In the world of personal and business finance, few strings of numbers are as foundational yet misunderstood as the routing transit number (RTN). If you have ever looked at the bottom of a paper check, you have likely seen a series of computer-style digits printed in a unique font. Among these is the routing number—a nine-digit code that acts as the primary “address” for your financial institution within the vast landscape of the American banking system.

Understanding what a routing number is, how it functions, and why it is critical to your financial security is essential for anyone navigating modern banking. Whether you are setting up direct deposit for a new job, paying a mortgage online, or sending a domestic wire transfer, the routing number is the silent engine that ensures your money arrives at the correct destination.

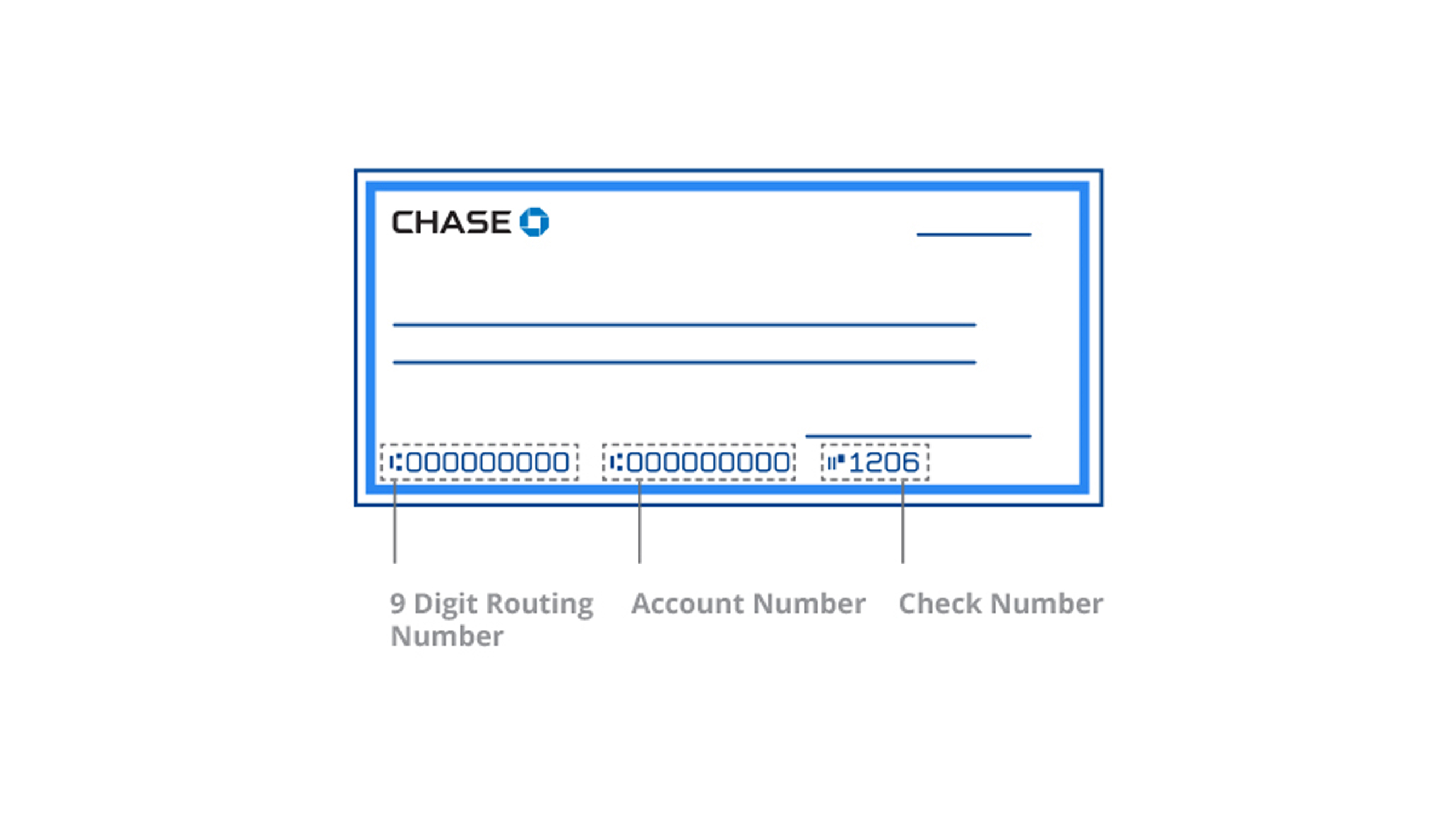

Understanding the Anatomy of a Check: The ABA Routing Number

When you hold a check, the bottom row of numbers—known as the MICR (Magnetic Ink Character Recognition) line—is designed to be read by high-speed sorting machines. This line typically consists of three distinct sets of numbers: the routing number, the account number, and the check number.

What is a Routing Number?

A routing number is a nine-digit numerical code used by financial institutions to identify themselves. Developed by the American Bankers Association (ABA) in 1910, this system was originally designed to make check processing more efficient. In the early 20th century, the volume of paper checks was exploding, and banks needed a standardized way to sort and route these documents to the correct clearinghouse. Today, while paper checks are less common, the routing number remains the standard identifier for electronic transfers, including ACH (Automated Clearing House) and wire transfers.

Where to Find it on Your Check

For most personal checks, the routing number is the nine-digit sequence located at the far left of the MICR line. It is flanked by a specific symbol that looks like a vertical bar with a small square. In some instances, particularly on business checks, the order might vary slightly, but the routing number will always be exactly nine digits long. If you do not have a physical checkbook, you can almost always find your routing number by logging into your online banking portal or mobile app under “Account Details.”

