For many Americans, Social Security is not just a monthly check; it is the bedrock of their retirement strategy. Despite its importance, the methodology used to determine the exact dollar amount a retiree receives remains shrouded in complexity for the average worker. Understanding how to calculate Social Security benefits is essential for effective financial planning, as it allows you to project your future cash flow and make informed decisions about when to stop working.

While the Social Security Administration (SSA) provides automated estimates, a deep dive into the underlying mechanics—including indexing, “bend points,” and the impact of filing ages—is necessary for anyone looking to maximize their lifetime wealth. This guide breaks down the multi-step process used to determine your benefits, providing the clarity needed to navigate your financial future.

1. The Core Formula: From Lifetime Earnings to the Primary Insurance Amount (PIA)

The calculation of Social Security benefits is not based on your final salary or your total career contributions. Instead, it is rooted in a formula designed to replace a portion of your career-average earnings. This process involves two critical metrics: Average Indexed Monthly Earnings (AIME) and the Primary Insurance Amount (PIA).

Understanding Average Indexed Monthly Earnings (AIME)

The first step in the calculation is identifying your 35 highest-earning years. The SSA looks at your entire work history and “indexes” your past earnings to account for inflation. This ensures that the $15,000 you earned in 1985 is weighted fairly against the $60,000 you earned in 2023.

If you have worked more than 35 years, only the highest 35 (after indexing) are used. If you have worked fewer than 35 years, the remaining years are averaged in as zeros, which significantly lowers your benefit. The sum of these 35 years is divided by 420 (the number of months in 35 years) to arrive at your AIME.

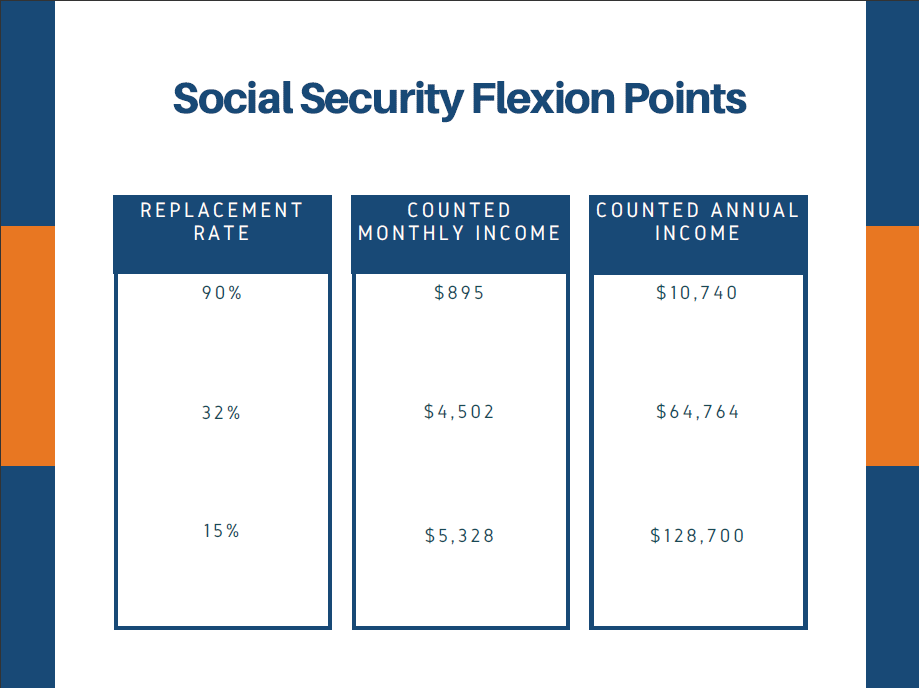

The Application of “Bend Points”

Once the AIME is established, the SSA applies a formula to determine your Primary Insurance Amount (PIA)—the monthly benefit you would receive if you retired exactly at your Full Retirement Age (FRA).

Social Security is a progressive system, meaning it replaces a higher percentage of income for lower-earners than for higher-earners. For 2024, the formula applies three fixed percentages to different portions of your AIME:

- 90% of the first $1,174 of your AIME.

- 32% of AIME amounts between $1,174 and $7,078.

- 15% of any AIME amount exceeding $7,078.

The sum of these three amounts, rounded down to the nearest dime, becomes your PIA. This “bend point” structure ensures a social safety net while still rewarding higher lifetime contributions.

2. The Impact of Timing: Full Retirement Age and Filing Adjustments

Knowing your PIA is only half the battle. Your actual monthly check depends heavily on when you choose to begin receiving benefits. The SSA assigns every individual a Full Retirement Age (FRA) based on their birth year—typically between 66 and 67.

