In the modern financial landscape, the boundary between traditional banking and digital wallets has become increasingly porous. Cash App, developed by Block, Inc., has evolved from a simple peer-to-peer (P2P) payment tool into a robust financial ecosystem offering everything from stock trading to Bitcoin purchasing. However, for many users, the primary utility of the app remains its ability to receive and hold funds. The true value of these digital balances is often realized only when they are moved into a traditional, interest-bearing, or more versatile bank account.

Understanding the nuances of transferring money from Cash App to a bank account is more than a technical necessity; it is a fundamental aspect of personal liquidity management. Whether you are a freelancer receiving payments from clients or an individual splitting a dinner bill, knowing how to navigate the speeds, fees, and security protocols of these transfers ensures that your capital remains accessible and productive.

The Foundation of Digital Transfers: Setting Up Your Financial Bridge

Before a single cent can move from the digital cloud of Cash App into your local bank vault, you must establish a secure link between the two entities. This process is the bedrock of your mobile financial strategy, ensuring that funds are routed accurately and securely.

Linking Your Bank Account vs. Debit Card

Cash App distinguishes between linking a bank account (via your routing and account numbers) and linking a debit card. While both allow for the movement of money, they serve different strategic purposes. Linking a bank account is essential for “Standard” transfers, which are processed via the Automated Clearing House (ACH) network. Conversely, linking a debit card is the prerequisite for “Instant” transfers. For a comprehensive financial setup, it is advisable to link both, providing you with the flexibility to choose between speed and cost-effectiveness depending on your immediate needs.

Verification and Security Protocols

To increase your transfer limits and ensure the safety of your assets, Cash App requires a verification process. This typically involves providing your full name, date of birth, and the last four digits of your Social Security Number. From a financial perspective, this “Know Your Customer” (KYC) compliance is vital. It not only protects the platform from illicit activity but also safeguards the user by establishing a legal identity associated with the funds. Once verified, users often see their sending and receiving limits significantly increased, allowing for larger-scale capital movement.

Executing the Transfer: Navigating Standard vs. Instant Options

Once your accounts are linked, the primary decision-making factor in moving your money is the balance between time and cost. Cash App offers two distinct pathways for cashing out, each catering to different financial circumstances.