Decoding the Nine Digits

A routing number is not a random sequence of integers; it is a structured code that tells a story about the bank it represents:

- The First Four Digits: These represent the Federal Reserve routing symbol. Specifically, the first two digits identify which of the 12 Federal Reserve districts the bank is located in.

- Digits Five through Eight: These identify the specific financial institution (the “ABA Institution Identifier”).

- The Ninth Digit: This is the “check digit.” It is calculated using a complex mathematical formula involving the first eight digits. If the result of the formula doesn’t match the ninth digit, the sorting machine knows there has been a reading error.

The Financial Significance of the Routing Number

While it may seem like a mere administrative detail, the routing number is the backbone of the movement of capital in the United States. Without this standardized system, the “Money” category of our economy would grind to a halt, as there would be no automated way to distinguish between thousands of different banks and credit unions.

Domestic Wire Transfers vs. ACH Payments

One of the most common points of confusion in personal finance is the difference between an ACH routing number and a Wire routing number. Many large national banks use one routing number for electronic payments like direct deposits and bill pay (ACH) and a completely different routing number for domestic wire transfers. Using the ACH routing number for a wire transfer can result in the transaction being rejected or delayed, which can be costly if you are trying to close on a home or make a time-sensitive investment.

Direct Deposits and Bill Pay

For most consumers, the routing number is most frequently used when setting up direct deposit. By providing your employer with your routing and account numbers, you are essentially providing the “ZIP code” and “Street Address” for your funds. The routing number ensures the money reaches the right bank, and the account number ensures it reaches your specific pocket within that bank. This same logic applies to “pull” transactions, such as when a utility company or credit card issuer withdraws funds directly from your checking account.

How Businesses Use Routing Numbers for Payroll

From a business finance perspective, routing numbers are vital for managing payroll and B2B (business-to-business) payments. Companies use the routing numbers of their employees’ banks to distribute wages through the ACH network. For businesses, accuracy is paramount; a single digit error in a routing number can lead to thousands of dollars being “lost” in the banking ether, requiring a lengthy “trace” process through the Federal Reserve to recover.

Security and Management of Your Financial Data

Because the routing number is printed on every check you write, many people wonder if it is a sensitive piece of information. The answer is nuanced: while a routing number is not “secret,” it is a key component of your financial identity that must be managed with care.

Is Sharing Your Routing Number Safe?

Generally, sharing your routing number is safe because it is public information. Anyone can look up the routing number for a major bank like Chase or Bank of America online. However, the routing number becomes a security risk when it is paired with your personal account number. Together, these two numbers are all someone needs to initiate an unauthorized ACH withdrawal from your account. This is why you should only provide these details to trusted entities and avoid sending images of your checks over unencrypted email.

Protecting Your Bank Account from Fraud

In the digital age, “check washing” and ACH fraud are real threats. To protect your money, financial experts recommend regularly reviewing your bank statements for unauthorized transactions. If you notice a “debit” you didn’t authorize, it usually means someone obtained your routing and account number. Most modern banks offer “Positive Pay” services for business accounts, which cross-references checks presented for payment against a list of checks actually issued by the company.

What Happens if You Use the Wrong Routing Number?

If you accidentally provide the wrong routing number for an incoming transfer, the money will typically be returned to the sender after a few days. However, if the wrong routing number happens to belong to a real, different bank, the funds could potentially be deposited into an account there if the account numbers happen to match (though this is statistically unlikely). The primary consequence is usually a “Return Fee” charged by your bank or the service provider for the failed transaction.

Distinguishing Routing Numbers from Other Financial Identifiers

To manage your money effectively, you must be able to distinguish between the various codes used in the global financial system. The routing number is just one tool in a larger toolkit.

Routing Number vs. Account Number

Think of your bank as a massive apartment complex. The routing number is the street address of the building, which tells the mail carrier (the Federal Reserve) which building to go to. The account number is your specific apartment number, which tells the mail carrier exactly which door to slide the envelope under. You cannot have one without the other if you want the “mail” (your money) to arrive.

Routing Number vs. SWIFT/BIC Codes

The nine-digit ABA routing number is used exclusively for domestic transfers within the United States. If you are sending or receiving money internationally, you will likely need a SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or a BIC (Bank Identifier Code). These codes are the international equivalent of routing numbers and allow banks across different countries to communicate and move currency across borders.

Fraction Routing Numbers

If you look at the top right corner of a check, you will often see a number that looks like a fraction (e.g., 12-345/678). This is the “Fractional Routing Number.” It contains the same information as the nine-digit MICR routing number but is presented in a different format. This was historically used as a backup for bank tellers if the MICR line at the bottom was damaged or unreadable.

The Future of Routing in a Digital-First Economy

As we move toward a world of “Instant Payments” and “Real-Time Rails,” the role of the traditional routing number is evolving. The Federal Reserve’s “FedNow” service and the private sector’s “RTP” (Real-Time Payments) network still rely on these identifiers, but the speed at which transactions are cleared is moving from days to seconds.

For the savvy consumer or business owner, the routing number remains the most important “map” for their capital. By understanding its structure, its use in different types of transfers, and the security protocols required to protect it, you can ensure that your financial transactions are handled with the professional precision they deserve. Whether you are building a side hustle or managing a corporate treasury, mastery over these nine digits is a fundamental step in achieving financial literacy and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.