Social Security remains the cornerstone of retirement planning for millions of Americans. While it was never intended to be the sole source of income in one’s golden years, it provides a guaranteed, inflation-adjusted floor that is vital for long-term financial stability. However, many workers treat Social Security as a “black box”—something they will simply deal with once they stop working.

Understanding your estimated benefit now, rather than later, is a critical component of a proactive financial strategy. Knowing your numbers allows you to bridge the gap between your projected expenses and your other income sources, such as 401(k)s, IRAs, and brokerage accounts. This guide provides a deep dive into how to find your estimated benefits, the math behind the numbers, and the strategic decisions that can significantly increase your monthly payout.

Understanding the Foundation of Your Social Security Estimate

Before you can accurately plan for the future, you must understand what your Social Security estimate actually represents. It is not a static number; it is a dynamic projection based on your current earnings history and assumptions about your future work life.

What is the Social Security Statement?

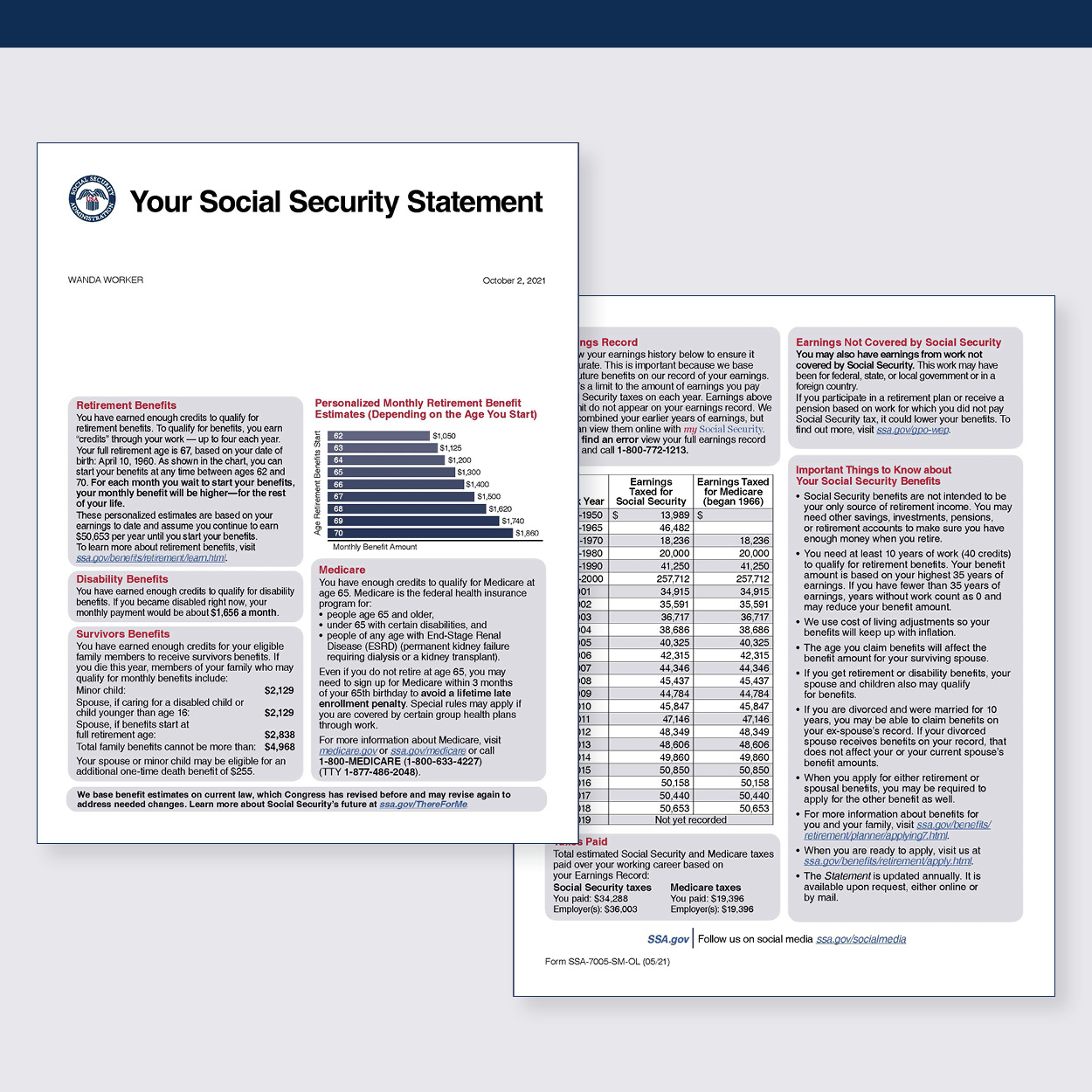

The Social Security Statement is the official document provided by the Social Security Administration (SSA) that summarizes your earnings history and provides estimates for retirement, disability, and survivor benefits. For those in the middle of their careers, this document is an essential “financial health check.” It allows you to verify that the government has accurately recorded your income for every year you have worked. Since your benefit is calculated based on these records, even a single missing year or an incorrect decimal point can cost you thousands of dollars over the course of your retirement.

How the SSA Calculates Your Primary Insurance Amount (PIA)

The “estimated benefit” you see on your statement is technically known as your Primary Insurance Amount (PIA). The SSA uses a complex formula to reach this number. First, they look at your “Average Indexed Monthly Earnings” (AIME) over your 35 highest-earning years. These earnings are adjusted—or “indexed”—for inflation to ensure that a dollar earned in 1990 is comparable to a dollar earned today.

If you have fewer than 35 years of work history, the SSA fills in the remaining years with zeros, which can significantly lower your average. This is why “finding your estimate” is often a wake-up call for individuals who have taken extended breaks from the workforce; it highlights the financial incentive to reach that 35-year milestone.

Step-by-Step Guide to Accessing Your Social Security Statement