The Standard Transfer: The Cost-Effective Choice

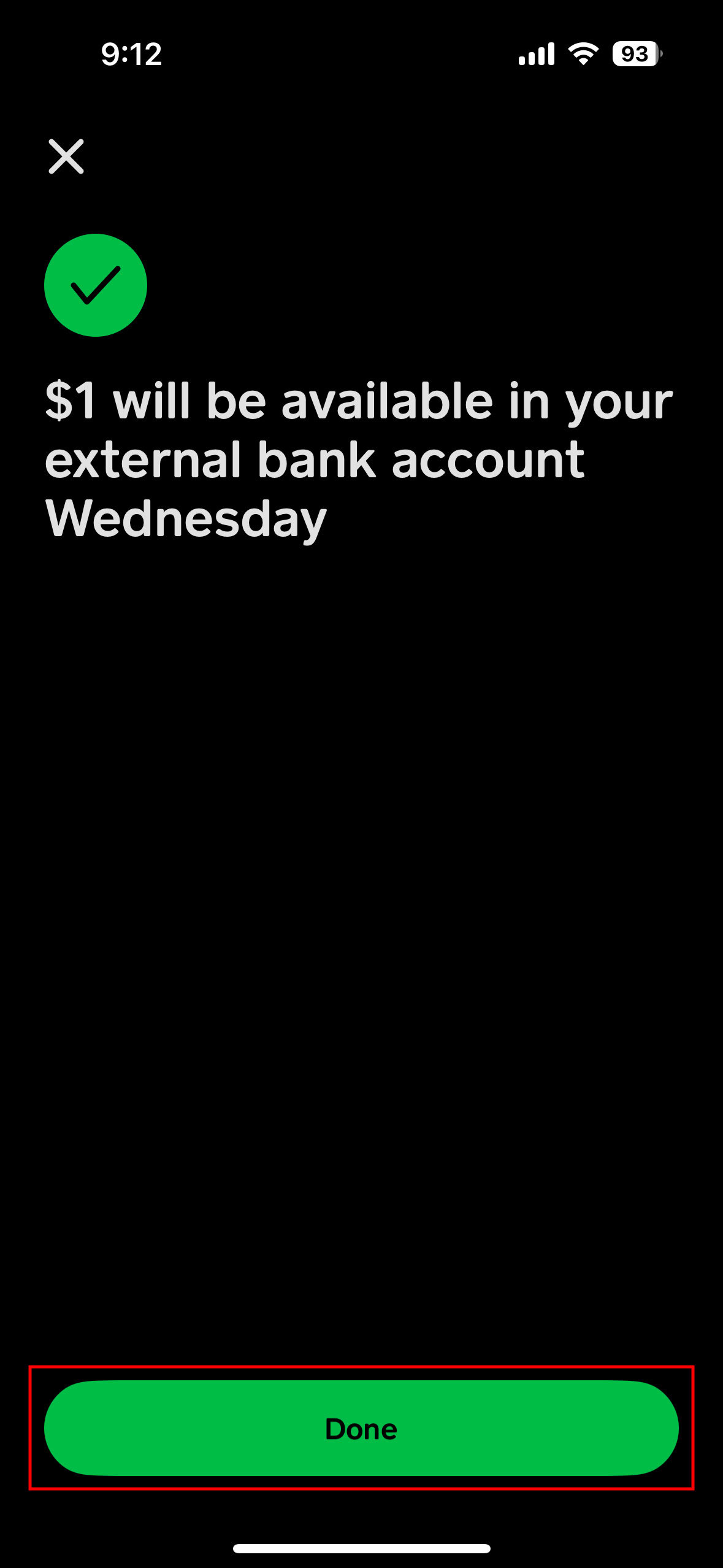

The Standard transfer is the preferred method for users who are not in an immediate rush for liquidity. This method utilizes the ACH network, which is the standard for domestic electronic fund transfers in the United States.

- Timeline: Typically takes one to three business days.

- Cost: Free of charge.

- Strategy: This is the most prudent choice for regular financial maintenance. If you are moving money to pay monthly bills or to fund a long-term savings goal, the Standard transfer allows you to retain 100% of your capital without succumbing to convenience fees.

The Instant Transfer: Liquidity on Demand

In contrast, the Instant transfer option is designed for scenarios where immediate access to cash is paramount. By leveraging the debit card networks (Visa or Mastercard), Cash App can push funds to your bank account almost instantaneously.

- Timeline: Usually within minutes, though it can occasionally take up to 30 minutes depending on the bank’s processing speed.

- Cost: A fee ranging from 0.5% to 1.75% (with a minimum fee of $0.25) is deducted from the transfer amount.

- Strategy: This option should be used strategically. While the convenience is high, frequent use of Instant transfers can lead to “fee leakage,” where a significant portion of your income is eroded by transaction costs over time.

Step-by-Step Execution via the App Interface

To initiate a transfer, the process is streamlined:

