In the realm of personal finance, few concepts carry as much weight or potential as compound interest. Often referred to as the “eighth wonder of the world,” compound interest is the engine that drives long-term wealth creation, turning modest savings into significant fortunes over time. Unlike simple interest, which is calculated only on the principal amount, compound interest is calculated on the principal plus the accumulated interest of previous periods.

Understanding how to calculate this figure is more than just a mathematical exercise; it is a fundamental skill for anyone looking to optimize their investments, manage debt, or plan for a secure retirement. This guide explores the mechanics of compound interest, the variables that influence its growth, and the practical ways you can apply these calculations to your financial strategy.

The Mechanics of Compound Interest: Moving Beyond Simple Growth

To master your finances, you must first distinguish between the two primary ways money grows: simple and compound. Simple interest is straightforward—it is a set percentage of the original amount (the principal) paid out over a period. However, compound interest is dynamic. It is “interest on interest,” and its effects become more dramatic the longer the money is allowed to grow.

Defining the “Eighth Wonder of the World”

The reason compound interest is so highly regarded in the financial world is its exponential nature. While simple growth moves in a straight line, compound growth moves in a curve that steepens over time. In the beginning, the differences might seem negligible. However, as the interest you earn begins to earn its own interest, the pace of accumulation accelerates. This creates a snowball effect where the growth in the later years of an investment often far exceeds the total contributions made in the early years.

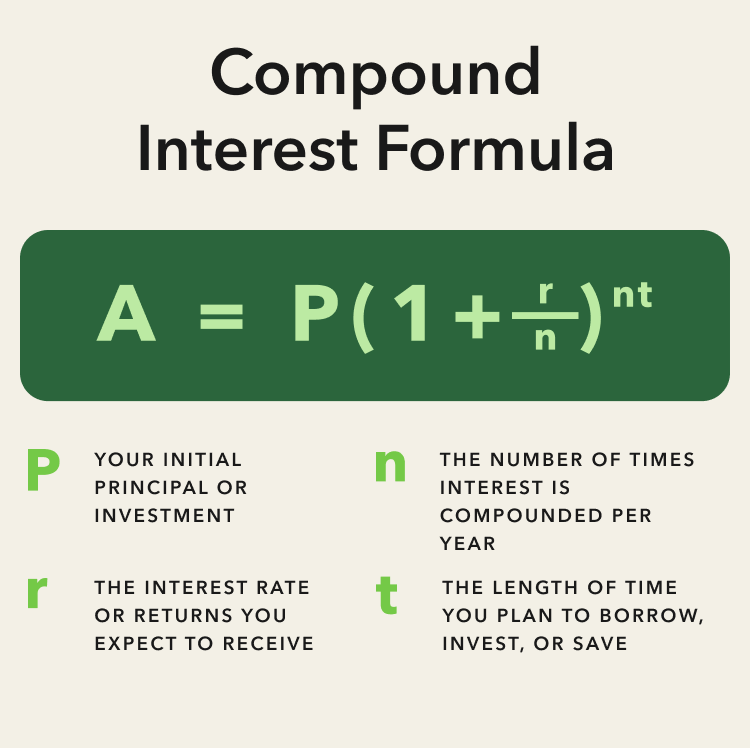

The Fundamental Formula Breakdown

Calculating compound interest requires a specific mathematical formula. While online calculators are abundant, understanding the components of the formula allows you to visualize how different factors change your ending balance. The standard formula for annual compounding is:

A = P (1 + r/n)^(nt)

- A = the final amount (the future value of the investment, including interest).

- P = the principal amount (the initial sum of money).

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per unit t.

- t = the time the money is invested for (usually years).

By deconstructing this equation, we see that the power lies in the exponent—the relationship between the frequency of compounding and the total time elapsed.

The Core Variables: What Drives Your Financial Growth?

Every compound interest calculation relies on four primary levers. By adjusting these variables, you can significantly alter the trajectory of your financial future. Understanding how each one functions is the key to strategic wealth management.

The Power of the Principal Amount

The principal is your starting line. While compounding can turn small amounts into large sums, a larger initial principal provides more “fuel” for the engine. In the context of business finance or personal investing, the principal represents your initial capital outlay. While you cannot always control having a massive starting principal, understanding its role highlights the importance of making significant initial contributions whenever possible to give the compounding process a stronger head start.

Interest Rates and the Compounding Frequency

The interest rate (r) is the speed at which your money grows. A small difference in the interest rate can result in a massive difference in the final balance over 20 or 30 years. However, the frequency of compounding (n) is equally vital.

Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily. The more frequently interest is added back to the principal, the faster the total amount grows. For example, an investment that compounds daily will yield a higher return than one that compounds annually, even if the nominal interest rate is the same. This is why financial institutions are required to disclose the Annual Percentage Yield (APY), which accounts for the effect of compounding frequency.

