In the realm of personal finance, few line items in a monthly budget cause as much confusion as auto insurance. Specifically, the term “full coverage” is often thrown around by lenders, agents, and car buyers, yet it remains one of the most misunderstood concepts in financial planning. Understanding how much full coverage insurance costs—and more importantly, what determines that cost—is essential for anyone looking to protect their assets while optimizing their cash flow.

Navigating the landscape of insurance premiums requires a balance between risk management and cost efficiency. For most drivers, insurance is not merely a legal requirement; it is a critical hedge against catastrophic financial loss. This article breaks down the financial mechanics of full coverage insurance, the variables that dictate your premium, and how to integrate this expense into a robust financial strategy.

Understanding the Financial Components of “Full Coverage”

Technically, “full coverage” is not a specific policy type you can buy. Instead, it is a colloquialism used in the financial world to describe a combination of coverages that protect both the policyholder and third parties. To understand the cost, one must first understand the ingredients of the policy.

The Triple Threat: Liability, Collision, and Comprehensive

A full coverage policy typically consists of three primary pillars. The first is Liability Insurance, which covers bodily injury and property damage to others if you are at fault. This is the foundation of any policy and is legally mandated in almost every state.

The second pillar is Collision Insurance. This pays for damage to your own vehicle resulting from an accident, regardless of who is at fault. From a personal finance perspective, this is vital if you do not have the liquid capital to replace your vehicle out of pocket.

The third pillar is Comprehensive Insurance. This covers “acts of God” or non-collision events, such as theft, vandalism, fire, or weather damage. Together, these three components form what we call full coverage.

The Role of Deductibles in Your Financial Plan

The deductible is the amount you agree to pay out of pocket before the insurance company kicks in. In the context of “Money,” the deductible is a powerful lever. A higher deductible—say $1,000 instead of $500—will significantly lower your monthly premium. However, this requires you to have an emergency fund capable of covering that $1,000 at a moment’s notice. Choosing the right deductible is a delicate balancing act between monthly fixed costs and potential out-of-pocket liabilities.

Additional Add-ons: Gap Insurance and Personal Injury Protection

For those financing a vehicle, “full coverage” may also need to include Gap Insurance. Because cars depreciate the moment they leave the lot, you might owe more on your loan than the car is worth. If the car is totaled, standard collision insurance only pays the market value. Gap insurance covers the “gap” between the value and the loan balance, preventing a financial deficit.

Factors That Dictate the Cost of Your Premium

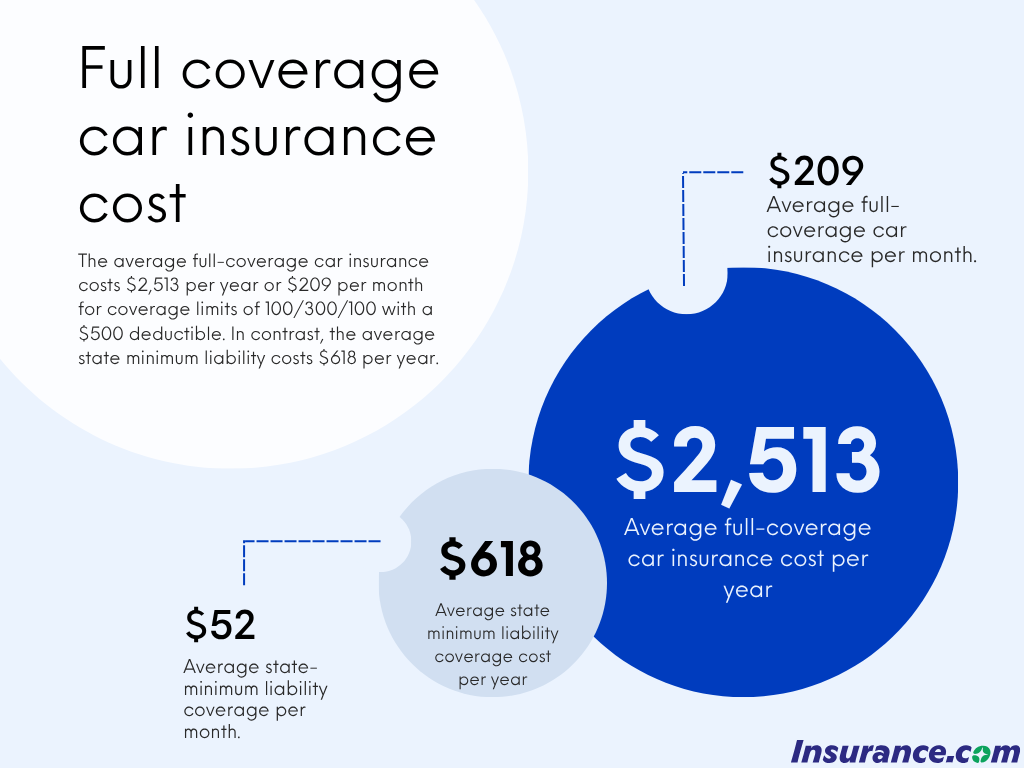

The cost of full coverage insurance is not a static number. Nationally, the average cost of full coverage insurance in the United States typically ranges from $1,500 to $2,500 per year, or roughly $125 to $200 per month. However, these figures can fluctuate wildly based on several financial and behavioral metrics.