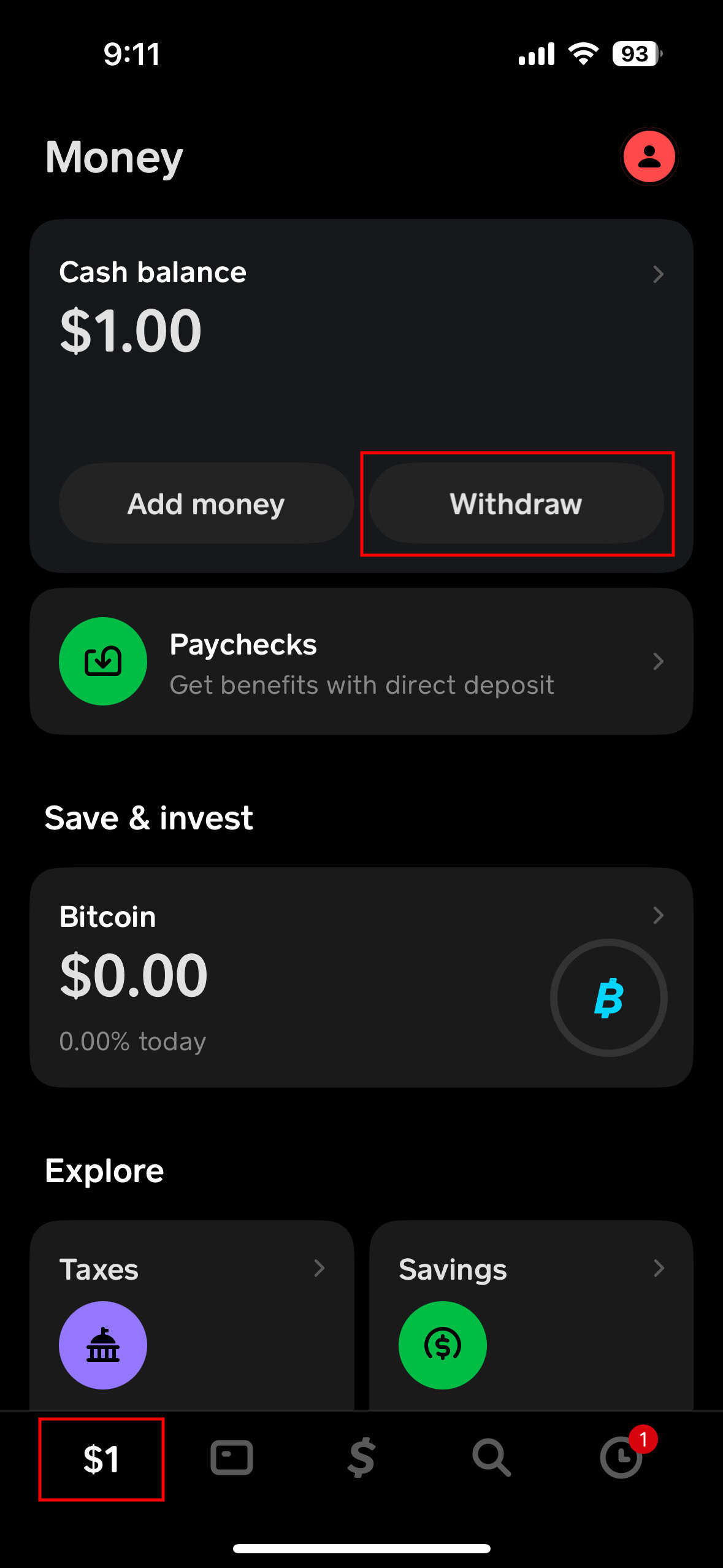

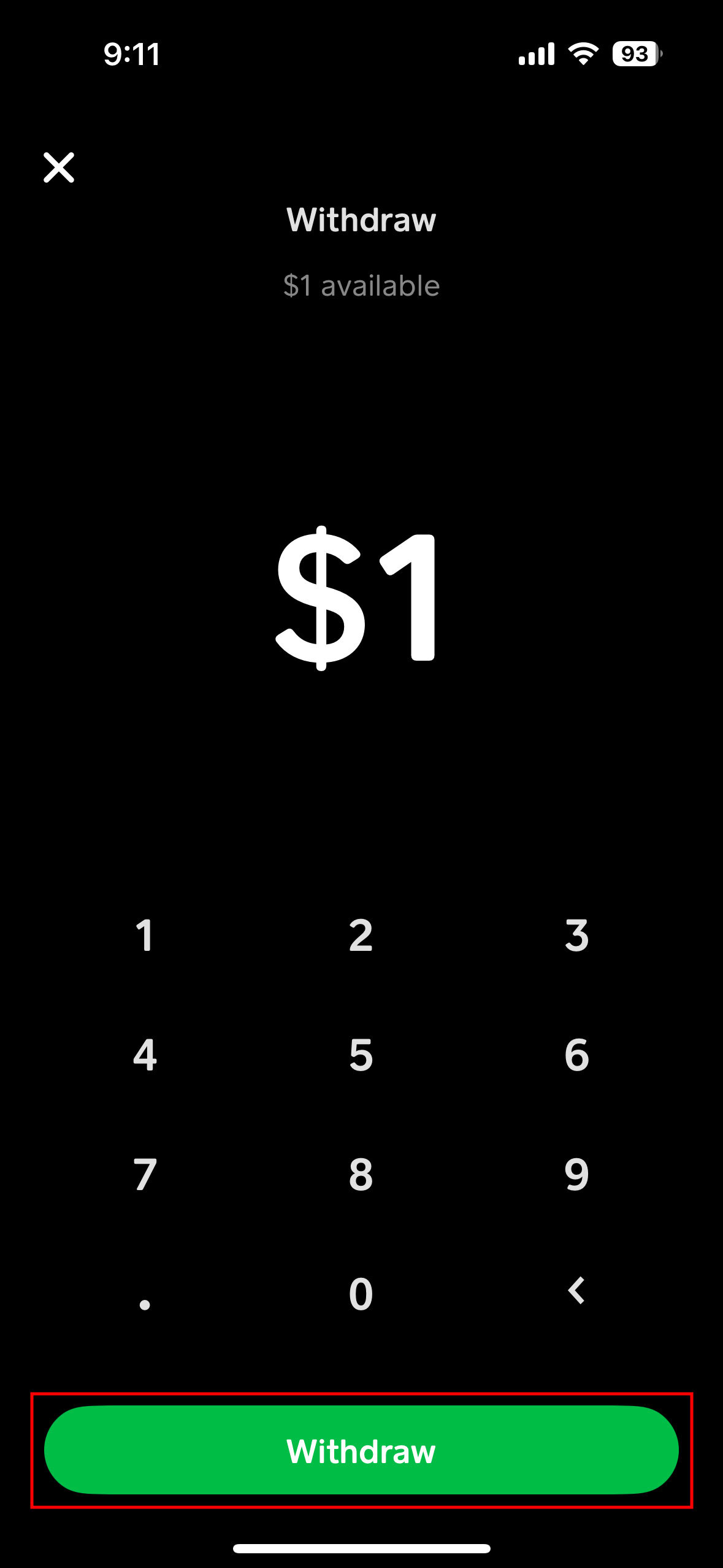

- Open Cash App and tap the “Money” tab (the icon that looks like a bank or a dollar amount) on the home screen.