Time: The Most Valuable Asset

If the interest rate is the speed, time (t) is the distance. In the compound interest formula, time is the most potent variable because it is part of the exponent. This means that doubling the duration of an investment doesn’t just double the return—it can quadruple it or more. This “time value of money” is why financial advisors stress the importance of starting early. Even with a lower interest rate, an individual who starts saving in their 20s will often outperform someone who starts in their 40s with a much higher interest rate and larger monthly contributions.

Practical Calculation Methods and the Rule of 72

While the formula provides the exact math, investors often need quicker ways to estimate growth or more robust tools for complex scenarios. Whether you are using a napkin or a high-end spreadsheet, knowing how to approach the calculation is essential.

Step-by-Step Manual Calculation

To calculate compound interest manually for a single period, you multiply the principal by the interest rate. To find the second period, you add that interest to the principal and multiply again.

- Example: You invest $1,000 at a 10% annual interest rate.

- Year 1: $1,000 x 0.10 = $100 interest. Total = $1,100.

- Year 2: $1,100 x 0.10 = $110 interest. Total = $1,210.

- Year 3: $1,210 x 0.10 = $121 interest. Total = $1,331.

Notice how the interest earned increases every year ($100, then $110, then $121) even though the rate stays the same.

Utilizing Financial Tools and Spreadsheet Functions

For those managing business finances or complex portfolios, manual calculation is inefficient. Modern software like Microsoft Excel or Google Sheets uses the FV (Future Value) function to handle these calculations instantly. The syntax is typically =FV(rate, nper, pmt, [pv]). This allows you to factor in not just the initial principal, but also recurring monthly contributions (pmt), which drastically changes the outcome of the calculation.

The Rule of 72: A Mental Shortcut for Investors

The “Rule of 72” is a simplified way to determine how long it will take for an investment to double in value at a fixed annual rate of interest. By dividing 72 by the annual rate of return, investors can get a rough estimate of the number of years required for their money to double.

- At a 6% return, your money doubles in 12 years (72 / 6 = 12).

- At a 12% return, your money doubles in 6 years (72 / 12 = 6).

This mental model is incredibly useful for comparing different investment opportunities on the fly without needing a calculator.

Strategic Applications in Personal Finance

Understanding the math is only the first step; the second is applying that knowledge to your balance sheet. Compound interest is a double-edged sword—it can build your wealth or accelerate your poverty depending on which side of the equation you stand.

Investing: The Upside of Compounding

In the world of investing, compounding is the primary tool for retirement planning. When you invest in stocks, mutual funds, or ETFs, you often receive dividends. By opting for a Dividend Reinvestment Plan (DRIP), those payouts are automatically used to buy more shares. This increases your principal, which in turn increases your future dividends, creating a self-sustaining cycle of wealth. Over decades, this process is responsible for the majority of gains in long-term portfolios.

Debt: The Dark Side of Compounded Interest

Compound interest works against you when you carry debt, particularly high-interest debt like credit cards. Most credit card companies compound interest daily. If you only pay the minimum balance, the interest charges are added to your principal, and you begin paying interest on your interest. This is why small balances can quickly spiral into unmanageable debt. Understanding the math behind this allows consumers to prioritize “avalanche” or “snowball” debt repayment methods to stop the negative compounding effect.

Maximizing Your Returns: Actionable Steps for the Long Term

To truly benefit from the mechanics of compound interest, you must move beyond calculation and into execution. Strategy is what separates those who understand the concept from those who build wealth through it.

Starting Early and Staying Consistent

The “Cost of Waiting” is perhaps the most expensive mistake a person can make in their financial life. If you wait ten years to start investing, you aren’t just missing ten years of contributions; you are missing the most aggressive growth phase of the compounding curve. Consistency is the second pillar. By automating contributions to an investment account, you ensure that the “n” (frequency) and “t” (time) variables are always working in your favor, regardless of market volatility.

Minimizing Leakage: Fees and Taxes

While the compound interest formula shows how money grows, it doesn’t automatically account for what takes money away. In the real world, management fees and taxes act as “negative compounding.” A 1% annual management fee might seem small, but when compounded over 30 years, it can eat away 20% to 30% of your potential final balance. Utilizing tax-advantaged accounts like 401(k)s or IRAs and choosing low-cost index funds are essential strategies to ensure that the math of compounding works entirely for you, rather than for your broker or the government.

By mastering the calculation of compound interest and understanding the levers that drive it, you gain a level of financial clarity that few possess. Whether you are aiming for early retirement, building a business, or simply trying to eliminate debt, the principles of compounding are the foundation upon which financial freedom is built. The math is certain; the only variable that remains is how soon you choose to start.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.