Demographic and Geographic Variables

Insurance is a game of actuarial science—the mathematical assessment of risk. Your age, gender, and marital status play a significant role. Statistically, younger drivers are more prone to accidents, leading to higher premiums. Conversely, married drivers are often viewed as more stable and risk-averse, frequently qualifying for lower rates.

Geography is equally impactful. If you live in a high-traffic urban area with high crime rates, your comprehensive and collision premiums will be higher than someone living in a rural area with a locked garage. States like Florida and Louisiana often see higher premiums due to weather-related risks, whereas states like Maine or Ohio may enjoy lower rates.

The Impact of Credit Scores on Insurance Costs

In many states, insurance companies use a “credit-based insurance score” to help determine your premium. This is a crucial intersection of personal finance and insurance. Data suggests that individuals with higher credit scores are less likely to file claims. Therefore, if you are working on improving your financial health by paying down debt and maintaining a high credit score, you will likely be rewarded with lower insurance premiums. A poor credit score can, in some cases, double the cost of a full coverage policy.

Vehicle Type and Replacement Value

The “what” is as important as the “who.” A high-end luxury SUV or a precision-engineered sports car costs significantly more to repair or replace than a standard sedan. Furthermore, vehicles equipped with advanced safety features (like automatic braking or lane-assist) may qualify for discounts, though the high cost of repairing those sensors can sometimes offset the savings.

The Cost-Benefit Analysis: When is Full Coverage Worth It?

From a wealth-management perspective, you must constantly evaluate whether the cost of insurance is justified by the protection it provides. While lenders require full coverage for financed vehicles, those who own their cars outright have a choice.

The 10% Rule of Thumb

A common financial guideline is the “10% Rule.” If the annual cost of your collision and comprehensive coverage exceeds 10% of your car’s total replacement value, it may be time to “self-insure.” For example, if your car is worth $4,000 and your full coverage premiums (minus the liability portion) cost $500 a year with a $1,000 deductible, you are paying a significant amount to protect a relatively small asset. In this scenario, dropping to liability-only and moving those premium savings into a high-yield savings account might be the smarter financial move.

Protecting Your Net Worth

For high-net-worth individuals, full coverage is less about the car and more about protecting total assets. If you are involved in a major accident and your liability limits are too low, your savings, investments, and even your home could be at risk in a lawsuit. In this context, the “cost” of insurance is a small price to pay for a shield around your entire financial portfolio.

The Opportunity Cost of High Premiums

Every dollar spent on insurance is a dollar not invested in the stock market or a retirement account. Therefore, over-insuring is a form of financial leakage. By auditing your policy annually and ensuring you aren’t paying for “zombie” coverages you don’t need, you can redirect that capital toward wealth-building vehicles.

Strategies to Optimize and Lower Your Insurance Costs

Reducing the cost of full coverage insurance doesn’t necessarily mean reducing your protection. It means being a savvy consumer of financial products.

Comparison Shopping and Re-quoting

The insurance market is highly competitive. Many drivers stay with the same carrier for a decade out of habit, failing to realize that their risk profile has changed. If you have turned 25, gotten married, or improved your credit score, you should shop your policy immediately. Using independent brokers or online comparison tools can often reveal savings of hundreds of dollars per year for the exact same coverage.

Bundling and Loyalty Discounts

Most major financial institutions offer discounts for “bundling” multiple products. Combining your homeowners or renters insurance with your auto policy is one of the most effective ways to slash 10% to 15% off your total bill. Additionally, many companies offer discounts for “safe driving” via telematics—small devices or apps that track your driving habits. If you are a low-mileage driver or a cautious one, this can result in significant “money back” in the form of lower premiums.

Reviewing Policy Limits Annually

As your financial situation evolves, so should your policy. If you have recently increased your emergency fund, you might be able to afford a higher deductible, which lowers your premium. If your car has aged significantly, the value of the comprehensive and collision portions of your policy has decreased, and your premium should reflect that.

Integrating Insurance into Your Long-Term Financial Plan

Auto insurance should not be viewed as an isolated expense. It is a vital component of a comprehensive financial plan, sitting alongside your emergency fund, your health insurance, and your investment strategy.

Insurance as a Risk Management Tool

In professional finance, risk management is about identifying potential threats to capital and mitigating them. A car accident is a “low probability, high impact” event. Full coverage insurance converts an unpredictable, potentially ruinous cost into a predictable, manageable monthly expense. This stability allows for better long-term budgeting and investment planning.

Building an “Insurance Buffer”

A sophisticated financial approach involves creating an “insurance buffer” within your emergency fund. This is a dedicated portion of your savings that covers your insurance deductibles and any potential rental car costs not covered by your policy. By having this cash set aside, you can confidently opt for higher deductibles, thereby lowering your fixed monthly costs and increasing your monthly investable income.

Conclusion: The True Value of Full Coverage

So, how much is full coverage insurance? While the answer in dollars depends on your specific circumstances, the answer in value is found in the security it provides. For most, the cost of a full coverage policy is a necessary investment in financial peace of mind. By understanding the factors that drive these costs and actively managing your policy like any other investment, you can ensure that you are protected against the unexpected without overpaying for the privilege.

In the end, the goal of personal finance is not just to accumulate wealth, but to protect it. A well-structured full coverage insurance policy is one of the most effective tools at your disposal to ensure that one bad day on the road doesn’t derail years of financial progress.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.