- Select the “Cash Out” button located under your total balance.

- Choose the specific amount you wish to transfer.

- Select your preferred speed: “Standard” or “Instant.”

- Confirm the transaction using your PIN or biometric ID (Touch ID/Face ID).

Navigating Fees, Limits, and Regulatory Requirements

A sophisticated approach to personal finance requires an understanding of the underlying constraints and costs associated with digital tools. Cash App is no exception, and its fee structure and limits are key components of your broader financial picture.

Breaking Down the Costs of Instant Deposits

The 0.5% to 1.75% fee for Instant deposits may seem negligible on small amounts, but on a $1,000 transfer, a 1.75% fee amounts to $17.50. For a small business owner or a freelancer, these costs can add up to hundreds of dollars annually. When managing your “Money” niche activities, it is vital to calculate whether the immediate need for that cash outweighs the percentage lost to the platform.

Understanding Withdrawal Caps and Limits

Cash App imposes limits on how much you can “Cash Out” to your bank account. For unverified accounts, these limits are quite restrictive. However, once verified, users can often transfer up to $25,000 per week. Understanding these caps is essential for those using Cash App as a primary vehicle for receiving large payments, such as rent or professional fees. If your incoming cash flow exceeds your weekly withdrawal limit, you may find your capital “trapped” in the app for a period, which could impact your ability to meet external financial obligations.

Tax Implications and Reporting Requirements

As of recent IRS regulations, third-party settlement organizations like Cash App are required to report gross payments for goods and services that exceed $600 in a calendar year via Form 1099-K. It is crucial to distinguish between personal transfers (splitting a bill) and business transactions. Proper record-keeping is necessary to ensure that when you transfer money to your bank, you are prepared for the potential tax liabilities associated with those funds.

Security Best Practices for Digital Asset Management

In the realm of personal finance, security is the highest priority. Moving money between apps and banks creates points of vulnerability that must be managed with diligence.

Safeguarding Your Account with Two-Factor Authentication (2FA)

The first line of defense is ensuring that your Cash App account is locked behind multiple layers of security. Enabling the “Security Lock” feature requires your PIN or biometric data for every transfer. Furthermore, ensuring that the email and phone number associated with your account have two-factor authentication (2FA) enabled prevents unauthorized “Cash Out” attempts by bad actors who might gain access to your device or credentials.

Recognizing and Avoiding Common Phishing Scams

Financial tools are frequent targets for social engineering scams. A common tactic involves “support” scams where individuals pose as Cash App representatives to gain access to your sign-in code. It is important to remember that Cash Out transfers should only be initiated by you within the app. No legitimate representative will ever ask you to send money or provide a code to “verify” a transfer to your bank.

The Role of FDIC Insurance in Fintech

One common misconception in digital finance is that funds held in apps are as safe as funds in a bank. While Cash App is not a bank itself, its banking partners (like Sutton Bank or Lincoln Savings Bank) provide FDIC insurance for funds held in accounts with a “Cash App Card.” However, the insurance generally applies to the balance, not necessarily the money in transit. Moving your funds to a traditional bank account ensures that your capital is protected by federal insurance and traditional banking regulations.

Integrating Cash App into Your Personal Finance Strategy

Mastering the transfer from Cash App to a bank account is just one part of a larger financial strategy. To maximize your money’s potential, you should view Cash App as a high-velocity transit point rather than a final destination for your wealth.

Using Cash App for Micro-Investing and Bitcoin

Cash App offers unique features like “Round Ups,” where spare change from your purchases is invested into stocks or Bitcoin. While these features are excellent for wealth building, the eventual “Cash Out” of these investments back to your bank account requires an understanding of capital gains taxes. When you sell stock or Bitcoin within the app, the proceeds are added to your Cash App balance, which can then be transferred to your bank following the steps outlined above.

Managing Cash Flow Between Digital Wallets and Traditional Banks

A sophisticated user maintains a “frictionless” flow of capital. This means keeping only what is necessary for immediate P2P transactions in the digital wallet and moving the surplus into a high-yield savings account (HYSA) via the Standard transfer method. By doing so, you avoid fees and ensure that your idle cash is earning interest—something most digital wallets do not offer.

In conclusion, the ability to transfer money from Cash App to your bank account is a vital skill in the modern economy. By choosing the right transfer speed, understanding the fee structures, and maintaining rigorous security standards, you can ensure that your digital earnings are seamlessly integrated into your broader financial life. Whether you are optimizing for speed or for cost, your mastery over these tools is a testament to your financial literacy in an increasingly digital world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.