In the past, the SSA mailed paper statements to every worker annually. Today, the process has largely moved online. Accessing your estimate is now faster and more detailed than ever, provided you know where to look.

Creating and Navigating a “my Social Security” Account

The most efficient way to find your estimated benefit is by creating a “my Social Security” account on the official SSA.gov website. Due to the sensitive nature of financial data, the registration process involves robust identity verification. You will likely need to use services like Login.gov or ID.me.

Once logged in, your dashboard provides a snapshot of your estimated monthly benefit if you were to retire at your Full Retirement Age (FRA). You can also view your “Earnings Record.” Financial experts recommend downloading this PDF at least once a year. By doing so, you can cross-reference the SSA’s data with your old W-2s or tax returns. If you find a discrepancy, you can file a correction request, ensuring your future benefit is based on every dollar you actually earned.

Utilizing Online Retirement Estimators

Within the “my Social Security” portal, the SSA offers an interactive “Retirement Calculator.” This tool is superior to the static statement because it allows for “what-if” scenarios. For example, you can input a projected future salary or change your expected retirement date to see how it moves the needle.

If you are planning to transition to part-time work or take a lower-paying “passion project” job in your late 50s, the calculator can show you exactly how that choice will impact your final check. This level of granularity is essential for high-net-worth individuals and middle-class savers alike who want to model their cash flow with precision.

Factors That Influence Your Benefit Calculations

Finding your estimate is only the first step; understanding why that number fluctuates is what allows for effective financial engineering. Several variables can alter your final payout, some within your control and some dictated by the economy.

The Impact of Annual Earnings and COLA

Your estimated benefit is sensitive to the “Social Security Wage Base.” This is the maximum amount of earnings subject to Social Security tax each year ($168,600 in 2024). If you earn above this threshold, your benefit won’t increase further for that specific year.

Additionally, once you begin receiving benefits, your checks are adjusted via Cost-of-Living Adjustments (COLA). However, even before you retire, the SSA’s estimation tools factor in average wage growth across the economy. If the economy experiences stagnant wage growth, your future estimates might appear lower than expected in real purchasing power terms.

