When navigating the complexities of a separation or divorce involving children, the question of “how much is child support” is often the most pressing financial concern for both parents. Child support is not merely a legal obligation; it is a significant factor in personal financial planning that dictates cash flow, lifestyle adjustments, and long-term wealth management for two separate households. Understanding the mechanics behind these payments is essential for maintaining financial stability and ensuring the well-being of the children involved.

From a personal finance perspective, child support represents a recurring, non-negotiable expense for the payor and a critical revenue stream for the payee. Because the amounts are determined by statutory guidelines that vary significantly by jurisdiction, approaching the topic with a rigorous, data-driven mindset is the best way to prepare for the future.

Understanding the Financial Framework of Child Support Calculations

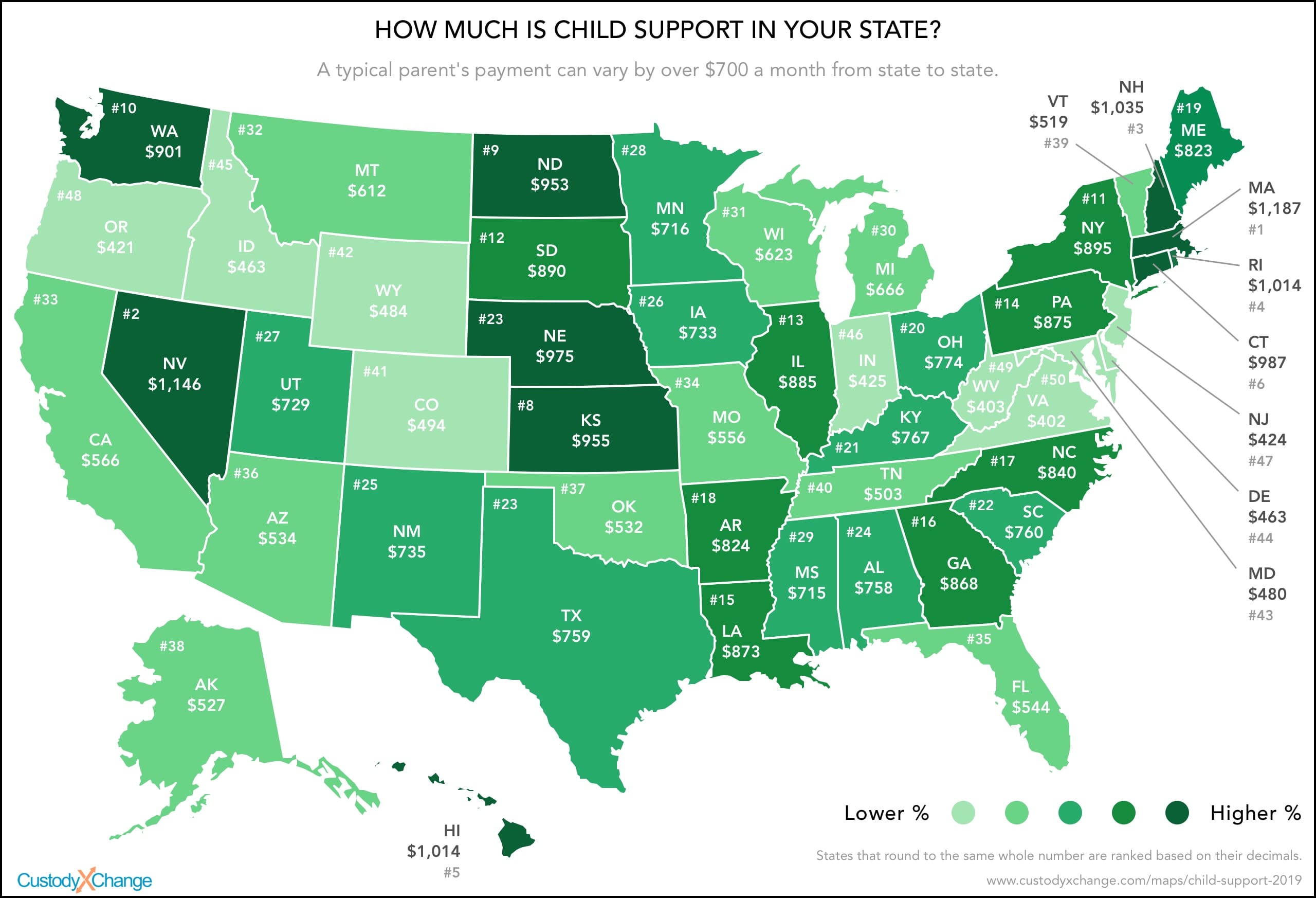

Child support is grounded in the principle that children should receive the same proportion of parental income that they would have received if the parents lived together. To standardize this, most regions utilize specific economic models to determine the “sticker price” of raising a child.