The Penalty for Early Filing

You can begin claiming Social Security as early as age 62, but doing so comes at a permanent cost. If you claim before your FRA, your benefit is reduced by a fraction of a percent for each month of “early” retirement.

For someone with an FRA of 67, claiming at 62 results in a permanent 30% reduction in their monthly payout. This reduction is calculated as 5/9 of 1% for each of the first 36 months, and 5/12 of 1% for each month beyond that. For the lifestyle-conscious retiree, this reduction can represent a significant loss in purchasing power over a 20- or 30-year retirement.

The Reward for Delayed Retirement Credits

Conversely, if you choose to delay your benefits past your FRA, your monthly check increases for every month you wait, up until age 70. These are known as Delayed Retirement Credits.

For those born in 1943 or later, the benefit increases by 8% for each full year of delay. If your FRA is 67 and you wait until 70 to claim, your monthly benefit will be 124% of your PIA. This is one of the most effective “guaranteed” returns available in the financial world, making delayed filing a primary strategy for those who have other assets to live on in their late 60s.

3. Specialized Calculations: Spousal, Survivor, and Disability Benefits

Social Security is not a “one size fits all” program. Many households must account for benefits that are not based solely on their own work history.

Calculating Spousal Benefits

A spouse is generally eligible for a benefit of up to 50% of the primary earner’s PIA. If a spouse’s own work record would result in a lower benefit than the 50% spousal amount, the SSA will pay the higher amount. It is important to note that if the spouse claims their benefit before their own FRA, the amount will be reduced. Furthermore, the primary earner must have filed for their own benefits before the spouse can claim a spousal benefit.

Survivor and Disability Benefits

In the event of a worker’s death, the calculation changes to focus on the survivor. A widow or widower can typically receive 100% of the deceased spouse’s benefit amount, provided they have reached their own FRA.

For Social Security Disability Insurance (SSDI), the calculation is slightly different. The 35-year rule is often waived because the worker may not have had time to accumulate 35 years of earnings. Instead, the PIA is calculated based on the indexed earnings up to the point the disability began, ensuring that individuals are not penalized for an unexpected end to their career.

4. Strategic Planning: Maximizing Your Payout and Managing Taxes

Calculation is not just about math; it’s about strategy. To maximize the value of your Social Security, you must consider external factors like the “Earnings Test” and the taxability of your benefits.

The Retirement Earnings Test

If you choose to work while receiving Social Security benefits before reaching your FRA, the SSA may temporarily withhold a portion of your benefits. In 2024, if you are under your FRA, the SSA deducts $1 from your benefit payments for every $2 you earn above $22,320.

While this sounds like a “tax,” it is technically a deferral. Once you reach your FRA, the SSA recalculates your benefit amount to account for the months where benefits were withheld, effectively increasing your monthly check for the rest of your life.

The Impact of Taxes on Benefits

Many retirees are surprised to find that their Social Security benefits are taxable. The calculation for this is based on your “provisional income,” which is the sum of your Adjusted Gross Income (AGI), tax-exempt interest, and 50% of your Social Security benefits.

- If your provisional income is between $25,000 and $34,000 (individual) or $32,000 and $44,000 (joint), up to 50% of your benefits may be taxable.

- Above those thresholds, up to 85% of your benefits can be subject to federal income tax.

Understanding this calculation is vital for tax-efficient withdrawal strategies, such as balancing Social Security with 401(k) distributions.

5. Utilizing Financial Tools for Precise Forecasting

While manual calculations provide a fundamental understanding of how the government values your labor, the sheer volume of data involved—decades of earnings and annual COLA (Cost of Living Adjustment) changes—makes digital tools indispensable.

The “My Social Security” Account

The most accurate data comes directly from the source. By creating an account on the SSA website, you can access your Social Security Statement. This document provides a year-by-year history of your earnings and offers personalized estimates for your benefits at ages 62, FRA, and 70. It is a critical document for identifying errors in your work history; if an employer failed to report earnings correctly, your benefit calculation will be permanently lower unless corrected.

Advanced Planning Software

For those with complex financial lives—such as those with multiple marriages, significant age gaps between spouses, or government pensions (which may trigger the Windfall Elimination Provision)—basic calculators may fall short. Professional financial planners often use sophisticated software that runs thousands of “what-if” scenarios to determine the optimal month to file. These tools account for life expectancy, tax brackets, and investment returns, ensuring that Social Security integrates seamlessly into a broader wealth management plan.

In conclusion, calculating Social Security benefits is a multifaceted process that involves much more than a simple percentage of your salary. It requires an understanding of indexed earnings, the progressive nature of the PIA formula, and the mathematical consequences of filing age. By mastering these variables, you move from a passive recipient of a government benefit to an active manager of your financial legacy, ensuring that you receive every dollar you have earned through years of contribution.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.