Work Credits and Eligibility Requirements

To even see an estimate for a retirement benefit, you must generally earn at least 40 “credits.” You can earn up to four credits per year by reaching a certain income threshold. For most people, this equates to 10 years of work. If you find your statement says “Not Eligible,” it usually means you haven’t hit this 10-year mark yet. For those nearing retirement who are just shy of 40 credits, working even a part-time job for a year or two can be the difference between receiving a lifetime monthly check and receiving nothing at all.

Spousal and Survivor Benefit Considerations

Your personal estimate doesn’t tell the whole story if you are married, divorced, or widowed. Spousal benefits allow a husband or wife to receive up to 50% of their partner’s FRA benefit if it is higher than their own. When you look at your estimate, you should also consider your spouse’s estimate. Often, the highest-earning spouse should delay claiming to maximize the eventual survivor benefit for the lower-earning spouse. This “household” approach to Social Security turns the estimate into a strategic piece of a much larger puzzle.

Strategic Timing: When to Claim for Maximum Payout

One of the most common mistakes people make after finding their estimated benefit is assuming they should claim it as soon as they retire. The age at which you choose to start receiving checks is perhaps the single most important financial decision you will make in your 60s.

The Full Retirement Age (FRA) Benchmark

The SSA bases your “100% benefit” on your Full Retirement Age, which is currently 67 for anyone born in 1960 or later. When you look at your online estimate, the primary number shown is usually the amount you get at this age. This serves as your baseline. If you claim exactly at your FRA, you receive exactly what you’ve earned without any reductions or bonuses.

The Cost of Early Filing at Age 62

The “my Social Security” portal will also show you a reduced estimate if you claim as early as age 62. This reduction is permanent. If your FRA is 67 and you claim at 62, your monthly check will be reduced by roughly 30%. While this may be necessary for those in poor health or those who have lost their jobs, it represents a significant loss of “guaranteed return” for those who have the assets to wait.

The Reward for Delayed Filing until Age 70

Conversely, for every year you delay claiming past your FRA (up until age 70), your benefit increases by approximately 8% per year in “delayed retirement credits.” This is a return that is nearly impossible to find in the private market with the same level of safety. If you find that your estimate at age 67 is $2,000, waiting until age 70 could boost that check to approximately $2,480—plus any COLA adjustments applied during those three years. For those with longevity in their family, waiting is often the most mathematically sound investment they can make.

Integrating Social Security into Your Broader Retirement Plan

Once you have your estimate and understand the timing variables, the final step is to view Social Security as one component of a diversified income stream. It should not be viewed in isolation.

Managing Taxes on Your Benefits

A common surprise for retirees is that Social Security benefits can be taxable. If your “combined income” (adjusted gross income + tax-exempt interest + half of your Social Security benefits) exceeds $25,000 for individuals or $32,000 for couples, you may owe federal income tax on a portion of your benefits. When you find your estimate, you should immediately subtract a projected tax percentage to see your “net” usable income. This helps in determining how much you need to withdraw from your tax-deferred accounts like a 401(k).

Social Security as a “Longevity Insurance” Policy

In the world of personal finance, Social Security is often compared to an annuity. Because it is backed by the federal government and adjusted for inflation, it serves as a hedge against “longevity risk”—the risk of outliving your money. When you look at your estimated benefit, don’t just see a monthly check; see it as a risk-management tool. If your estimate is high, you can afford to be more aggressive with your other investments. If it is low, you know you need to prioritize capital preservation in your private accounts.

Using Professional Financial Tools for Precision

While the SSA tools are excellent, they are limited. Professional-grade financial planning software can take your Social Security estimate and run “Monte Carlo” simulations. These simulations test your retirement plan against thousands of market scenarios. By plugging your Social Security estimate into these models, you can determine your “probability of success.” This gives you the confidence to spend your money in retirement, knowing that your Social Security floor is secure and that you have timed your claim to optimize your total lifetime wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.