The Income Shares Model

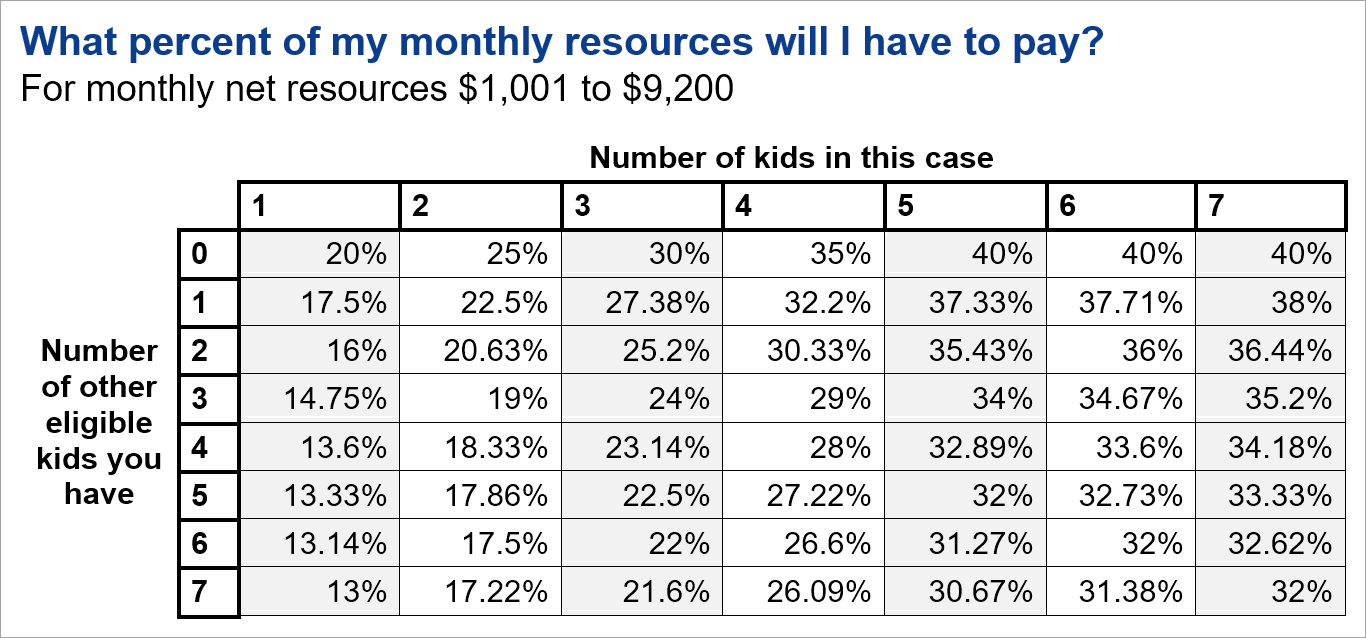

The most common methodology used today is the Income Shares Model. This approach estimates the total amount of money parents would spend on their children if they were still living in one household. That total “basket of goods and services” is then divided between the parents based on their respective incomes. For example, if Parent A earns $70,000 and Parent B earns $30,000, Parent A is responsible for 70% of the calculated support amount.

The Percentage of Income Model

Some jurisdictions prefer a simpler “Percentage of Income” model. In this scenario, the court applies a flat percentage to the non-custodial parent’s income—such as 17% for one child or 25% for two—regardless of what the custodial parent earns. While this is easier to calculate, it often fails to account for the nuances of modern dual-income households, making it a more rigid financial burden for the payor.

Melson Formula and Discretionary Adjustments

A third, more complex model known as the Melson Formula incorporates a “self-support reserve.” This ensures that the parent paying support is left with enough money to maintain a basic standard of living before the support amount is finalized. Understanding which model your jurisdiction uses is the first step in forecasting your post-divorce budget.

Core Factors That Influence the Final Dollar Amount

Determining the actual cost of child support involves more than just looking at a salary stub. It requires a deep dive into “Adjusted Gross Income” and several secondary financial variables that can drastically shift the final figure.

Defining “Income” in a Financial Context

In the eyes of the court, income often extends beyond a base salary. It typically includes bonuses, commissions, interest from investments, rental income, and even certain employer-provided perks like a car allowance. For business owners and entrepreneurs, this calculation becomes more complex. Courts may “pierce” the corporate veil to look at the actual cash flow of a business, ensuring that a parent isn’t artificially lowering their salary to reduce support obligations.

The Impact of Parenting Time (Custody Split)

The amount of time a child spends with each parent has a direct “offset” effect on child support. In many states, if a parent has the child for more than 35% or 40% of the year (often measured in overnights), the child support amount is reduced. This recognizes that the parent is already incurring direct costs—such as food, utilities, and entertainment—while the child is in their care. From a financial planning perspective, a move from “sole custody” to “joint physical custody” can result in a significant swing in monthly cash flow.

