductions. Next, list your “fixed” or mandatory expenses. These are costs that remain relatively constant each month, such as housing, car payments, and basic utilities. Understanding this baseline is critical because it reveals your “disposable income”—the actual amount you have available to play with for variable expenses and savings.

Auditing Variable Spending Habits

This is often the most eye-opening part of the process. For 30 days, track every single purchase. Most people are surprised to find how much “leakage” occurs in small, unnoticed increments—the $7 coffee, the unused gym membership, or the convenience fees on food delivery apps. By auditing these variable expenses, you can identify areas where you can “trim the fat” without significantly impacting your quality of life.

Setting Realistic Savings and Debt Repayment Goals

A common mistake is setting goals that are too aggressive, leading to burnout. If you currently save 0% of your income, jumping immediately to 20% might be unsustainable. Start by building a “starter” emergency fund (typically $1,000 to $2,000) to protect against minor crises. Once that is in place, focus on high-interest debt—anything with an interest rate above 7%—using either the “Debt Snowball” (paying smallest balances first for psychological wins) or the “Debt Avalanche” (paying highest interest rates first to save money over time).

Leveraging Technology and Tools for Financial Efficiency

In the modern era, you don’t need a physical ledger to manage your money. Technology has streamlined the budgeting process, making it more accurate and less time-consuming.

Top-Tier Budgeting Apps and Software

The market is filled with sophisticated tools designed to sync with your bank accounts and categorize your spending automatically.

- YNAB (You Need A Budget): This software is built specifically for the Zero-Based Budgeting philosophy and is widely considered the best for changing spending behavior.

- Monarch Money and Empower: These platforms offer comprehensive dashboards that track net worth, investment portfolios, and monthly spending in one place.

- Custom Spreadsheets: For those who prioritize privacy and total customization, a well-built Excel or Google Sheets template remains an elite option.

The Power of Automated Transfers

One of the greatest “hacks” in personal finance is automation. Human willpower is a finite resource. By setting up automated transfers to your savings, retirement, and brokerage accounts, you remove the need to make a conscious decision every month. Automation ensures that your “future self” gets paid before you have the chance to spend the money on current desires.

Sustaining the Habit: Overcoming Common Budgeting Pitfalls

A budget is a living document, not a static monument. To succeed over the long term, you must be prepared for the fluctuations of real life.

Dealing with Irregular Income or Unexpected Costs

For freelancers, entrepreneurs, or those in commission-based roles, budgeting can be challenging because income varies. The solution is to budget based on your “floor”—the minimum amount you expect to earn in a bad month. Any income above that floor can be treated as a bonus and directed toward “sinking funds” (savings accounts for specific future costs like car repairs or annual insurance premiums).

The Importance of Monthly Reviews and Adjustments

At the end of every month, conduct a “financial post-mortem.” Did you overspend in the dining out category? Why? Was it a special occasion, or a lack of meal planning? Don’t punish yourself for deviations; instead, adjust the budget for the following month. If you consistently overspend on groceries, your grocery budget might simply be too low for your reality. Adjust the numbers to reflect the truth of your life.

Mastering how we budget is ultimately about achieving freedom. It provides the clarity to stop worrying about the “now” and start building for the “next.” By choosing a framework that fits your personality, leveraging modern tools, and maintaining a mindset of intentionality, you can transform your relationship with money from one of stress to one of power.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.