Imputed Income and Underemployment

A common financial pitfall in child support cases is “imputed income.” If a parent is voluntarily unemployed or underemployed—for instance, a high-earning software engineer taking a minimum-wage job to avoid payments—the court may calculate support based on what that parent could be earning. This creates a dangerous financial gap where the legal obligation exceeds the parent’s actual liquid cash, leading to rapid debt accumulation.

Beyond the Base Payment: Extraordinary Expenses and Add-Ons

The “basic” child support figure rarely covers the total cost of raising a child. In most financial arrangements, there are “add-on” expenses that are shared proportionally between the parents, often on top of the monthly base payment.

Healthcare and Health Insurance Premiums

The cost of maintaining a child on a health insurance plan is usually a shared expense. If Parent A pays $400 a month to add the child to their employer-sponsored plan, they generally receive a credit for a portion of that cost in the child support formula. Furthermore, “unreimbursed medical expenses”—such as braces, therapy, or emergency room co-pays—are typically split based on income percentages.

Childcare and Education Costs

For working parents, childcare (daycare, after-school care, or nannies) is often the largest single expense after housing. Because these costs are necessary for the parents to earn an income, they are almost always treated as mandatory add-ons. Similarly, if a child has historically attended private school, the court may order that these tuition payments continue, creating a long-term fixed liability that must be accounted for in a multi-year financial forecast.

Extracurricular Activities and “Hidden” Costs

Sports, music lessons, and summer camps are frequently debated. While not always legally mandated in the same way as healthcare, many parents include specific clauses in their financial agreements to share these costs. Without a clear agreement, these “hidden” costs can lead to “financial creep,” where the custodial parent absorbs more than their fair share of the child’s lifestyle expenses.

Managing Cash Flow and Personal Budgeting for Child Support

Once the amount is determined, both the payor and the recipient must treat child support as a core component of their personal finance strategy. Failure to manage this cash flow properly can lead to legal penalties, damaged credit, or household insolvency.

Integrating Support into a Monthly Budget

For the payor, child support should be viewed as a “top-line” expense, similar to a mortgage or taxes. It is often deducted directly from wages via an Income Withholding Order (IWO). While this ensures consistency, it also means the parent’s “take-home pay” is significantly lower than their gross earnings suggest. Budgeting must be done based on the net amount after support is removed.

For the recipient, child support is a vital revenue stream, but it is also a “risky” one. Dependence on child support can be dangerous if the payor loses their job or becomes unable to pay. A sound financial strategy involves using child support for the child’s direct needs while ensuring the parent’s own essential expenses (like their own retirement savings) are not entirely dependent on those payments.

Tax Implications and the TCJA

Following the Tax Cuts and Jobs Act (TCJA) of 2017, the tax treatment of child support remained clear: it is tax-neutral. Unlike alimony (for agreements finalized after 2018), child support is not tax-deductible for the payer, nor is it considered taxable income for the recipient. This is a critical distinction for tax planning; the money you pay is “after-tax” dollars, meaning its real cost to your wealth is higher than the nominal dollar amount.

Modifying Support and Long-Term Wealth Planning

Child support is rarely a static figure. As financial circumstances change, the “price” of support can and should be adjusted to reflect current realities.

The “Significant Change in Circumstances” Rule

Most jurisdictions allow for a modification of child support if there is a “significant change in circumstances”—usually defined as a 10% to 15% shift in income. This could be due to a promotion, a layoff, or a change in the child’s needs. From a business finance perspective, it is imperative to file for a modification immediately upon a loss of income; child support arrears (back pay) generally cannot be reduced retroactively, meaning the debt stays on the books even if the income is gone.

Planning for College and Post-Minority Support

In many regions, child support ends at age 18 or upon high school graduation. However, some states allow for “post-minority” support to cover college expenses. Incorporating 529 plans or other educational savings vehicles into a child support agreement is a sophisticated way to manage future liabilities. By locking in these contributions early, parents can mitigate the “sticker shock” of university tuition later in life.

Life Insurance as a Financial Safeguard

To protect the “income stream” of child support, many agreements require the payor to maintain a life insurance policy with the children (or the other parent) as the beneficiary. This ensures that if the payor passes away, the financial needs of the children are met through a lump-sum death benefit, effectively “pre-paying” the remaining support obligation.

In conclusion, determining how much child support will be is a multifaceted financial calculation that extends far beyond a simple chart. It requires a comprehensive understanding of income definitions, custody impacts, and future expense forecasting. By approaching child support with the same rigor one would apply to a business investment or a retirement plan, parents can ensure financial stability for themselves and a secure future for their children.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.